Oracle Corporation (NYSE: ORCL) has successfully transitioned into a cloud-centric business from a software maker, but recent data show that the company is lagging behind its peers in the cloud space. When the tech firm reports earnings next week, investors’ focus will be on its top line which experienced a slowdown in recent quarters.

The Stock

Oracle’s stock has gained 6% so far this year and is currently trading around $110, which is 12% below the September peak. The value has more than doubled in the past five years. However, the valuation is still reasonable, which makes ORCL a good long-term investment though the price will likely remain flat in the foreseeable future. The company has a good track record of returning cash to shareholders generously, through dividends and stock repurchases.

Oracle is expected to deliver positive results for the February quarter. Experts predict earnings of $1.38 per share for Q3, compared to $1.22 per share in the same period of 2023. It is estimated that third-quarter revenues increased 7% annually to $13.31 billion. The management targets capital spending of around $8 billion for fiscal 2024, with a large portion of that expected in the second half as it works to bring online more capacity. The report will be released on March 11, after the closing bell.

In Growth Mode

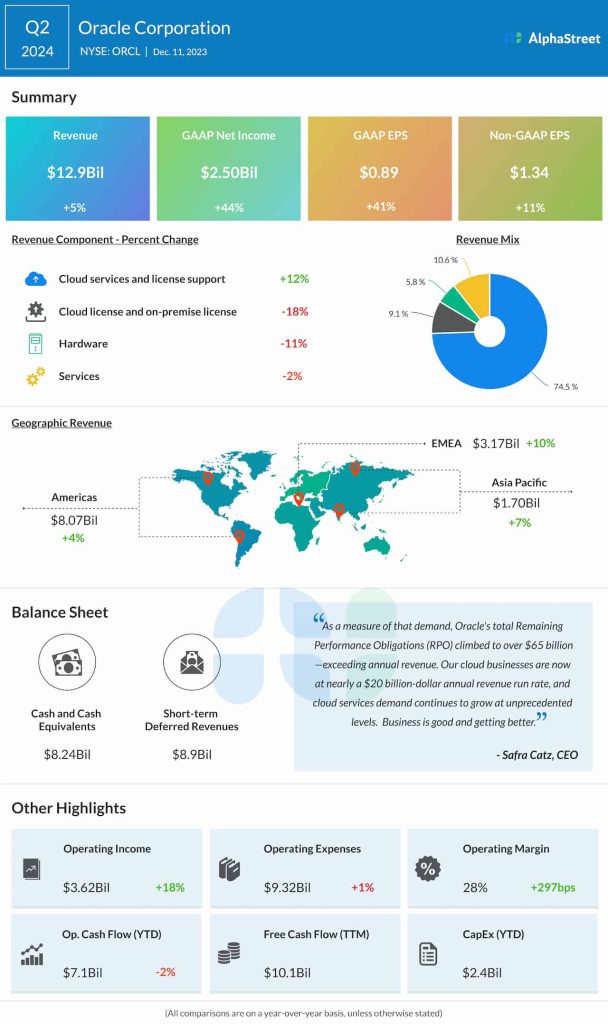

Oracle ended the last quarter with an impressive free cash flow of about $10 billion, which is good considering its ongoing growth initiatives focused on cloud infrastructure. The cloud push has boosted the company’s enterprise software-as-a-service capabilities and better positioned it to compete with others, including Microsoft and Google. Recently, it announced the availability of the Oracle Cloud Infrastructure Generative AI service that makes it easier for companies to leverage the latest advancements in generative AI.

However, economic uncertainties and cautious enterprise spending on technology will likely remain a drag on revenues. Since Oracle continues to rely on legacy systems and licenses, it is crucial to balance the shift to modern cloud offerings while maintaining existing revenue streams.

“The demand for cloud infrastructure services and new Oracle Cloud data centers is broad-based, driven not only by generative AI customers but also by nation-states buying sovereign Oracle Cloud data centers, plus large banks, telecommunications companies, and industrial companies buying dedicated cloud data centers — dedicated Oracle Cloud data centers. And perhaps most interestingly, demand from other hyper-scalers and other cloud service providers co-locating and connecting their clouds with Oracle Cloud data centers,” said Oracle’s CTO Larry Ellison at the Q2 earnings call.

Mixed Outcome

In the second quarter, earnings beat the Street View for the fifth time in a row, while revenues missed. A double-digit revenue growth in the core cloud services division more than offset declines in the other segments, resulting in a 5% growth in total Q2 revenues to about $13 billion. Meanwhile, the top line grew across all geographical regions. There was an 11% increase in adjusted earnings to $1.34 per share during the three months.

On Tuesday, Oracle’s shares opened sharply lower and traded down 2.55% in the afternoon. They have gone through a series of ups and downs in the past six months.