Over the years, brand loyalty and diversification of the portfolio have played a key role in the continued success of PepsiCo, Inc. (NASDAQ: PEP) The soft drink giant is now focused on productivity initiatives to support spending on innovation and brand building, as it seeks to become a faster, stronger and better organization.

The company regularly pays dividends and currently offers a dividend of 2.8%, which is well above the S&P 500 average. The stock has been pretty resilient to the many headwinds markets faced in recent years. Though the shares rebound quickly after every drop, they often underperformed the market this year. After making steady gains over the years, PEP hit a peak in May 2023 but changed course since then and traded at a near-one-year low last week. Right now, the stock is reasonably priced.

Market Leader

PepsiCo’s constantly expanding portfolio and growing market share allow it tackle to the general demand slowdown in the beverages market. The company and its arch-rival Coca-Cola are far ahead of their competitors but data show that PepsiCo generates significantly higher quarterly revenues, helped by its larger portfolio. However, the company’s pricing power is relatively weak in the non-beverage segments, which often results in lower gross margins. To some extent, the bottom line is benefitting from the management’s cost-cutting program, which included several layoffs. That is important because the company has had a tough time dealing with the sharp increase in operating expenses over the last year, mainly due to higher costs related to labor, transportation, and raw materials.

Commenting on consumers’ shopping patterns, at the second-quarter earnings call, PepsiCo’s CEO Ramon Laguarta said, “We’re seeing consumers shopping in more stores than before. They’re looking for better deals. They’re starting to look for optimization. They are going into channels that have better-perceived value. They’re buying more in dollar stores or they’re buying more in mass or in clubs. So, every segment of the consumer is making adjustments. Overall, we’re seeing very positive, and I think it has to do with the levels of unemployment that we’re seeing all around the world.”

What’s in Cards

When it announces third-quarter results on October 10, in the morning, PepsiCo is expected to report earnings of $2.15 per share, which is up 9% from the prior-year quarter. In the third quarter of 2022, the adjusted profit was $1.97 per share. It is estimated that August-quarter revenues rose about 7% annually to $23.43 billion.

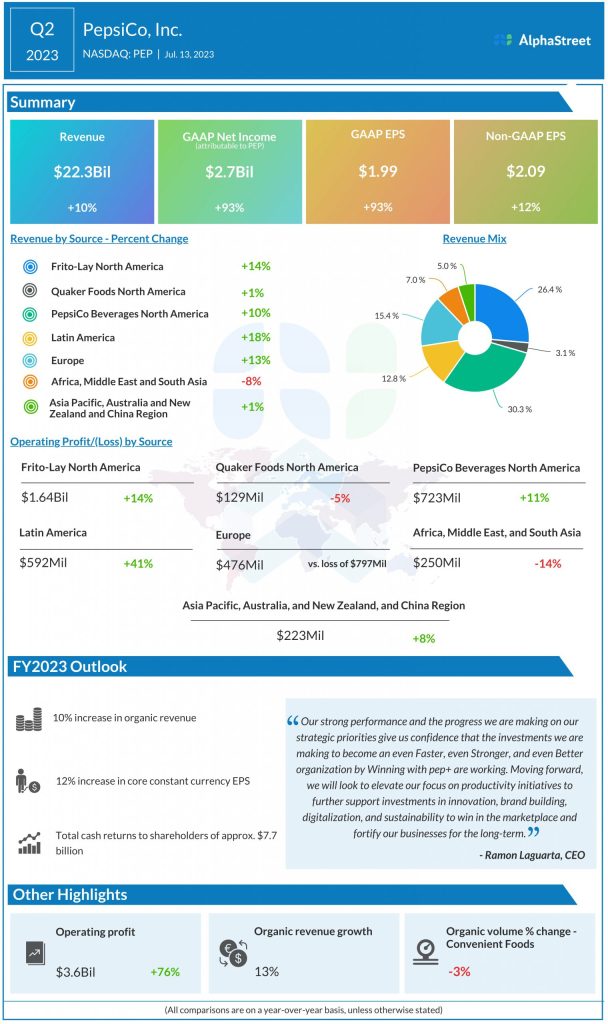

In the last quarter, sales grew across all business segments and almost all geographical regions. At $22.3 billion, total revenue was up 10% from last year. The positive top-line growth translated into a 12% increase in adjusted earnings to $2.09 per share. There was a 13% increase in organic revenue. The results also topped expectations. Interestingly, the company maintained stable performance even during the pandemic, and its quarterly earnings beat estimates constantly for more than a decade.

Encouraged by the solid Q2 outcome, the management raised its full-year guidance and currently forecasts a 10% rise in organic revenue and 12% earnings growth on a constant-currency basis.

The stock experienced weakness throughout September and ended the month on a low note. It traded around $170 on Monday afternoon.