After generating record-high revenues in the last quarter, American Express Company (NYSE: AXP) is poised to reveal its third-quarter numbers this week. This year, effective cost management and the increasing scale of the business have enabled the company to maintain momentum despite the slower growth environment.

Earlier this month, the company’s stock peaked and traded around $275. That is sharply above its 52-week average price. The value nearly doubled in the past 12 months, and the stock appears to be expensive at the current market price. However, the high valuation should not be a problem for long-term investors, given the company’s healthy financials and upbeat prospects. It is worth noting that American Express has a good track record of operating successfully, taking advantage of its unique business model. The company acts as both a card issuer and payment network, unlike others like Mastercard which only processes transactions.

Q3 Report Due

When the New York-headquartered credit card giant reports third-quarter earnings on Friday, market watchers will be looking for adjusted earnings of $3.28 per share, which is broadly in line with the $3.3/share profit the company generated in the year-ago quarter. Meanwhile, Q3 revenue is expected to grow 8.4% year-over-year to $16.67 billion. The report is slated for release on October 18, at 7:00 am ET.

The company’s healthy cash flow allows it to invest in marketing initiatives and other strategic areas – targets $6 billion in marketing spending in FY24. The management sees continued strong spending by affluent customers on entertainment, travel, and dining — focus areas that differentiate American Express from other credit card companies. Since the spending habits of its premium customers are not materially impacted by economic uncertainties and inflation, the company mostly stays resilient to such challenges.

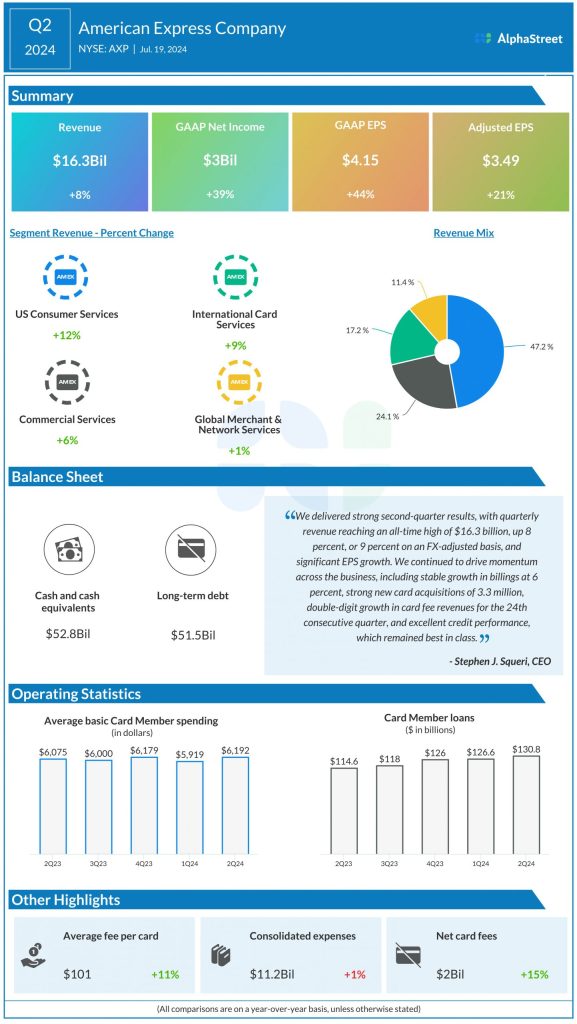

Stable Momentum

In the June quarter, consolidated revenues, net of interest expense, moved up 8% annually to $16.3 billion. The growth was driven by higher net interest income, an increase in card member spending, and continued strong card fee growth. US Consumer Services, which represents nearly 50% of total revenues, expanded 12% from last year. That translated into a 21% surge in adjusted earnings to $3.49 per share in the second quarter.

From American Express’ Q2 2024 earnings call:

“As we’ve seen through the first half of the year, our core business continues to generate strong momentum, even against a backdrop of a slower growth environment. The continued momentum we’re generating reflects the earnings power of our business model which is driven by several interrelated factors, including, first and foremost, the quality of our loyal premium customer base, plus the increasing scale of our business, a well-controlled expense base, the success of the strategic investments we’re making to enhance Amex membership, and our talented colleagues around the world.”

Profit

Unadjusted net income increased 39% to $3 billion and EPS rose 44% to $4.15 in the second quarter compared to last year. Earnings beat estimates while revenue missed expectations. Meanwhile, the Amex leadership raised its full-year 2024 earnings guidance to $13.30-13.80 per share from the previous range of $12.65-13.15 per share. It continues to expect full-year revenue growth between 9% and 11%.

AXP is up 47% since the beginning of the year, constantly maintaining an upward momentum and often outperforming the market. The stock traded slightly lower on Monday morning.