The financial performance of Domino’s Pizza, Inc. (NYSE: DPZ) has been broadly stable in the recent past despite the inflation-induced strain on consumer’s spending power. While sales benefitted from its reward loyalty program and continued menu innovations, the fast-food chain’s operations outside the US came under pressure from inflation and unfavorable market conditions.

In the past two months, the pizza giant’s stock mostly traded sideways, after retreating from a two-and-half-year high. The last closing price is almost in line with the value seen at the beginning of the year. Over the past twelve months, the stock gained around 12%.

Q3 Report Due

It is estimated that Dominos’ third-quarter earnings decreased to $3.62 per share from $4.18 per share last year. Meanwhile, market watchers see a modest increase in Q3 revenues to $1.1 billion. The report is expected to be out on Thursday, October 10, at 6:05 am ET. The company’s earnings consistently surpassed Wall Street’s forecasts in the past seven quarters, while revenues missed or matched expectations during that period.

The company has constantly innovated its menu offerings, such as the recent launch of New York-style pizza with a thin and foldable crust. It has also rolled out a new service program that allows customers to receive their orders at locations like beaches and parks. While exuding confidence of being on track to achieve the target of $170,000 average US franchise store profit this year, the management said it may fail to meet the store growth goal in the international market due to weakness in Domino’s Pizza Enterprises, its largest franchise outside the US.

Outlook

Recently, Domino’s announced heavy discounts on items ordered online for a specific period this month, on the occasion of National Pizza Month. For the long term, from 2024 to 2028, the management expects annual global retail sales to grow more than 7% and sees an operating profit growth of above 8%, excluding the impact of foreign currency. Meanwhile, higher operating costs and wages might remain a drag on margins, partially offsetting benefits from the management’s efforts to reduce costs and increase operational efficiency.

While interacting with analysts after Q2 earnings, Dominos’ CEO Russell Weiner said, “As I shared on our last earnings call, in 2024 we are rolling out a new service program, we’re calling more delicious operation. This is a series of three product training sprints focused on our dough, how we build and make our products, and then how we cook. In Q1, we embarked on our first Sprint, which focused on our dough, and are now rolling out our second sprint around ingredients and product built.”

Stable Sales

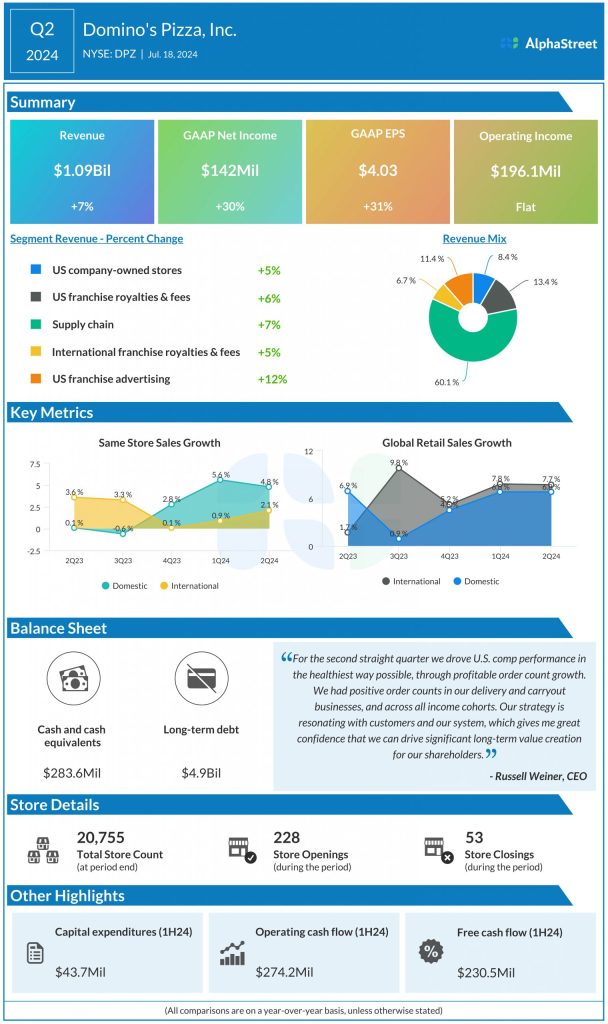

In the second quarter, total revenues increased 7% year-over-year to $1.09 billion. US same-store sales rose 4.8% during the three months and international same-store sales grew by 2.1%. The top line benefited from an increase in supply chain revenues, US franchise advertising revenues, and franchise royalty fees. Net income increased about 30% from last year to $142 million or $4.03 per share in the June quarter. Order counts across income groups, both in delivery and carryout, have been positive during the quarter.

Shares of Domino’s traded below their 52-week average price in recent weeks. On Wednesday, the stock opened flat and traded lower in the early hours of the session.