CSX Corp. (NASDAQ: CSX), a leading provider of rail-based transportation services, has maintained stable revenues over the years but the business has been affected by inflation and high fuel expenses, lately. The cost pressure and macro challenges have prompted the company to take steps to increase volumes by enhancing operating efficiency.

In a sign that the management’s initiatives are paying off, the Jacksonville-headquartered freight mover reported strong earnings and revenue growth for the first quarter. The stock got a major boost after last week’s earnings announcement. CSX has been pretty stable though it declined about 15% since peaking more than a year ago.

Buy CSX?

Going by the stock’s past performance, it is expected to make modest gains this year. However, that is unlikely to create meaningful shareholder value, and the company’s unimpressive dividends – marked by multiple reductions and modest yield – might discourage long-term investors. Also, the outlook for the railroad industry this year is not very optimistic due to macro concerns and fears of an imminent recession. So, it makes sense to keep a tab on future earnings and look for positive cues before taking a position in the stock.

It is worth noting that the company did not provide guidance for fiscal 2023, citing the market uncertainties. The management has been able to ease tensions with labor unions and disputes with shippers recently by effectively implementing ‘One CSX’, a cultural initiative envisaged to better engage with stakeholders. The efforts got a fillip under new CEO Joe Hinrichs who took office in September 2022, succeeding James Foote.

Road Ahead

Increased volumes, mainly in coal and domestic merchandise shipments, and the revamped workforce should enable the company to perform better this year. Meanwhile, inflation-related cost pressure is expected to persist for the rest of the year, restricting margin growth. The performance of the International division is likely to remain weak. While the high demand for logistics services amid the COVID-induced supply chain disruption can be a tailwind, the volume trend will likely be mixed across the segments.

From CSX’s Q1 2023 earnings conference call:

“We continue to benefit from the favorable pricing environment with customer negotiations supported by our transparency on costs and our improved service products. We still expect supplemental revenues to decline by roughly $300 million compared to last year, with much of that decline in run rate already apparent in the first quarter. International met coal benchmarks remained very strong over the quarter and spot prices are just below $300 per tonne today, but year-over-year comparisons will get tougher from here.”

Positive Data

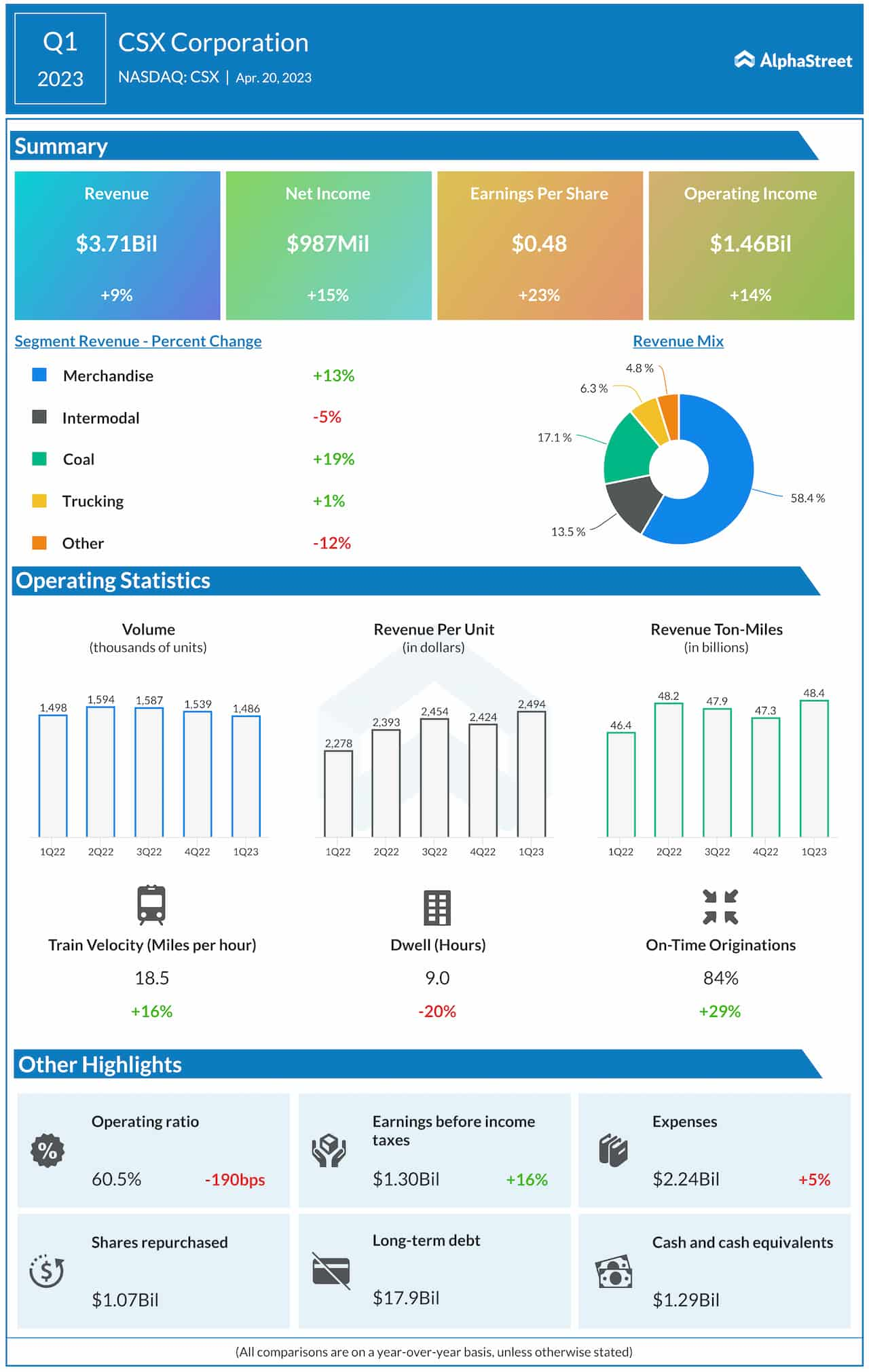

The company had a positive start to 2023 with earnings and revenues beating estimates in the first quarter, continuing the recent trend. Revenues increased 9% to $3.71 billion and topped expectations as a modest decline in freight volumes was more than offset by better unit prices that rose 9% from last year to $2,494. There was double-digit growth in the main merchandise and coal segments, while the other areas experienced weakness. Driven by the strong top-line growth, net profit rose to $987 million or $0.48 per share from $859 million or $0.39 per share in Q1 2022. There was a 5% annual increase in operating expenses, while the operating ratio came in at 60.5%.

The company’s stock traded slightly lower in early trading on Monday, after closing the previous session at $30.81. It has gained 13% in the past six months.