Delta Air Lines is preparing to report fourth-quarter earnings, with investors closely watching how the carrier navigated ongoing cost pressures and evolving demand trends. The company’s resilient performance in 2025 boosted investor confidence, and the stock has made steady gains since mid-year. Delta is leaning on its pricing power and disciplined cost management to sustain recent momentum.

Estimates

In a recent statement, management said it expects fourth-quarter earnings per share to be in the range of $1.60 to $1.90, and operating margin between 10.5% and 12%. The earnings forecast is above $1.55 per share Wall Street forecasts, compared to $1.29 per share in Q4 2024. Analysts are looking for revenues of $15.77 billion for the December quarter, representing a 1.4% year-over-year increase. The company is expected to report fourth-quarter earnings on January 13, before the opening bell.

Delta shares have grown around 40% in the past six months and set a new record last week. The stock outperformed the S&P 500 during that period and is trading above its 52-week average price of $56.13. Analysts are generally optimistic about DAL’s prospects, with the majority maintaining Buy ratings as of this week. The momentum is expected to continue in fiscal 2026, aided by healthy demand, particularly in the domestic market, thanks to the company’s continued focus on the premium segment.

Key Metrics

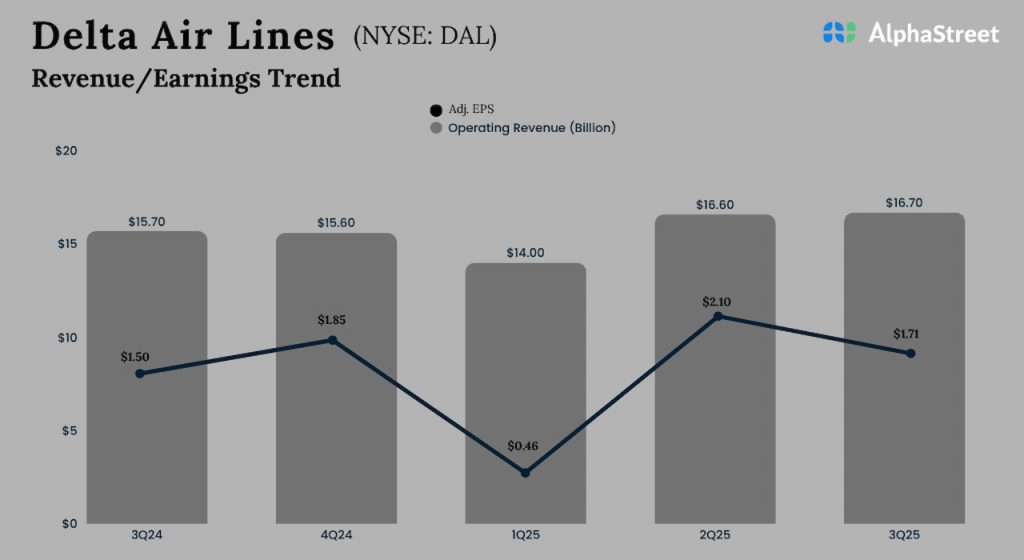

For the third quarter of fiscal 2025, Delta reported operating revenues of $16.7 billion, higher than $15.7 billion in the prior-year quarter. Adjusted earnings per share rose to $1.71 in the September quarter from $1.50 a year earlier. Both revenues and the bottom line exceeded Wall Street’s expectations, after beating in each of the trailing three quarters. On a reported basis, net income was $1.42 billion or $2.17 per share, vs. $1.27 billion or $1.97 per share in Q3 2024.

Delta’s chief executive officer, Edward Herman Bastian, said in the Q3 earnings call, “Structural change has taken hold across the industry as unprofitable flying is rationalized and carriers not earning their cost of capital adjust strategies to prioritize returns. Against this backdrop, we expect to deliver a double-digit operating margin again in the December quarter, with earnings comparable to what we earned in the September quarter. This would be at or above our all-time fourth quarter earnings performance. This brings our outlook for full-year earnings to approximately $6 per share, which is in the upper half of our July guidance range.”

Flying High

For fiscal 2025, Delta leadership predicts adjusted earnings to be approximately $6 per share, which is above analysts’ consensus estimates, and free cash flow between $3.5 billion and $4 billion. It continues to advance its fleet renewal program and targets around 40 aircraft deliveries through 2026. The company stands to benefit from lower interest rates when tapping capital markets to execute growth plans. Also, the shift away from traditional pricing patterns toward an AI‑driven dynamic pricing model is expected to optimize revenue and strengthen overall yield.

On Tuesday, Delta shares opened at $69.49 and dropped slightly in early trading. While the stock has gained around 8% in the past 30 days, the momentum moderated in recent sessions.