DocuSign, Inc. (NASDAQ: DOCU) is one of the many tech companies affected by falling customer demand amid economic uncertainties and rate hikes. The company embarked on a cost-reduction drive and laid off hundreds of workers in recent months as part of its efforts to streamline the business.

The earnings and revenue performance of the San Francisco-headquartered e-signature solutions provider has remained stable in recent years. But the stock has been in a downward spiral since hitting an all-time high around two years ago. For shareholders, there has not been much to cheer about as the stock remained almost stagnant in the past twelve months.

Valuation

While the stock price is expected to improve this year, analysts in general are cautious in their outlook for the company due to uncertainties related to profitability and near-term prospects of the business. That said, being an innovative technology company, DocuSign has what it takes to create long-term shareholder value. The company banks on its first-mover advantage to gain an edge over competitors and tap into new opportunities in the area of e-agreements.

DocuSign’s CEO Allan Thygesen said at the last earnings call: “Today, e-sign signs provide an online replica of a static document. While that is a huge improvement in convenience and productivity for senders and signers, it’s hardly the endpoint. Just like creating digital copies of maps, or recorded music was the beginning of a re-imagination of long-established categories, fundamentally altering creation, distribution, and use. Our goal is to turn flat agreements into structured data that can be used to make intelligent decisions,”

Rightsizing

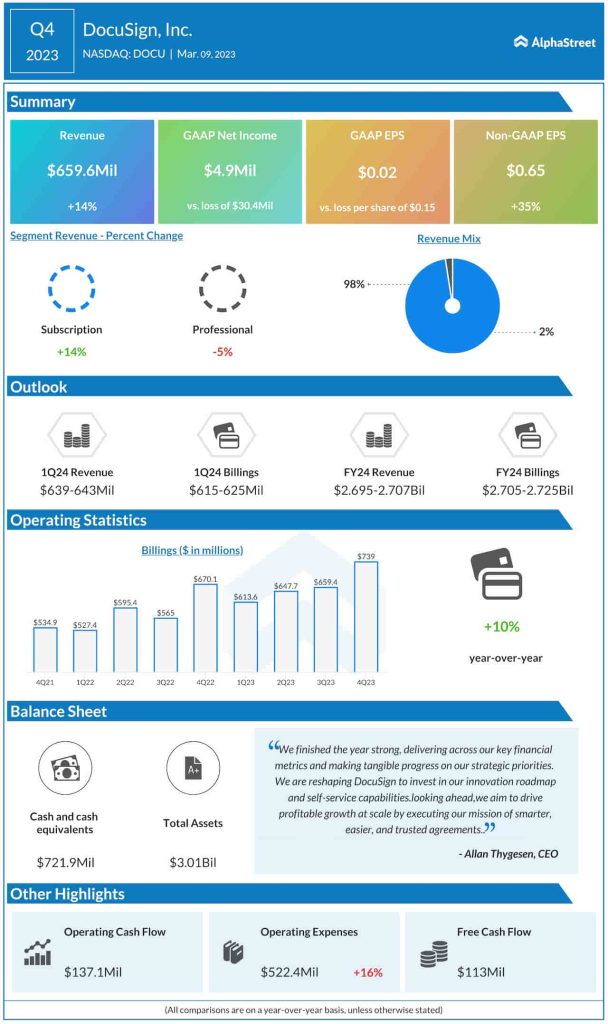

Earlier this year, the company announced a new round of headcount reduction after laying off around 9% of its workforce last year. The move is part of the management’s efforts to position the company for profitable growth while freeing up resources for investments. In the most recent quarter, operating cash flow increased more than 50% year-over-year to about $137 million.

When DocuSign reports first-quarter 2024 results on June 8 after the closing bell, the market will be looking for earnings of $0.55 per share, which is up 45% from the year-ago quarter. It is estimated that revenues increased 9% annually to $641.8 million in the April quarter. The revenue forecast is broadly in line with the management’s guidance. It is expected that the results would include impairment charges related to the recent layoffs.

Key Numbers

At $660 million, fourth-quarter revenues were up 14% from last year and above the consensus estimates. Driven by the top-line growth, adjusted profit climbed 35% to $0.65 per share. On a reported basis, net income was $4.9 million or $0.02 per share, compared to a loss last year. The bottom line also exceeded estimates, as it did in each of the trailing four quarters. Total billings were $739 million, up 10%. As per the company’s most recent guidance, total billing is expected to be in the range of $2.71 billion to $2.73 billion in the whole of 2024.

DocuSign’s stock traded lower in early trading on Wednesday and stayed below its 52-week average. It has gained 17% in the past six months.