Shares of Delta Air Lines (NYSE: DAL) were down 2% on Thursday despite the company delivering better-than-expected earnings results for the third quarter of 2023. The airline said it was seeing strong demand for travel continuing into the fourth quarter and expects revenues to grow for the period. However, the company reduced its earnings outlook for the full year. The stock has gained 7% year-to-date.

Quarterly performance

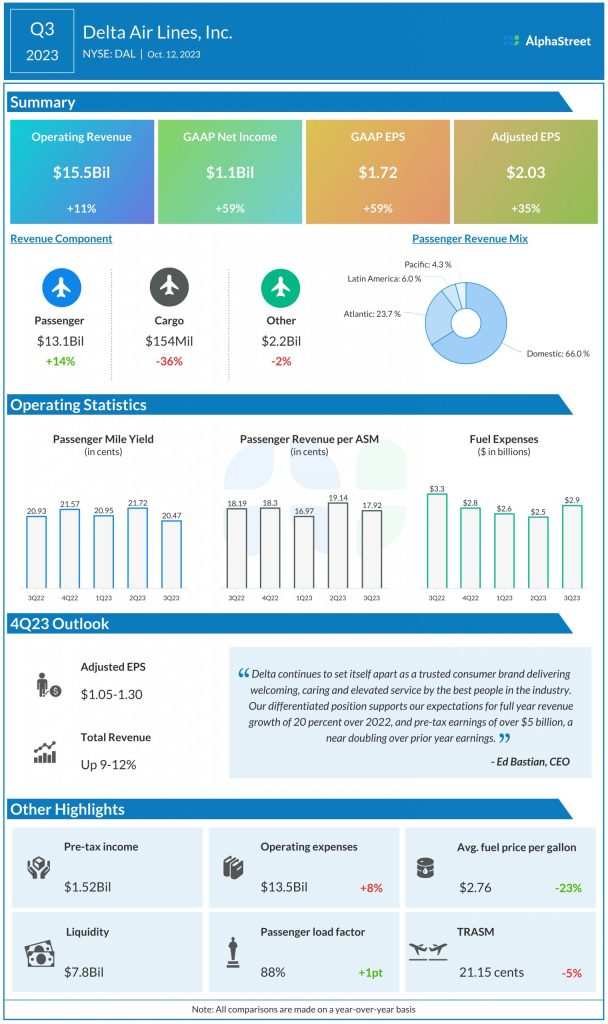

Delta’s operating revenues increased 11% year-over-year in the third quarter of 2023 to $15.5 billion, beating estimates of $14.5 billion. Adjusted operating revenues increased 13% to $14.6 billion. GAAP net income rose 59% to $1.1 billion, or $1.72 per share, compared to last year. Adjusted EPS grew 35% to $2.03, beating consensus targets of $1.94.

Demand trends

In the third quarter, Delta saw passenger revenue grow by 14% while cargo fell 36%. Total revenue per available seat mile (TRASM), or unit revenue, was down 5% YoY. Passenger unit revenue (PRASM) was down 1.5% YoY. Capacity was up 16% in Q3. Passenger load factor stood at 88%.

The airline is seeing stable demand for domestic travel, with domestic passenger revenue increasing 6% YoY in Q3. Domestic unit revenue dropped 4%. The company continues to see improvement in business travel helped by return-to-office initiatives. Delta stated that as per its corporate surveys, a significant majority of companies expect their travel volumes to increase or stay the same in Q4 and into 2024.

Delta is seeing momentum in international travel as well, with international passenger revenue rising 35% YoY in Q3. The company saw robust double-digit revenue growth across all three of its international entities during the quarter, and it expects to end the year with strong profits across these three divisions.

Outlook

Delta is seeing strong demand for travel continuing into the fourth quarter of 2023 and expects revenue for the period to grow 9-12% from the same quarter a year ago. Total revenue is expected to range between $13.4-13.8 billion in Q4.

Total unit revenue is expected to decline 2.5-4.5% in Q4. Capacity is estimated to be up 14-15% YoY. EPS is expected to range between $1.05-1.30 in the fourth quarter. Operating margin is expected to range between 9-11%. CASM-Ex is expected to be flat to up 2% YoY. Fuel price for the December quarter is estimated to be $2.90-3.20 per gallon.

Delta revised its guidance for the full year of 2023 and now expects revenue to be up approx. 20% YoY and EPS to range between $6.00-6.25. This compares to the previous outlook of revenue growth of 17-20% and EPS of $6-7. Operating margin is now expected to be around 11.5% versus the earlier expectation of greater than 12%.