Restaurant chains that offer home delivery were in high demand during the pandemic as a lot of people relied on them when movement restrictions were imposed, and Domino’s Pizza, Inc. (NYSE: DPZ) is one such company that benefited from the lockdown-indued sales boom. But when normalcy returned, sales also returned to normal levels.

The fast food company’s muted top-line performance this year has taken a toll on the stock, which traded at three-year lows most of the first half, before rebounding a few months ago. However, the company maintains stable profitability aided by higher franchise fees and menu prices, with margins benefiting from the improving inflation environment. That, together with the management’s efforts to enhance sales in the domestic market, should enable the company to create good shareholder value. So, prospective investors can consider adding DPZ to their watchlists.

Growth Plan

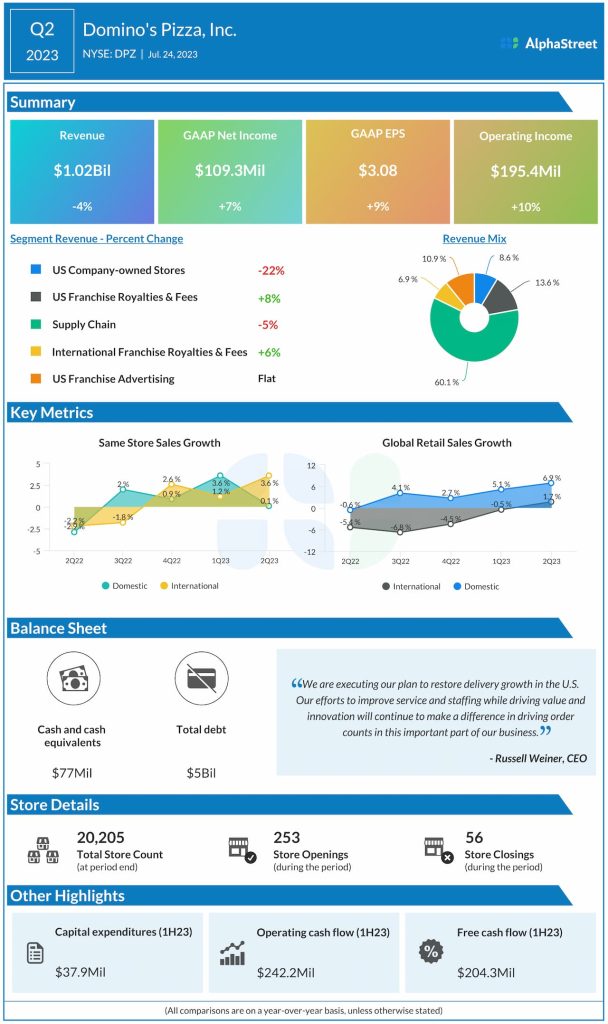

Right now, the key priorities for the world’s largest pizza chain include restoring delivery growth in the domestic market and driving order volumes by enhancing customer experience and through innovation. The company recently partnered with Uber Eats to serve delivery customers, whose number is growing steadily. Complementing the growth strategy, Domino’s opened an impressive 253 new stores in the second quarter and used around $38 million for capital spending in the first half.

Dominos’ CEO Russell Weiner said, “Our extensive evaluation indicates that by participating in the aggregator marketplace, we’ll drive net incremental orders over the long term by tapping into a new group of consumers. In addition, our contractual agreement has secured the protections that we require to maintain control over our customer data and assess the incrementality of the platform. And most importantly, orders placed on the Uber Eats platform will be delivered by Domino’s delivery experts.”

The Market

The fast-food market is becoming highly competitive, and it looks like Domino’s has to compete effectively with its peers including Chipotle Mexican Grill and McDonald’s to retain market share. The company’s same-store sales in the U.S. have not been encouraging lately. That calls for further expansion of the store network but it might not be sustainable beyond a certain limit, especially in a market that is getting crowded.

Domino’s will be releasing its third-quarter report on October 12, before markets open. Analysts’ estimates indicate that the trend seen in the second quarter continued this time. The consensus earnings estimate is $329 per share, which is up 18% from the prior-year quarter. Wall Street is looking for revenues of $1.05 billion, which represents a 1.2% decline.

Q2 Outcome

In the second quarter of FY23, sales at the US Company-owned Stores, which account for around 60% of total revenues, declined 22%. As a result, the topline dropped 4% year-over-year to $1.02 billion. International same-store sales rose 3.6% annually, while domestic sales remained almost unchanged. Earnings increased 9% to $3.08 per share and topped expectations for the third consecutive quarter, while revenues missed each time.

Shares of Domino’s traded down 5% towards the end of Friday’s session. After suffering losses most of the week, the price matched the 52-week average.