AlphaStreet Newsdesk powered by AlphaStreet Intelligence

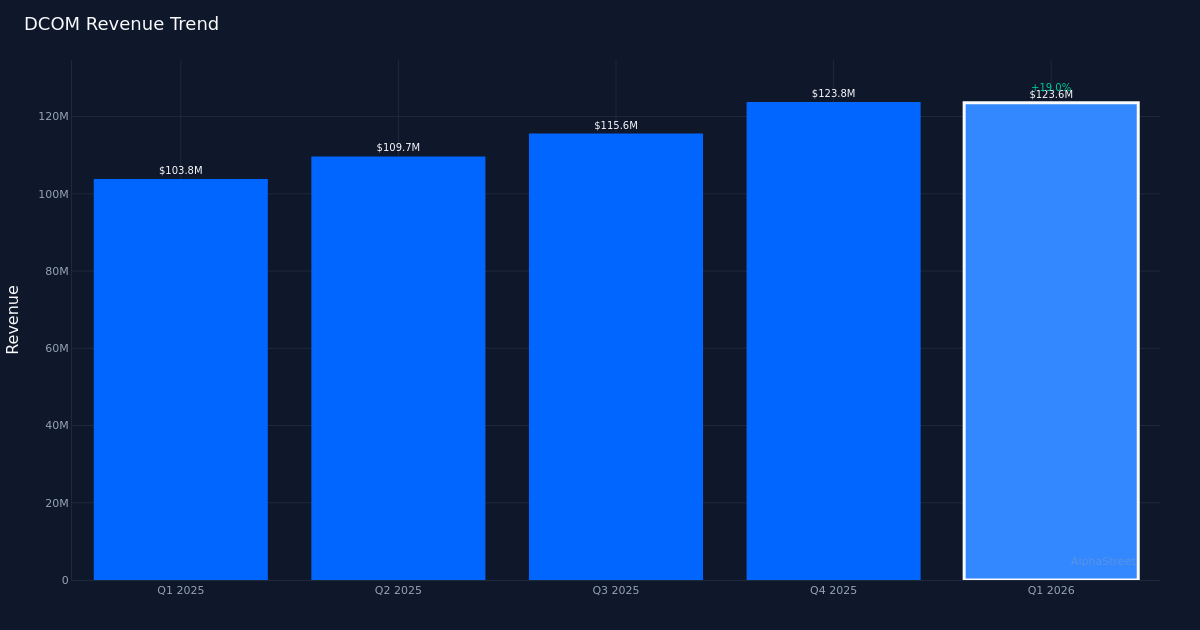

Dime Community Bancshares (DCOM) delivered a paradoxical Q1 2026 result, missing analyst expectations by 5.1% with adjusted EPS of $0.74 versus the $0.78 consensus, yet posting strong year-over-year fundamentals that propelled shares up 4.3% as investors looked past the near-term miss to focus on the underlying trajectory. The regional bank’s $123.6M in revenue represented 19.0% growth year-over-year, while net income of $34.6M translated to a robust 28.0% net margin, suggesting quality earnings generation despite the headline disappointment.

The earnings quality story here is unambiguously positive, with margin expansion validating revenue growth as genuine operating improvement rather than top-line inflation masking deteriorating economics. Net margin improved 4.2 percentage points from 23.8% in Q1 2025 to 28.0% in the current quarter, while operating margin reached 39.3% on pre-tax income of $48.5M. This simultaneous expansion of both revenue and profitability metrics indicates Dime is converting growth into bottom-line results effectively. Management highlighted that “the growth in EPS was driven by record total core revenues of $124 million,” reinforcing that the 29.8% year-over-year EPS increase from $0.57 to $0.74 stems from fundamental business momentum. The company’s net interest margin expanded 3.2%, a critical indicator for banks that compressed margins have been squeezing profitability across the regional banking sector.

Sequential revenue analysis reveals a bank approaching a plateau after a strong growth phase, with Q1 revenue of $123.6M essentially flat against Q4’s $123.8M. The four-quarter trend shows clear acceleration through 2025—Q2’s $109.7M climbing to Q3’s $115.6M, then jumping to Q4’s $123.8M—before stabilizing in the current quarter. This deceleration in sequential growth, even as year-over-year comparisons remain robust at 19.1%, suggests Dime may be reaching a natural ceiling at current deployment rates. Net income tells a similar story: $34.6M in Q1 2026 nearly mirrors Q4 2025’s $34.5M, after climbing from $27.9M in Q2 2025 and $26.6M in Q3 2025. The sequential stall warrants attention, particularly given the miss against expectations.

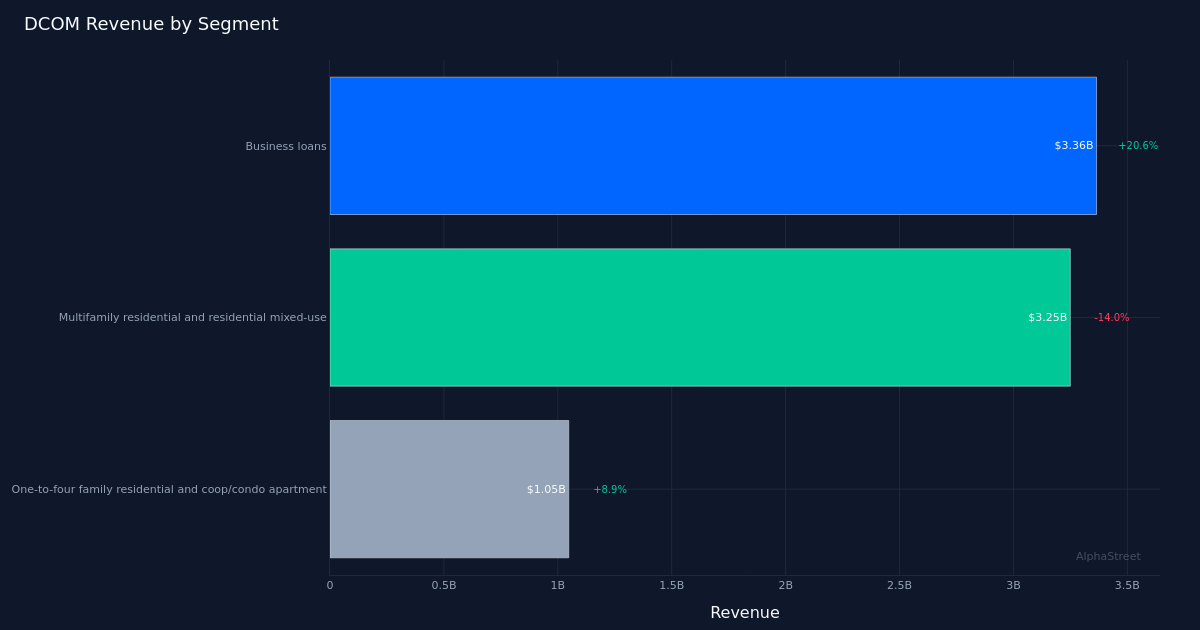

Segment dynamics reveal a strategic portfolio rotation away from multifamily residential exposure toward business lending, with material implications for both risk profile and growth sustainability. Business loans grew to $3.36B with 20.6% growth. This diversification move is partially offset by deliberate retrenchment in multifamily residential and residential mixed-use loans, which declined 14.0% to $3.25B. Management explicitly acknowledged this shift, noting “this quarter we had $170 million of multifamily payoff and $90 million of CRE, investor CRE payoff.” The one-to-four family residential and coop/condo apartment segment showed moderate 8.9% growth to $1.05B, suggesting stable demand in core retail real estate lending. This portfolio rebalancing appears intentional rather than market-driven, with management indicating future CRE growth constraints: “once we get to that 350% and we’ve got a $2.7 billion, $2.8 billion investor CRE portfolio that probably grows at $200 million on an annual basis just using a 5% to 6% growth rate.”

The deposit gathering momentum provides crucial fuel for future loan growth, with management emphasizing that “year-over-year our core deposit growth was $1 billion.” Against total assets of $15.00B, adding $1 billion in core deposits represents meaningful funding base expansion that reduces reliance on wholesale funding and positions the bank to sustain lending growth even as certain segments contract. This deposit growth is particularly valuable in an environment where regional banks have faced deposit flight pressures, suggesting Dime’s franchise strength in its core New York metropolitan market.

The stock’s 4.3% post-earnings rally to $37.34 despite the EPS miss signals investor comfort with the strategic direction and underlying fundamentals, though the zero-for-one recent beat record indicates expectations calibration issues. The market appears willing to overlook near-term estimate misses when margin expansion and strategic repositioning tell a constructive longer-term story. However, consecutive misses would likely erode this goodwill, making the Q2 execution critical for maintaining credibility with the investment community.

The 5.1% earnings miss warrants scrutiny given it follows a pattern of missing estimates in the most recent quarter, suggesting either conservative internal forecasting that management is communicating to analysts or execution challenges that prevent the bank from meeting its own implied guidance. The combination of strong year-over-year growth but sequential flattening indicates Dime may be entering a consolidation phase where digesting recent expansion takes priority over continued aggressive growth. The margin expansion provides breathing room for this consolidation, but investors will need visibility into whether the sequential plateau is temporary or represents a new normalized run rate.

This content is for informational purposes only and should not be considered investment advice. AlphaStreet Intelligence analyzes financial data using AI to deliver fast and accurate market information. Human editors verify content.