For Micron Technology, Inc. (NASDAQ: MU), 2023 was a challenging year when sales were hit by unfavorable demand-supply dynamics and a ban in China. When the company reports second-quarter results next week, the market will be closely following the event as it is expected to provide crucial insights into the semiconductor firm’s financial health. Recently, Micron’s management issued positive guidance for the quarter, after reporting better-than-expected first-quarter results.

Stock Peaks

The chipmaker’s stock has gained around 15% since the beginning of the year and hit an all-time high last week. The value has more than doubled in the past four years. MU is a growth stock with the potential to deliver handsome shareholder returns. Considering its aggressive AI push and the fast-paced infusion of artificial intelligence in mobile devices, Micron looks like a good long-term investment. The AI adoption spree should trigger a rebound in the demand for Micron’s products, further driving up the stock price. There has been a sales slowdown ever since markets reopened, reversing the demand surge that boosted revenues during the pandemic-induced shutdown a couple of years ago.

Micron’s second-quarter report is slated for release on Wednesday, March 20, at 4.05 p.m. ET. Experts’ consensus estimates indicate that the company incurred an adjusted loss of $0.25 per share for the February quarter, which is sharply narrower than the $1.91/share loss it reported for the prior year period. Meanwhile, Micron executives are looking for a loss of approximately $0.28 per share. The bottom-line forecast reflects an estimated 32% increase in Q2 revenues to $4.87 billion, which is below the company’s guidance of $5.30 billion.

Demand Picks up

Since Micron’s high-bandwidth memory chips are ideal for use in AI-enabled systems, they are in high demand, thanks to the widespread integration of the technology in data centers and mobile devices. While the business is cyclical, the current demand-supply gap should enable the company to generate profitable growth going forward.

From Micron’s Q1 2024 earnings call:

“The improved supply-demand environment in the current calendar quarter gives us additional confidence in the trajectory of our business. We have driven a strong inflection in industry pricing this calendar quarter, which will allow us to benefit from higher prices earlier in our fiscal year compared to prior plans. We intend to stay very disciplined with our supply and capacity investments as our pricing is still far from the levels associated with the necessary return on investment (ROI). We expect our pricing to continue to strengthen through the course of calendar 2024.”

Net Loss in Q1

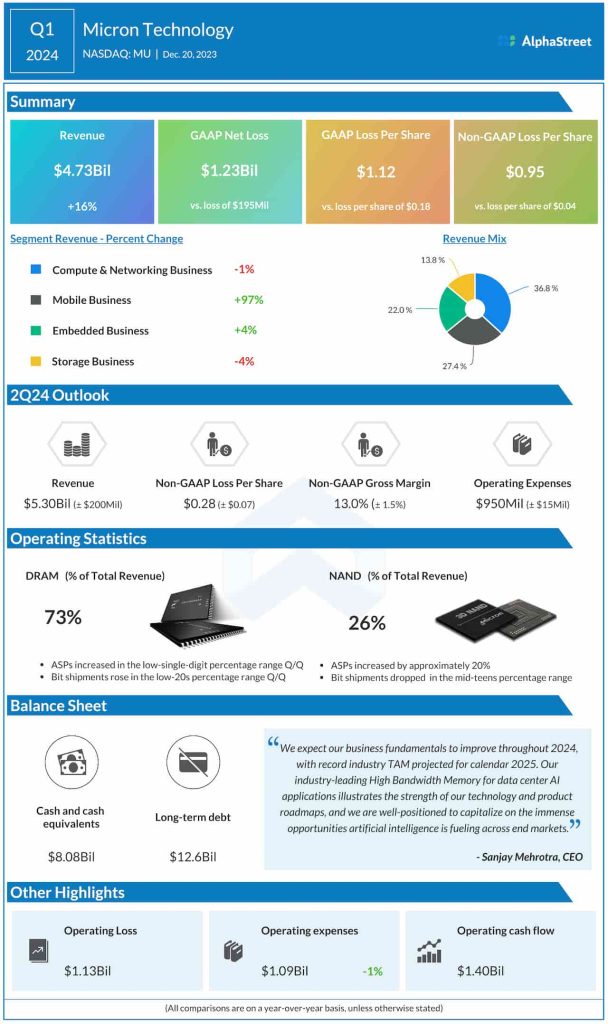

The company has been reporting quarterly losses regularly for over a year. In the most recent quarter, the results came in above analysts’ estimates, after two consecutive misses. Adjusted loss widened to $0.95 per share in the first quarter from $0.04 per share in the year-ago quarter. Meanwhile, revenues increased 16% year-over-year to $4.73 billion, mainly reflecting strong performance by the Mobile Business division.

Shares of Micron made strong gains on Tuesday, after opening the session higher. The stock traded around $95 in the afternoon, which is well above the long-term average.