AlphaStreet Newsdesk powered by AlphaStreet Intelligence

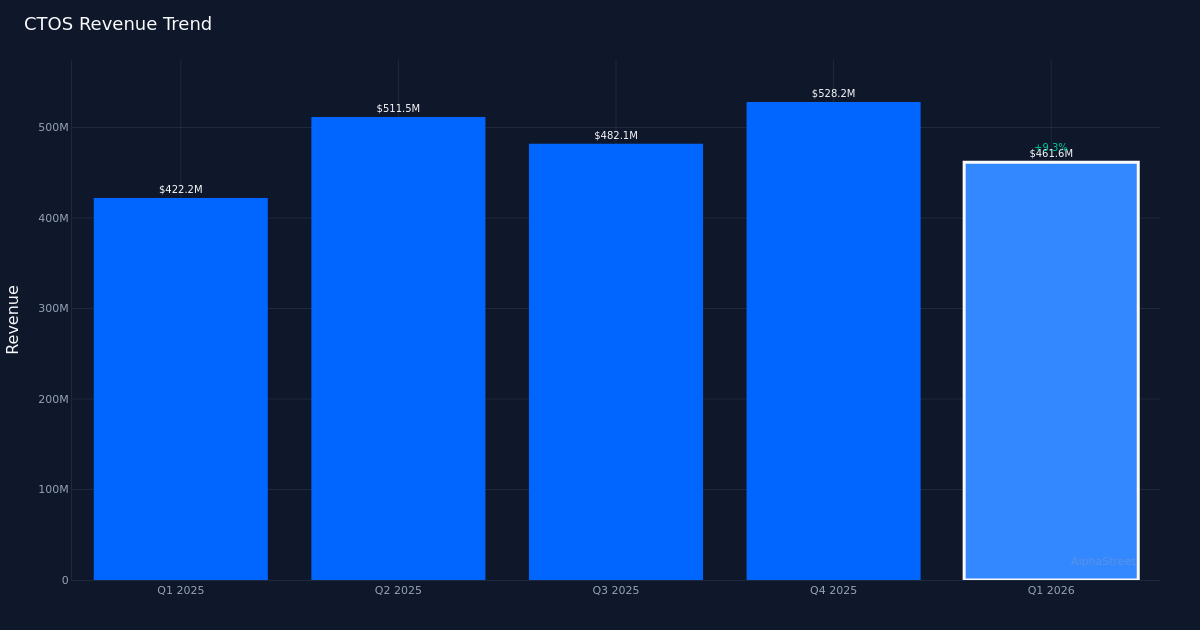

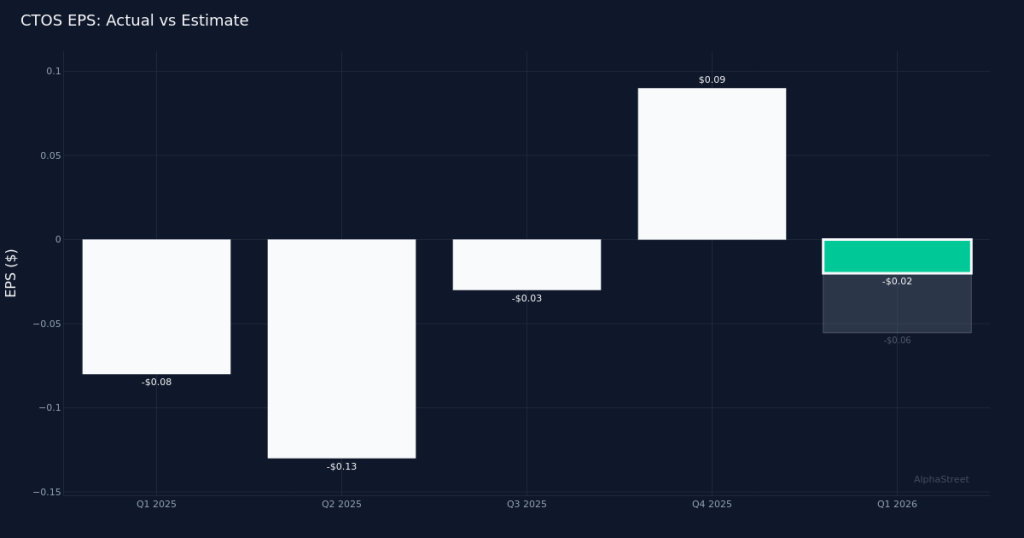

Better-Than-Expected Quarter. Custom Truck One Source, Inc. (NYSE:CTOS) posted a Q1 2026 diluted loss of $0.02 per share, narrower than the $0.06 expected loss. The company generated $461.6M in revenue for the quarter, marking a 9.3% increase from the $422.2M recorded in Q1 2025. The loss of $0.02 per share narrowed 75.0% from the $0.08 loss in Q1 2025, demonstrating meaningful improvement in the company’s profitability trajectory. Shares traded largely unchanged following the report, suggesting investors may have already anticipated the improvement or are waiting for sustained performance.

Revenue-Driven Improvement. The company’s performance reflects genuine operational progress rather than simply cost-cutting measures. The revenue increase to $461.6M from $422.2M year-over-year indicates growing demand for Custom Truck’s rental and leasing services, while the company posted a net loss of $4.1M for the quarter—a significant improvement that speaks to better operating leverage. Fleet utilization reached 81.4% for the quarter, a strong metric for the rental and leasing services industry that demonstrates effective asset deployment. The company operated 1,655,414,000 total OEC at period end at quarter end, representing the scale of assets under management.

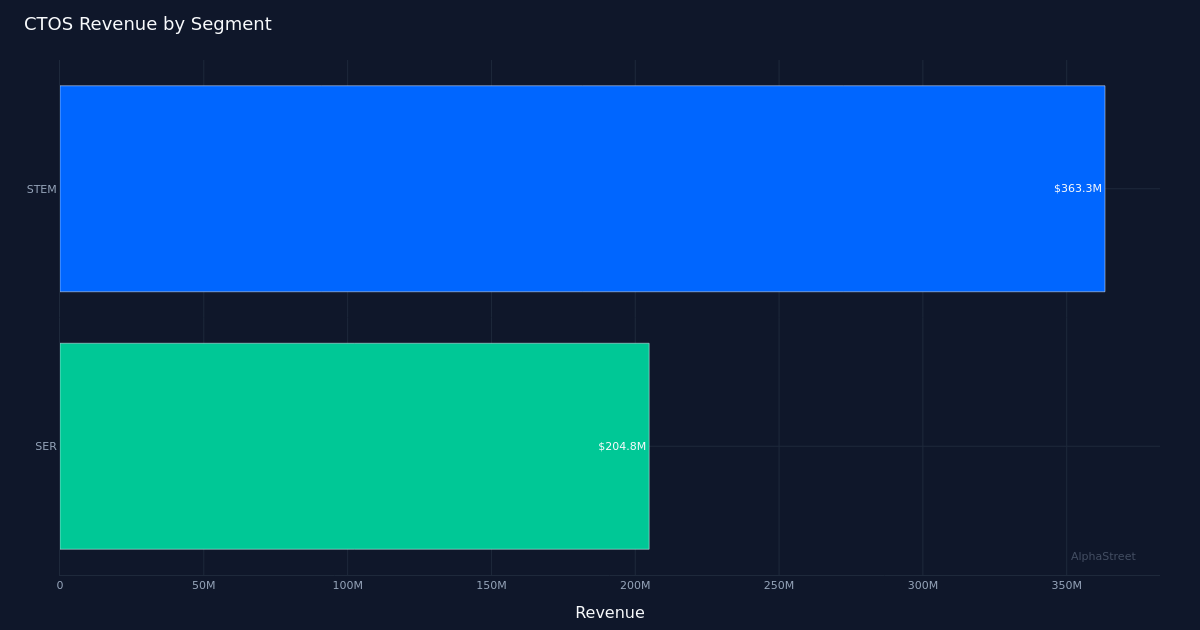

Segment Performance. SER generated $204.8M in revenue for the quarter, representing a substantial portion of total company revenue and highlighting the importance of this division to Custom Truck’s overall results. The segment’s performance underscores the company’s position in serving specialized truck and equipment needs across its customer base. The diversified revenue stream helps insulate the business from volatility in any single end market.

Full-Year Outlook. Management provided full-year revenue guidance of $2.00B, establishing clear expectations for continued growth through 2026. This guidance suggests management expects the momentum from Q1 to carry through the remainder of the year, with the quarterly run rate implying acceleration in coming periods. The guidance provides investors with a framework for evaluating execution as the year progresses and demonstrates confidence in the company’s pipeline and market positioning.

Street Positioning. Wall Street consensus stands at 5 buy, 2 hold, 1 sell, reflecting a generally positive but measured view on the stock. The mixed ratings suggest analysts see opportunity but may want to see sustained profitability before upgrading more aggressively. The narrowing loss and revenue growth should support the bull case, particularly if the company can continue improving margins while growing the top line.

This content is for informational purposes only and should not be considered investment advice. AlphaStreet Intelligence analyzes financial data using AI to deliver fast and accurate market information. Human editors verify content.