Domino’s Pizza, Inc. (NYSE: DPZ) entered the new fiscal year on a high note, reporting stronger-than-expected earnings for the first quarter. The fast-food giant is preparing to release its Q2 report on July 18, before the opening bell. Being the world’s largest pizza chain, the company has thrived on the growing demand for the traditional Italian dish over the years.

After rising to a two-and-half-year high last month, Domino’s stock pulled back and maintained a downtrend since then. However, it is up 15% since the beginning of the year. Long-term investors wouldn’t want to miss the opportunity brought about by the recent drop in share price. Considering the company’s strong fundamentals and growing store chain, there is great potential for share price growth.

It is estimated that the Michigan-headquartered firm’s earnings increased to $3.63 per share in the June quarter from $3.08 per share a year earlier. The company is expected to report $1.1 billion in revenues when it announces Q2 results on Thursday, July 18, at 6:05 am ET. In the year-ago quarter, it generated revenues of $1.07 billion.

Stable Growth

While maintaining its dominance in the market, the restaurant chain keeps expanding globally, indicating continued long-term revenue growth. Since the lion’s share of Domino’s sales comes through its partners, the steady uptick in franchise profits bodes well for the company – last year, there was a double-digit increase in profits earned by franchises. The Hungry for MORE strategy has been successful, and it is expected to drive revenue growth in the long term. The top line also benefits from the extended loyalty program and delivery partnership with Uber Eats.

Domino’s CEO Russell Weiner said during his post-earnings interaction with analysts, “Domino’s Rewards continues to perform extremely well and was the key driver of our strong U.S. comp performance. The program is delivering on our objectives. Active member growth rates are up significantly since the launch of our new program. From a percentage standpoint, our biggest increases are coming from new, lapsed, and light customers. So, we’re bringing these new customers into the fold. I’m particularly pleased with the increase in carryout customers made possible in part by our reduced $5 minimum spend for earning point.”

Q1 Results

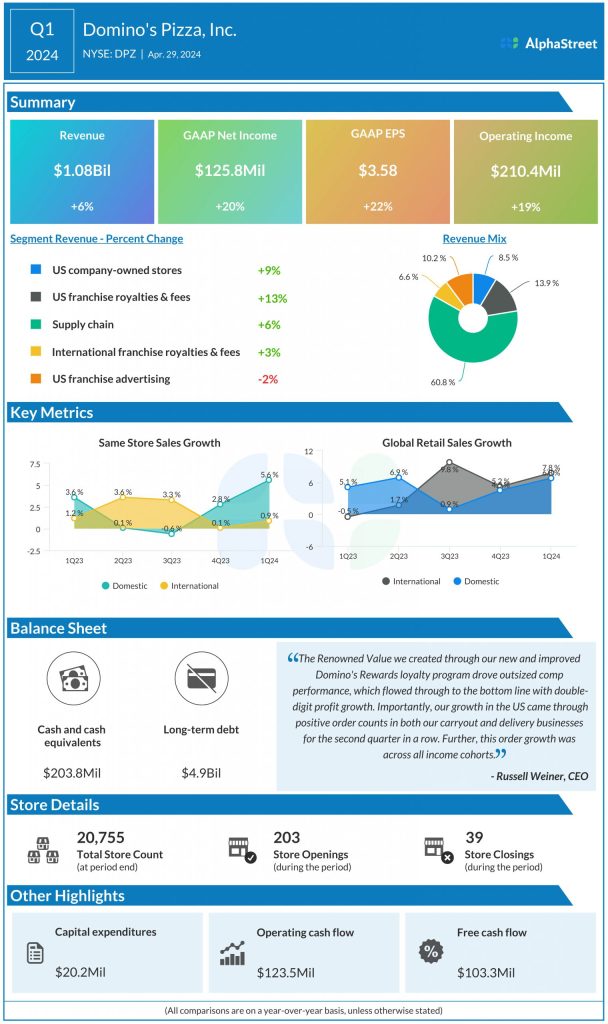

The company delivered stronger-than-expected earnings consistently in the past six quarters, while the top line mostly fell short of expectations. In the March quarter, revenues advanced 6% annually to $1.08 billion, reflecting higher sales at the main operating divisions.

The top line particularly benefited from higher supply chain revenues and US franchise royalties/fees, as well as strong performance by US Company-owned stores. Both retail sales and comparable store sales growth accelerated during the period. Consequently, Q1 profit climbed to $125.8 million or $3.58 per share from $104.8 million or $2.93 per share a year earlier.

Extending the recent weakness, Domino’s stock dropped further this week and slipped below $500. The shares traded down 1% on Wednesday afternoon.