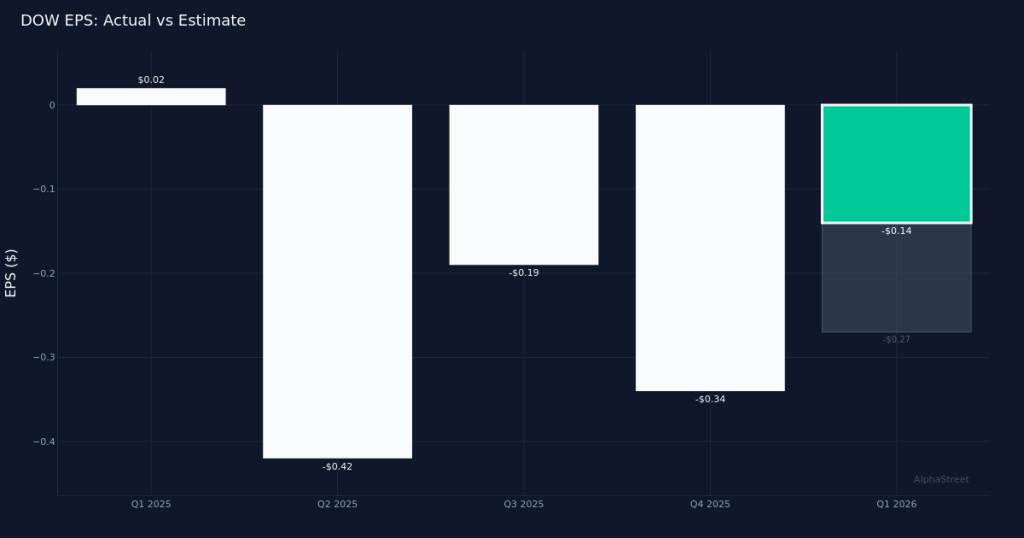

Better-than-feared results. Dow Inc. (NYSE:DOW) posted a Q1 2026 operating loss per share of $0.14, coming in 48.1% narrower than the $0.27 loss analysts had anticipated, providing a glimmer of hope for the embattled chemicals giant. The company generated $9.79B in revenue for the quarter, though that figure represents a 6.0% decline from the $10.43B recorded in Q1 2025. Shares rose 1.3% to $38.81 following the release, suggesting investors are focusing on the loss improvement rather than the persistent top-line headwinds.

Volume pressures persist. The 6.0% revenue decline reflects ongoing demand challenges across Dow’s key end markets, with volume down 2.0% for the quarter. The bottom line showed a net loss of $445.0M, underscoring the magnitude of cyclical pressures facing the industry. Packaging & Specialty Plastics, historically the company’s largest segment, led with $4.92B in revenue but fell 7.0% year-over-year, highlighting weakness in consumer-facing applications that have been slow to recover from the prolonged destocking cycle.

Cost discipline evident. The significantly narrower-than-expected loss suggests management’s restructuring initiatives are gaining traction, though investors should scrutinize whether the improvement stems from sustainable operational efficiency or transient cost cuts. With 34,600 employees at quarter end, the company has maintained workforce discipline while navigating the downturn. The quality of this beat hinges on whether margin improvement can persist as volume headwinds eventually ease—a critical distinction between genuine operational improvement and temporary cost management.

Cautious Wall Street stance. Analyst sentiment reflects the uncertainty surrounding Dow’s recovery trajectory, with consensus standing at 7 buy ratings, 13 holds, and 1 sell. This balanced distribution suggests the Street is adopting a wait-and-see approach, likely wanting confirmation that demand stabilization is sustainable before upgrading positions. The modest stock price reaction—up just 1.3%—reinforces that institutional investors view this as a step in the right direction rather than a definitive inflection point.

Sector headwinds remain. The chemicals industry continues grappling with excess capacity, particularly in polyethylene and other commodity plastics where Chinese production has flooded global markets. Dow’s ability to narrow its loss while operating in this challenging environment demonstrates resilience, but the 7.0% decline in its largest segment signals that pricing power remains elusive. The durability of any margin recovery will depend on whether demand growth can outpace capacity additions across the industry.

This article was generated with the assistance of AI technology and reviewed for accuracy. AlphaStreet may receive compensation from companies mentioned in this article. This content is for informational purposes only and should not be considered investment advice.