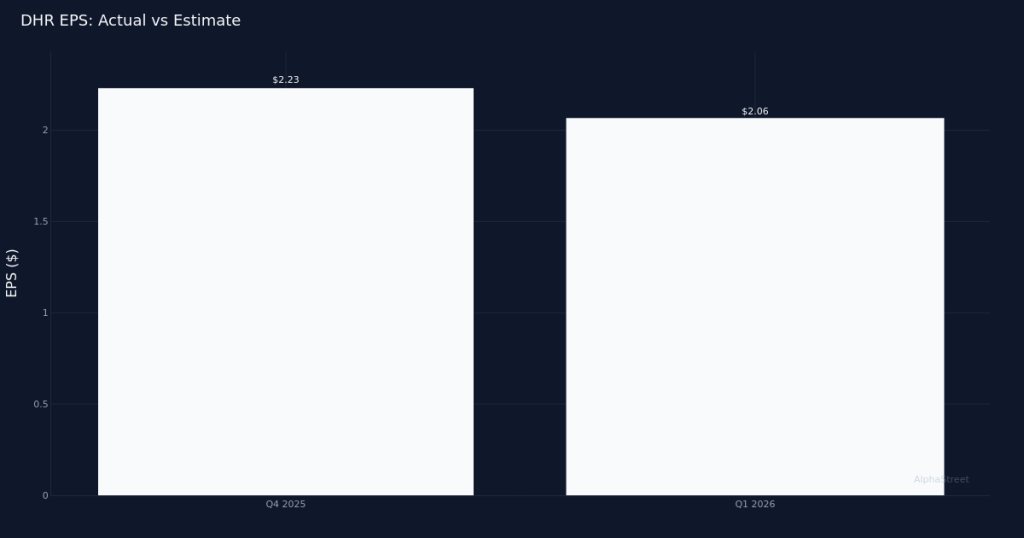

Mixed Quarter. Danaher Corporation (DHR) posted Q1 2026 adjusted EPS of $2.06 on revenue of $5.95B, delivering what appears to be a modest quarter for the diagnostics and research tools giant. Revenue climbed 3.5% from $5.74B in Q1 2025, though the muted stock reaction—shares largely unchanged following the report—suggests investors found little to get excited about in these results. Net income reached $1.03B for the quarter, reflecting the company’s ability to maintain profitability even as growth momentum remains subdued.

Core Growth Concerns. The headline revenue gain of 3.5% masks a more challenging underlying picture, with core revenue growth registering just 0.5% for the quarter. This anemic organic expansion signals that much of the topline improvement came from acquisitions, currency tailwinds, or other non-operational factors rather than fundamental demand strength across Danaher’s portfolio of life sciences and diagnostics businesses. For a company that historically commanded premium valuations based on consistent mid-single-digit organic growth, this deceleration warrants scrutiny. The divergence between reported and core growth suggests the quality of this revenue beat is questionable at best.

Scale Maintained. Danaher operated 60,000 associates worldwide at quarter end, maintaining the workforce infrastructure needed to support its diversified platform spanning biotechnology, diagnostics, and environmental and applied solutions. This headcount stability indicates management isn’t panicking about near-term demand softness, but rather views current conditions as cyclical rather than structural. The company’s continued investment in its global footprint positions it to capitalize when end markets—particularly biopharma manufacturing and clinical diagnostics—return to more normalized growth trajectories.

Full-Year Outlook. Management guided FY 2026 adjusted EPS to a range of $8.35 to $8.55, providing investors with a framework for expectations through year-end. This guidance will be critical for validating whether the Q1 core growth weakness represents a temporary blip or the beginning of a more prolonged slowdown. The Street appears to be taking a wait-and-see approach, as evidenced by the flat stock response and analyst sentiment that shows 15 buy ratings, 4 hold ratings, and no sell recommendations—a generally constructive but not overwhelmingly bullish stance.

Valuation Crossroads. With shares treading water post-earnings, investors seem to be weighing Danaher’s premium multiple against its current growth profile. The company has long traded at a valuation premium to industrial peers based on superior execution and margin expansion through the Danaher Business System, but that premium becomes harder to justify when core revenue growth barely registers positive. The next few quarters will be telling as management works to demonstrate whether this represents a temporary pause or a new normal requiring multiple compression.

This article was generated with the assistance of AI technology and reviewed for accuracy. AlphaStreet may receive compensation from companies mentioned in this article. This content is for informational purposes only and should not be considered investment advice.