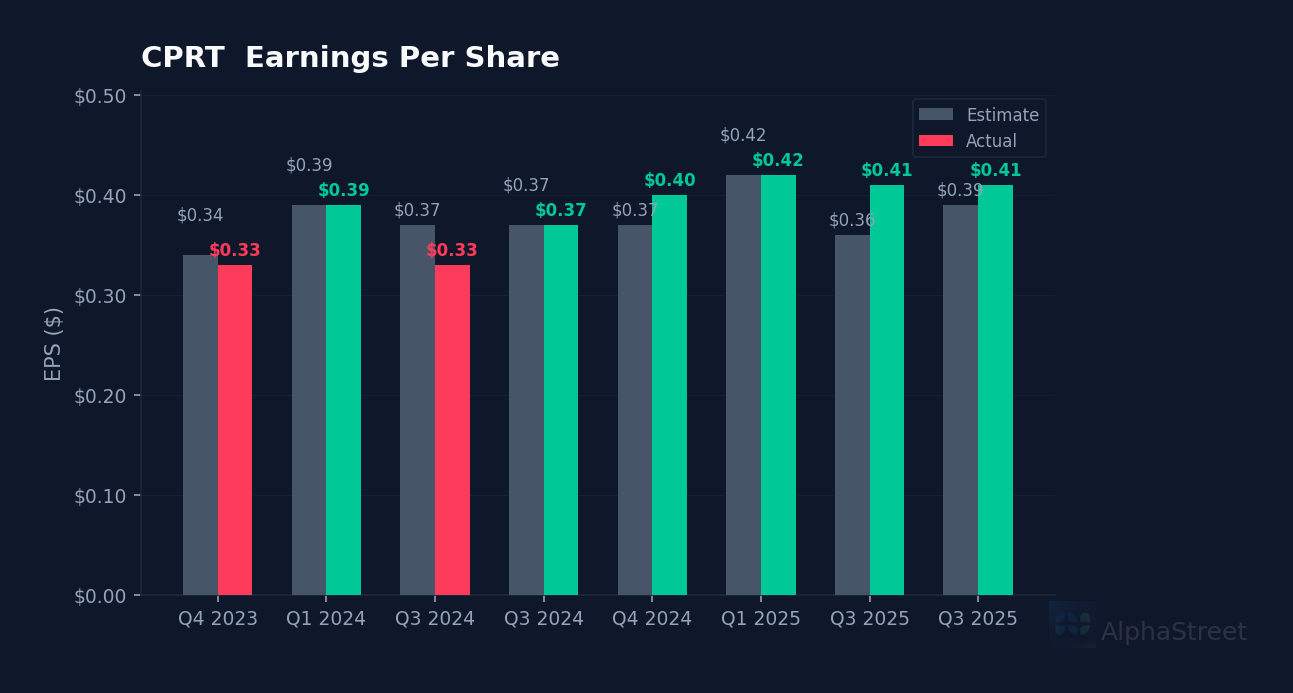

Markets yawn at the beat. Copart posted Q2 fiscal 2026 EPS of $0.41, topping consensus $0.39 by 5.1%, matching the same beat magnitude from Q1. Revenue hit $4.66B for the quarter. Yet shares slipped 0.03% in after-hours trading to $37.31, extending a brutal three-month slide that’s dragged the stock down 9.5% from $41.32 in mid-November to current levels near $37.44.

The insurance volume puzzle. CEO Jeff Liaw addressed trends in Copart’s core insurance business on the earnings call, noting the company continues working through competitive dynamics with certain insurers. One analyst pressed on whether Copart sees any path to recapturing volume lost to competitors despite the company’s higher auction returns—a question that drew measured commentary about Progressive’s relative competitiveness. With insurance claims representing the bulk of salvage vehicle supply, any sustained volume pressure could cap revenue growth even as ASPs climb.

Noninsurance growth provides offset. Liaw highlighted progress expanding the company’s noninsurance vehicle channels, which include dealer trade-ins, fleet disposals, and rental car off-rentals. This segment has become increasingly important as a diversification lever, particularly given the company’s 34.2% profit margin and premium valuation at 23.0x trailing earnings. The international segment also remains a long-term growth driver, though CFO Leah Stearns provided limited incremental color on Q2 international performance beyond consolidated results.

Buyback silence raises eyebrows. During Q&A, an analyst asked pointedly about Copart’s capital allocation plans, specifically why the company might not deploy its balance sheet on share repurchases over the next 6-12 months. Management’s response suggested caution around the current economic outlook, unusual for a company sitting on $10.6B in total assets and generating $403.7M in quarterly net income. That hesitation may signal internal concern about sector headwinds—or simply prudent cash preservation ahead of potential market volatility.

Valuation pressure mounts. Trading at $37.44 versus an analyst target of $48.89, Copart faces a 30.6% implied upside—but the stock has underperformed that target consistently, sitting 23.5% below its 200-day moving average of $45.69. The forward P/E of 20.8x and trailing P/E of 23.0x look stretched against just 0.7% revenue growth, raising questions about whether the market has lost patience with the company’s growth trajectory. Volume 37% above average on February 12 accompanied a single-day 7.1% plunge, suggesting institutional repositioning.

This article was generated using AlphaStreet’s proprietary financial analysis technology and reviewed by our editorial team.