Shares of Conagra Brands, Inc. (NYSE: CAG) rose 1% on Friday. The stock has dropped 7% in the past three months. The branded food company is slated to report its earnings results for the second quarter of 2026 on Friday, December 19, before the market opens. Here’s a look at what to expect from the earnings report:

Revenue

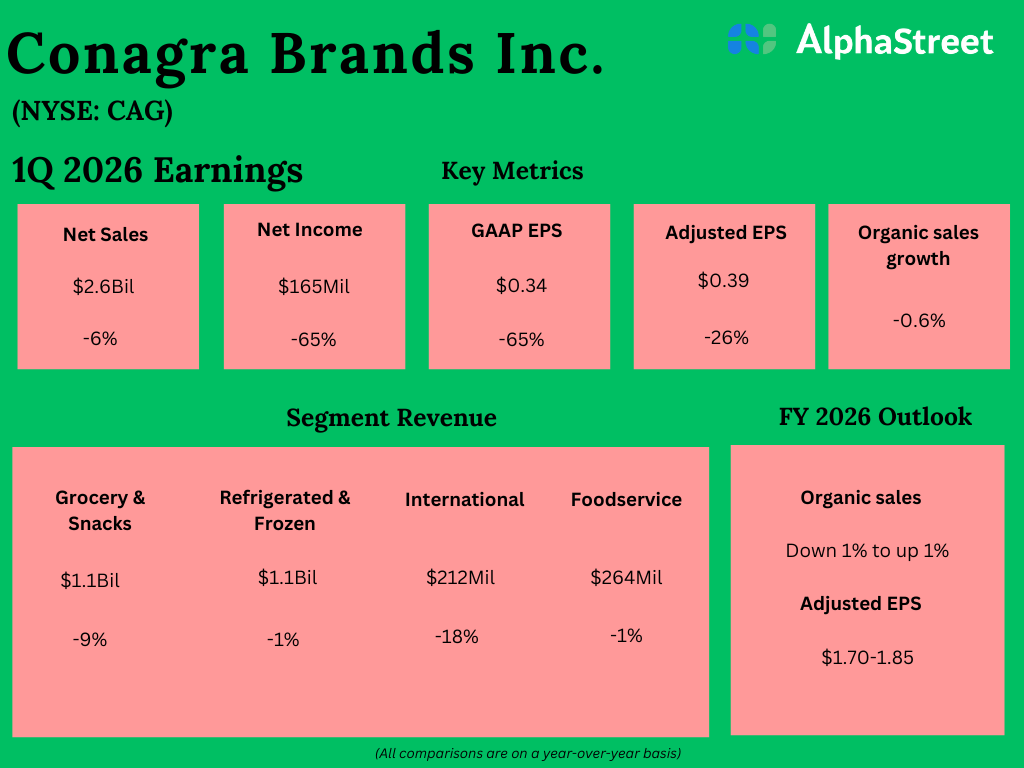

Analysts are projecting revenue of $2.99 billion for Conagra in the second quarter of 2026, which indicates a decline of 6% from the corresponding period a year ago. In the first quarter of 2026, net sales decreased 5.8% year-over-year to $2.63 billion.

Earnings

The consensus estimate for earnings per share in Q2 2026 is $0.44, which implies a decrease of 37% from the prior-year quarter. In Q1 2026, adjusted EPS fell 26.4% YoY to $0.39.

Points to note

Conagra continues to face a challenging operating environment with inflationary pressures, tariffs and muted consumer sentiment. The company expects bigger impacts from inflation and tariffs than previously anticipated, while consumers continue to seek value against an inflationary backdrop.

On its last earnings call, CAG forecast organic sales to decline low-single-digits in the second quarter, driven by consumption trends and a shift in trade expense. In Q1, organic sales dipped 0.6%, driven by a 0.6% positive impact from price/mix and a 1.2% drop in volume.

Last quarter Conagra saw declines in sales and volume across its segments. The company continues to invest in its brands to drive volume recovery in a difficult consumer environment. In Q1, it saw gains in categories such as frozen vegetables and meals, as well as strategic protein snacks, like meat snacks and seeds, but salty snacks and sweet treats witnessed declines.

Higher costs for animal proteins such as beef, pork, and turkey are expected to remain a headwind. As inflation persists, value-seeking behavior from consumers can be expected to pressure category growth. CAG managed to resolve most of the supply chain issues it faced in the past quarters and it continues to invest in supply chain resiliency. The company has been implementing targeted pricing and taking measures to improve its productivity and these may be reflected in the Q2 performance.