Blue Apron Holdings (NYSE: APRN) is scheduled to report its second quarter 2019 earnings results on Tuesday, August 6, before market open. Analysts expect the company to report a loss of $1.08 per share on revenue of $138 million.

There appears to be very little optimism surrounding Blue Apron in general. The company’s business model is both expensive and inefficient and it does not offer much incentive in terms of attracting new customers or retaining existing ones.

Blue Apron also faces tough competition from other delivery services as well as retailers like Walmart (NYSE: WMT) and Kroger (NYSE: KR) who offer lower-priced meal kits in their stores. This significantly hurts the company’s business.

In June, Blue Apron announced a 1-for-15 reverse stock split which helped it avoid delisting from the NYSE. Last month, the company announced it would start offering plant-based products from Beyond Meat (NASDAQ: BYND) on its menus from August.

Wall Street remains unimpressed with these two moves. Analysts

do not see much benefit coming out of these actions and even though Blue Apron’s

shares had spiked 20% on the Beyond Meat-alliance news, it was considered

nothing more than a halo effect.

Analysts do not believe the partnership with Beyond Meat can

save Blue Apron and the sentiment surrounding Blue Apron’s future prospects is bleak.

Blue Apron would require a change in strategy fast in order to survive in this

difficult environment.

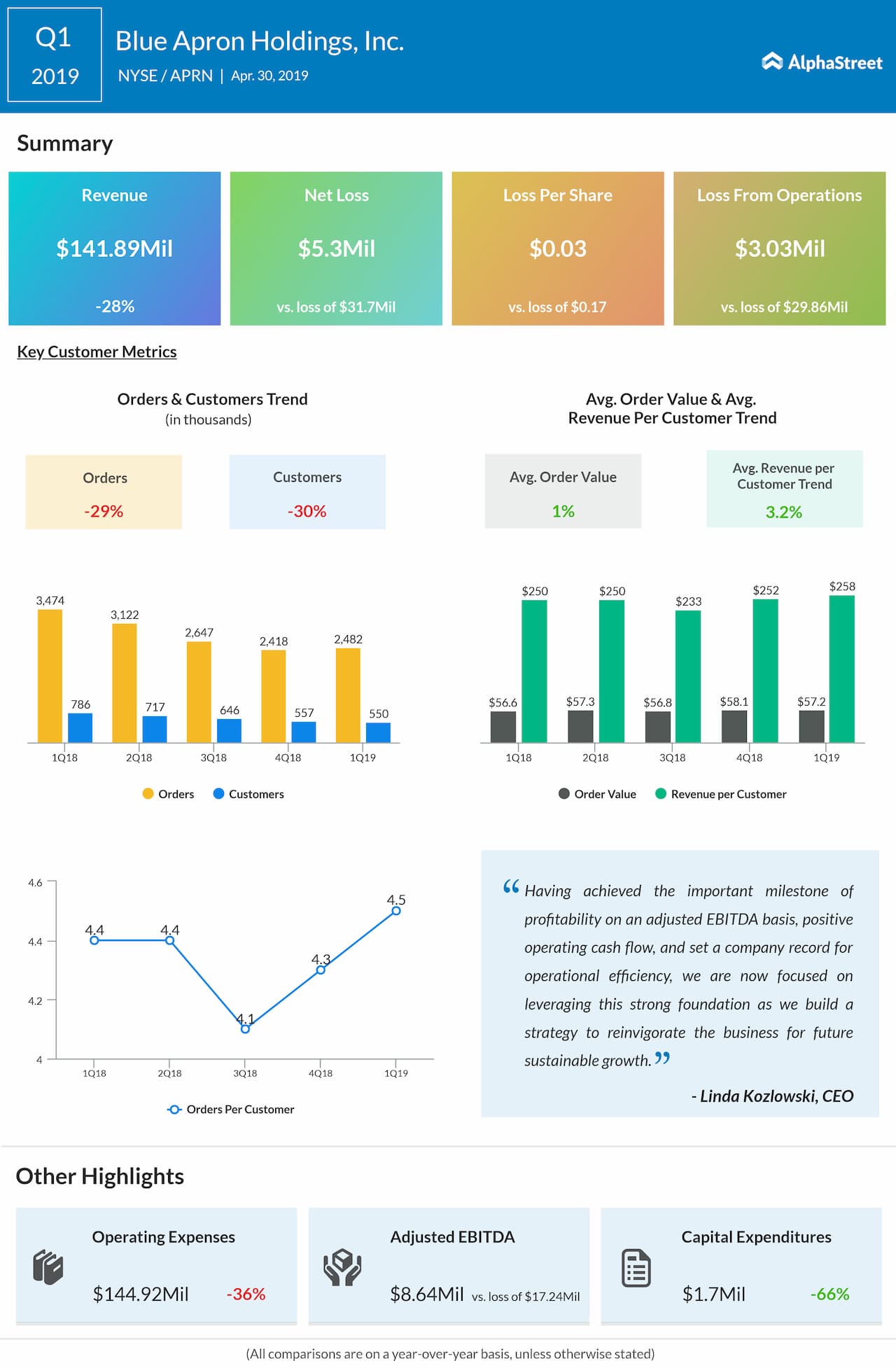

In the first quarter of 2019, Blue Apron missed top line estimates while the bottom line was narrower-than-expected. Revenue fell 28% year-over-year to $141.9 million while net loss narrowed to $0.03 per share from $0.17 per share last year. Orders fell 29% while the number of customers dropped 30% from a year ago.

Blue Apron’s shares have dropped 52% year-to-date and 48% over the past three months. The stock has an average 12-month price target of $6.00.