The restaurant industry is almost back on track after a challenging period that made food chains revisit their business model with focus on digitization and value-addition. Currently, the companies are experiencing a slowdown due to high inflation and cautious customer spending, but Darden Restaurants, Inc. (NYSE: DRI) maintained stable traffic aided by innovation and affordable prices.

DRI is one of the best-performing Wall Street stocks that stayed unaffected by the market downturn and outperformed the industry quite often. The stock reached its highest-ever value last week, mainly reflecting positive investor sentiment ahead of the upcoming earnings. Darden’s dividend has been increasing at a slow but steady pace and offers a bigger-than-average yield of 3.2%.

Investing in DRI

It is expected that the stock has more room for growth despite the steady gains as the company maintains its strategy of providing quality products at affordable prices. In the most recent quarter, same-restaurant sales and traffic exceeded the industry average. The company’s casual dining brands including LongHorn Steakhouse and Olive Garden Italian Restaurant — the top business segment that accounts for around 50% of total sales — continue to be industry leaders.

Outlook

Being a company that performed well consistently in times of difficulty, Darden can be considered a good investment option. That said, the food industry is often influenced by people’s changing eating habits and menu preferences, and Darden is not immune to that. Also, the management has been investing heavily in initiatives to enhance customer experience, which could have a negative impact on margins at some point, considering the relatively low prices.

Darden is preparing to report fourth-quarter earnings on Thursday before markets open. It is widely expected that earnings increased 12% annually to $2.54 per share in the May quarter. The positive forecast reflects an estimated 6% increase in revenues to $2.77 billion.

Key Numbers

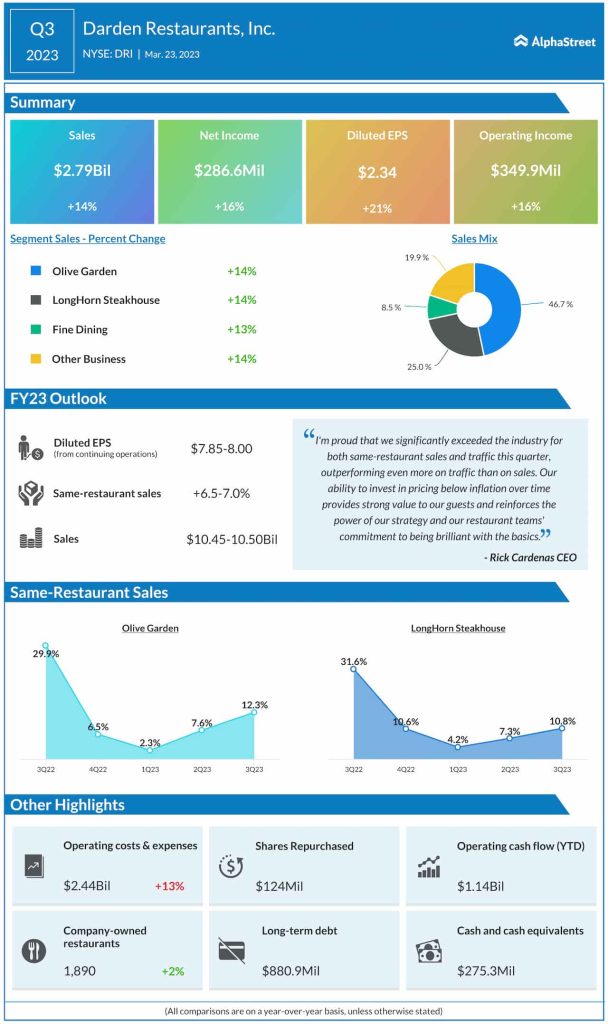

In the trailing two quarters, both earnings and revenues topped expectations and the trend is expected to continue this time because the company has an impressive track record of reporting better-than-expected quarterly results. Sales rose sharply to $2.80 billion in the third quarter when the core Olive Garden segment expanded by 14%. The other three divisions also grew in double digits. As a result, earnings rose 16% annually to $2.34 per share.

From Darden’s Q3 2023 earnings call:

“We significantly exceeded the industry benchmarks for same-restaurant sales and traffic, outperforming more on traffic than we did on sales. We also continued to underprice inflation, resulting in lower overall check growth relative to the industry. Our ability to make this investment and provide strong value to our guests reinforces the power of our strategy, which comes to life through our four competitive advantages and executing our back-to-basics operating philosophy.”

Shares of Darden Restaurants traded slightly higher in early trading on Tuesday, after closing the previous session lower. They have mostly stayed above the 52-week average so far this year.