In recent years, semiconductor company Advanced Micro Devices, Inc. (NASDAQ: AMD) constantly strengthened its portfolio through new products and acquisitions. Currently, it is focused on integrating artificial intelligence technology into the products. However, recent data indicate that the AI initiative might need a push, considering the high demand for AI-supported GPUs from leading enterprise and cloud customers.

This week, the company’s share price hovered close to the levels seen at the beginning of the year, though it hit an all-time high in early March. The stock is losing momentum ahead of the earnings but stays above the long-term average. AMD has a history of bouncing back quickly every time it slides, and the stock has what it takes to return to the growth path and continue creating shareholder value.

Q2 Report on Tap

AMD is expected to publish its second-quarter report on July 30, at 4:15 pm ET. The consensus earnings estimate is $0.68 per share, on an adjusted basis, compared to $0.58 per share a year earlier. Q2 revenue is seen increasing 6.8% from last year to $5.72 billion. Interestingly, in the past two quarters, earnings and revenues matched analysts’ estimates, after four consecutive beats.

The company has effectively navigated recent geopolitical tensions and economic uncertainties. Currently, it is busy building and implementing AI solutions, and those efforts got a boost with the acquisition of Silo AI earlier this month. AMD bets on its popular MI300 GPU to drive profitability as the chip is in high demand and competes with Nvidia’s H100. However, the company lags behind Nvidia in the AI chip race. As far as near-term profitability is concerned, continued pressure on margin and inventory buildup is a concern.

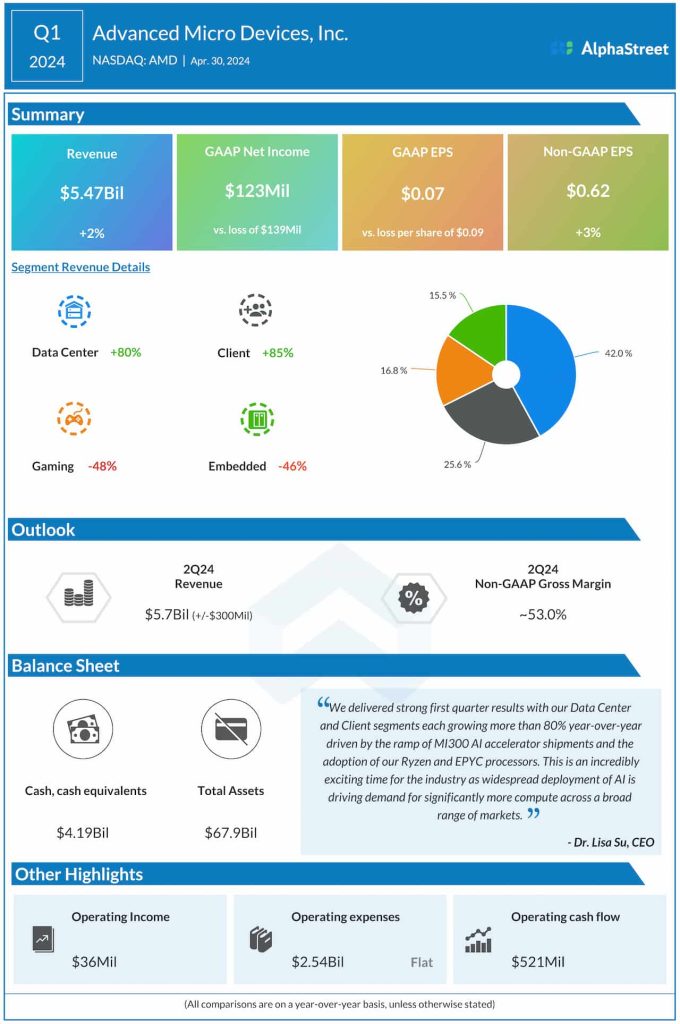

Modest Q1

For the first quarter of 2024, the tech firm reported modest results – revenue increased 2% year-over-year to $5.47 billion and adjusted profit moved up 3% to $0.62 per share. Revenue growth of more than 80% in the Data Center and Client segments, which together account for about 65% of the total, was partially offset by weakness in the Gaming and Embedded divisions. For the second quarter, the management expects revenue to be around $5.7 billion and adjusted gross margin of about 53%.

AMD’s CEO Lisa Su said at the Q1 earnings call, “Looking ahead, we’re very excited about our next-gen Turin family of EPYC processors featuring our Zen five core. We’re widely sampling Turin, and the silicon is looking great. In the cloud, the significant performance and efficiency increases of Turin position us well to capture an even larger share of both first- and third-party workloads. In addition, there are 30% more Turin platforms in development from our server partners compared to fourth-gen EPYC platforms, increasing our enterprise SAM with new solutions optimized for additional workloads.”

Extending the recent downtrend, AMD’s stock traded lower on Wednesday afternoon after opening the session slightly above $150.