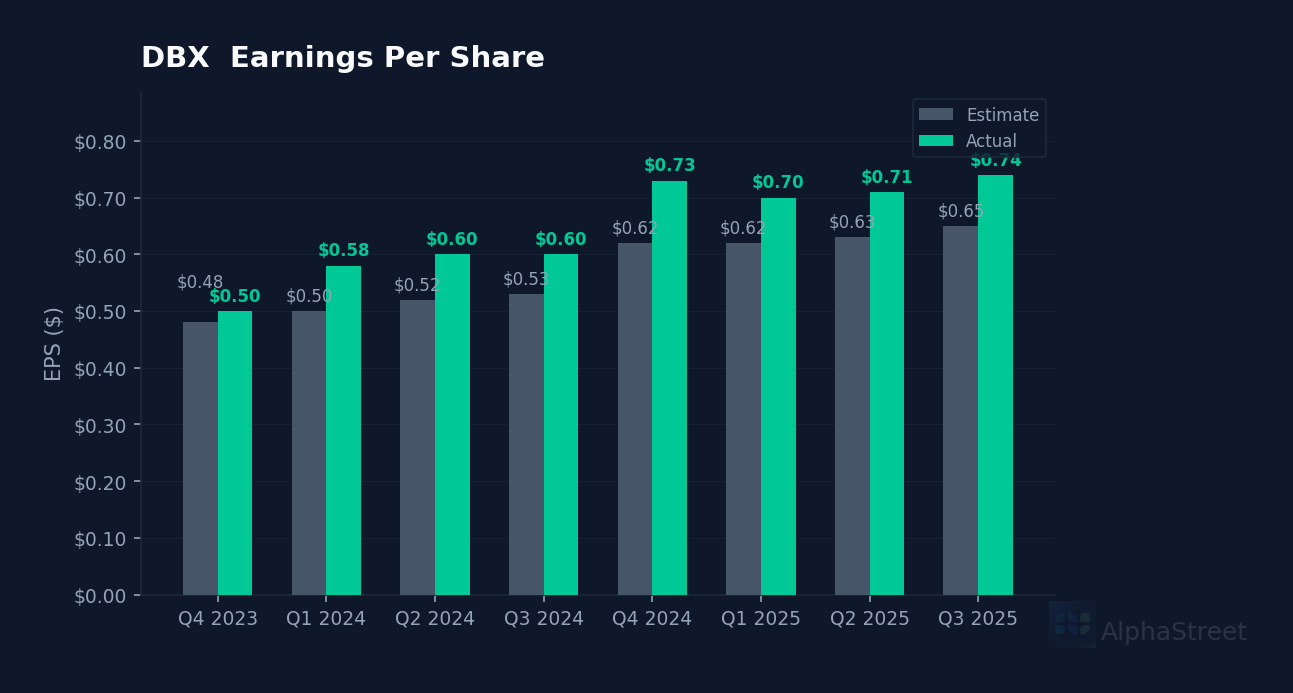

Fifth straight double-digit beat. Dropbox delivered Q4 EPS of $0.74, crushing the Street’s $0.65 consensus by 14.1%—its fifth consecutive quarter of earnings surprises above 12%. Revenue of $2.53B came in flat year-over-year, though sequential growth held at 1.1%. Shares edged up 0.5% to $24.53 in after-hours trading, extending a modest 0.7% gain during regular hours.

The subscription engine misfires. Revenue barely budged from Q4 2024’s $643.6M despite operating margins that remain robust at 27.6%. The company’s trailing twelve-month revenue actually declined 0.7%, a troubling signal for a subscription business that trades at just 13.9x trailing earnings. Management’s success in monetizing existing users—evidenced by that consistent earnings beat streak—masks the harder truth: Dropbox isn’t growing its top line.

Churn improvements carry the quarter. CFO Timothy Regan attributed the Q3 outperformance (which set up this Q4 beat) to “continued improvements in churn and downsell for teams following changes to the cancellation flow.” The company’s individual SKUs overperformed expectations, while DocSend’s advanced data room plan drove double-digit growth in that segment. FormSwift, a recent acquisition, also exceeded internal projections. These tactical wins bought the company time, but they’re playing defense in a market where Microsoft, Google, and Box continue to bundle storage with broader productivity suites.

Valuation screams value trap. At $24.58, Dropbox trades 13% below its 50-day average of $26.86 and 15% under its 200-day average of $28.41. The stock has surrendered 17% since peaking near $29.90 in late November. With a forward P/E of just 8.2x and analyst price targets at $28.33, the discount looks compelling—until you consider that negative stockholders’ equity of $1.53B (worsening from -$752M a year ago) reflects aggressive buybacks that have cratered the balance sheet. The company generated $502M in net income through nine months of 2025, but it’s returning capital faster than it’s growing revenue.

The AI pivot remains unproven. CEO Drew Houston has positioned Dropbox’s AI search and organization features as the company’s path to renewed growth, but those capabilities haven’t yet translated into accelerating revenue. With the stock down 16% from its February 2025 peak and competitors embedding AI throughout their ecosystems, Dropbox needs to show that its focused file-management approach can compete against integrated platforms. The margin profile remains enviable—operating margins of 27.6% and profit margins near 20%—but investors are pricing in stagnation, not transformation.

This article was generated using AlphaStreet’s proprietary financial analysis technology and reviewed by our editorial team.