Over the years, Johnson & Johnson (NYSE: JNJ) has remained a dominant player in the medical industry, benefitting from its unique business model and growth strategy focused on constant innovation. The diversified portfolio has helped the healthcare conglomerate to be resilient to various headwinds, including regulatory issues and the multiple lawsuits it faces over product safety. The company will be reporting its third-quarter results next week.

The last closing price of Johnson & Johnson’s stock is broadly unchanged from its value about three-and-half years ago, as the shares maintained a sideways trend during that period. Recovering from the downturn experienced in the first half, the stock has grown about 9% in the past three months. Earlier this year, the management raised the quarterly dividend by 4.2%, continuing a tradition of annual dividend hikes that date back over six decades. With an above-average yield of 3%, JNJ remains an attractive buying option for income investors.

Q3 Report Due

The pharma giant’s third-quarter report is slated for release on Tuesday, October 15, at 6:20 am ET. The market is expecting a mixed outcome – adjusted profit is seen declining year-over-year to $2.20 per share from $2.66 per share in Q3 2023. On the other hand, revenue is estimated to have increased 5.2% from last year to $22.13 billion in the September quarter. The company has a long history of delivering stronger-than-expected quarterly earnings consistently.

In the most recent quarter, sales grew across all key geographical segments except Asia and Africa. The company stands out among others in the industry due to its equally strong presence in the consumer health, medical devices, and pharmaceutical markets. Johnson & Johnson has a strong balance sheet, and it is one of the only two companies with AAA bond ratings globally.

Tailwinds

Johnson & Johnson stands to benefit from its healthy cash position when settling the series of litigations over unsafe talcum powder and asbestos contamination, which are likely to cost the company billions of dollars. A few months ago, the firm announced a reorganization of its subsidiary, LLT Management, to resolve all current and future claims related to cosmetic talc litigation in the US. Meanwhile, the company recently challenged in court the Inflation Reduction Act, a new law for lowering prescription drug prices, and confirmed its growth projections for FY25.

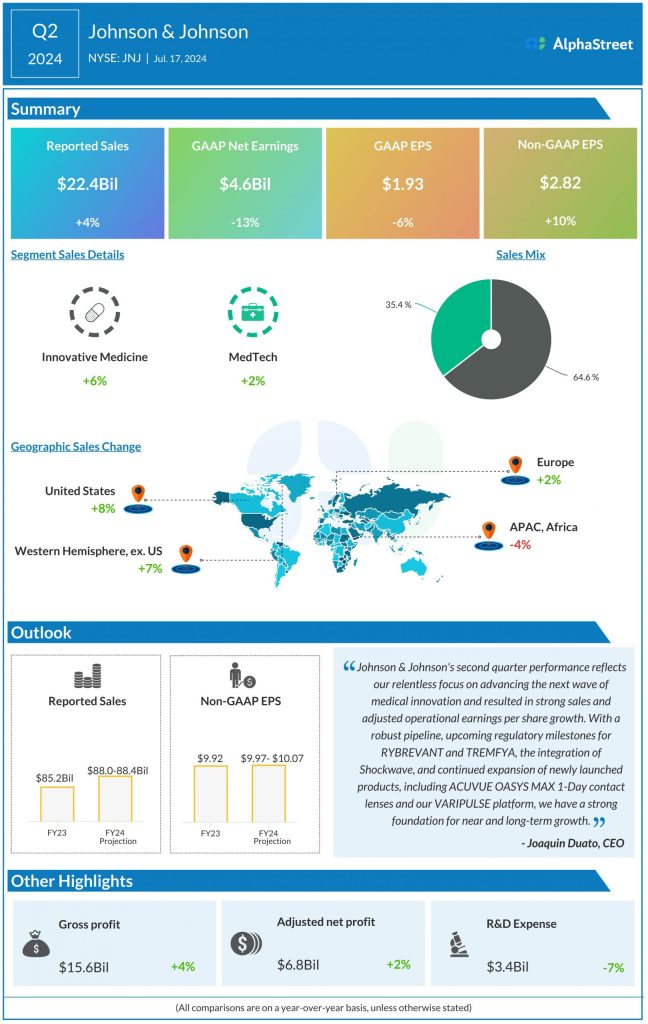

On the positive full-year guidance, Johnson & Johnson’s CEO Joaquin Duato said at the Q2 earnings call, “Our confidence in the business outlook remains unchanged with meaningful outcomes from the DanGer Shock trial in Abiomed and the second quarter close of the Shockwave acquisition, we look forward to continued expansion into high-growth MedTech markets. As you know, Johnson & Johnson is laser-focused on advancing the next wave of medical innovation, we’re building on a strong foundation to unlock accelerated growth with a healthy balance sheet and industry-leading investments in the best science and innovation.”

Mixed Results

In the second quarter, it was a mixed show for the company in terms of its financial performance compared to analysts’ estimates, with earnings beating and sales missing estimates. The Innovative Medicine segment, which represents nearly 65% of the total business, expanded 6% year-over-year in the June quarter, while MedTech revenue rose modestly by 2%. At $22.4 billion, total sales were up 4% year-over-year, and that translated into a 10% increase in adjusted earnings per share to $2.82.

After staying almost flat throughout last week, shares of Johnson & Johnson traded slightly higher in the early hours of Tuesday’s session.