Home Depot (NYSE: HD) is preparing to report earnings next week amid speculation that the downturn in the housing market would negatively impact the results. Meanwhile, it is estimated that the demand for new homes will bounce back once the central bank lowers interest rates this year as widely expected. But, the recovery might be restricted by inflation and economic uncertainties.

Home Depot’s stock peaked in mid-March but has lost around 10% since then. While the valuation looks high despite the recent dip, HD remains a good long-term investment, thanks to the company’s strong fundamentals, brand power, and market dominance. The current price is broadly in line with the stock’s value six months ago. It has been a favorite among income investors due to regular dividend raises. After the latest hike, the dividend yield is 2.8%, well above the average S&P 500 yield.

Outlook

The second-quarter report is slated for publication on Tuesday, August 13, at 6:00 am ET. On average, analysts who follow the company project earnings of $4.53 per share for the June quarter, which represents a decrease from the $4.65/share the company earned in Q2 2023. Meanwhile, revenues are seen increasing to $43.24 billion in the second quarter from $42.9 billion in the prior-year period.

From Home Depot’s Q1 2024 earnings call:

“We know that delivering the best shopping experience for any purchase occasion is critical to our success. That is why we continue to invest in our Pro sales teams and capabilities. We have developed new capabilities within our Pro intelligence tool which feeds our CRM platform and leverages data science to bring better insight to our sales teams. These tools are helping us to both assist in identifying the optimal Pro target in a market as well as the highest value cross-selling opportunities to drive action and sales.“

The company’s cash flows have been quite healthy, giving it the leeway to repurchase shares at regular intervals. At the same time, Home Depot’s scale and operational efficiency have steadily increased its profit margin over the years. While the business continues to suffer from the slowdown in home sales, a potential interest rate cut – as signaled by policymakers – could provide a much-needed boost.

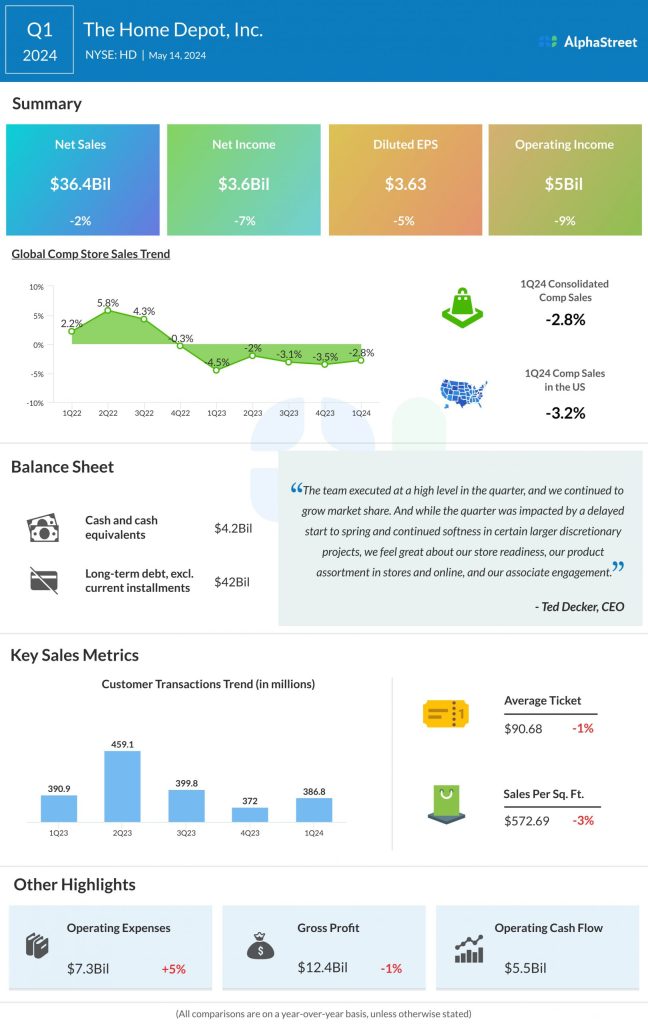

Sales Dip

In the first three months of fiscal 2024, Home Depot’s sales decreased 2.3% year-over-year to $36.4 billion. Comparable sales dropped 2.8%, marking the sixth decline in a row. As a result, first-quarter net income dropped to $3.6 billion or $3.63 per share from $3.9 billion or $3.82 per share in the corresponding quarter a year earlier. Earnings topped expectations – the fourth consecutive beat — while revenue missed the view after beating in the trailing three quarters.

The management attributed the weak Q1 performance to the delayed start to spring and continued softness in certain discretionary projects. For fiscal 2024, the leadership expects sales and earnings/share growth of around 1%, including the 53rd week. Full-year comparable sales are expected to decline by 1% annually.

After last week’s lackluster performance, Home Depot’s stock regained some strength ahead of the earnings and traded higher mostly during Tuesday’s session.