Semiconductor technology company Applied Materials, Inc. (NASDAQ: AMAT) is scheduled to release first-quarter results on Thursday after the closing bell. Being a leading provider of semiconductor fabrication equipment and electronic display solutions, the company is well-positioned to benefit from the AI-driven upswing in the global semiconductor market.

Stock Gains

The Santa Clara-headquartered tech firm’s shares have been in an upward spiral for over a year, and they climbed to a record high last week. Though the stock has retreated from the peak it continues to stay above the long-term average, ahead of the earnings. Considering AMAT’s relatively high valuation, investors are likely to examine the Q1 outcome closely before making their buying decisions.

The company is all set to publish the results on February 15, at 4:00 p.m. ET. The consensus earnings estimate is $1.91 per share, which represents a decline from the $2.03/share reported in the first quarter of 2023. Market watchers are looking for revenues of $6.48 billion for the January quarter, compared to $6.74 billion in the year-ago period. In the trailing six quarters, earnings and revenues beat estimates consistently and the trend is likely to continue.

Road Ahead

Applied Materials’ long-term prospects look promising, thanks to the demand rebound in China and growing opportunities in the areas of AI and cloud infrastructure. At the same time, the US government’s recent initiatives to accelerate innovation in microprocessor research, with a focus on AI chips, bodes well for companies like Applied Materials. It is estimated that the rapid adoption of AI, which has created a sharp demand-supply imbalance, will make semiconductors a $1 trillion industry by 2030.

From Applied Materials’ Q4 2023 earnings call:

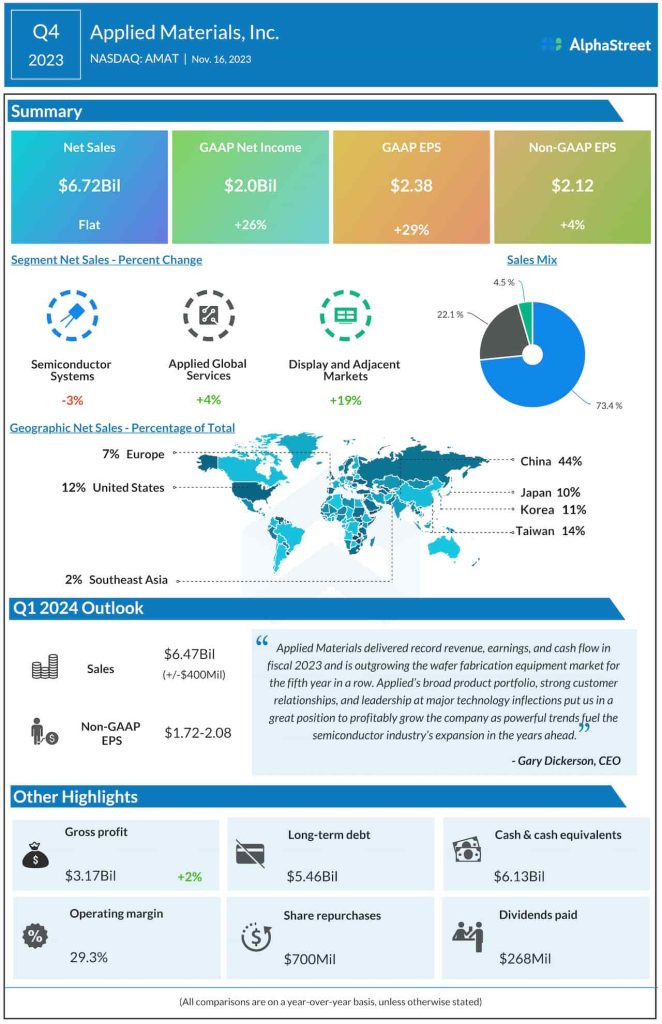

“While semiconductor and wafer fabrication equipment spending were both down in 2023, Applied was able to demonstrate the strength of our broad portfolio, as well as the central role we play in enabling major industry inflections. Our semiconductor systems business delivered mid-single-digit growth for the fiscal year and remains on track for growth in calendar 2023, which will be the fifth consecutive year that we’ve outperformed the wafer fab equipment market.”

Mixed Q4

In the final three months of fiscal 2023, the company’s adjusted earnings rose to $2.12 per share from $2.03 per share in the same period of 2022. Net income, including special items, was $2.0 billion or $2.38 per share in the October quarter, compared to $1.59 billion or $1.85 per share last year.

At $6.72 billion, Q4 sales were broadly unchanged from the prior-year period. The company generated $1.56 billion in cash from operations and distributed $968 million to shareholders during the three months.

Over the past three months, AMAT has constantly traded above the 52-week average. The stock traded lower during Tuesday’s regular session, after retreating from last week’s peak.