While the business world struggles to come out from the grip of inflation, some sectors have managed to stay resilient and the beverage industry is one of them. PepsiCo, Inc. (NASDAQ: PEP), a dominant player in the soft drink market, has a history of tackling challenges with the power of its brands and diversified portfolio. Currently focused on investing in the business and boosting productivity, the company is all set to report its June quarter results next week.

After retreating from its peak about a year ago, PepsiCo’s stock is yet to fully recover though it saw a significant upswing a few weeks ago. Its performance in 2024 has been lackluster so far, and the share price has remained relatively unchanged since the beginning of the year. The company raised its dividend regularly for over half a century and currently has a yield of above 3%. This dividend king is an attractive investment option for income investors.

Estimates

The New York-headquartered beverage giant is expected to publish its second-quarter 2024 earnings report on July 11, at 6:00 am ET. On average, analysts covering the company estimate that adjusted earnings increased to $2.16 per share in Q2 from $2.09 per share a year earlier. They see a 1.4% growth in revenues to $22.63 billion.

There has been a great deal of caution among customers when it comes to spending on discretionary items due to inflation, but people are still willing to spend on relatively less expensive items like snacks and soft drinks. PepsiCo’s brands are well-received across markets as the company follows the strategy of adding local flavors to products and integrating elements of a particular region’s culture into its offerings.

LATAM Gains

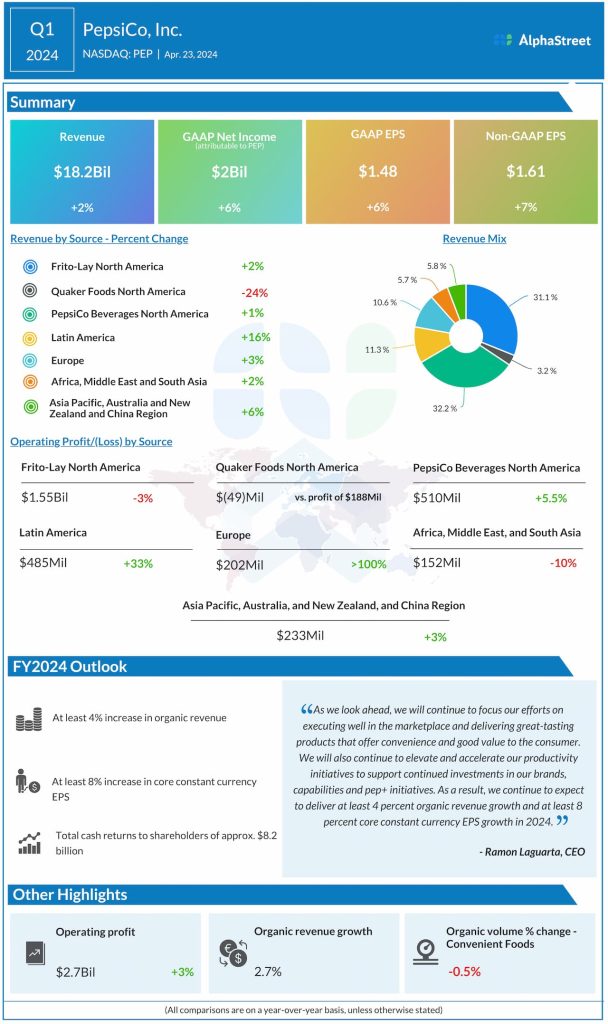

In recent quarters, continued sales growth in Latin America has helped the company overcome weaknesses in core business segments — Frito-Lay North America and PepsiCo Beverages North America. Interestingly, operating profit for the Latin America business grew an impressive 33% in the most recent quarter. For fiscal 2024, the management predicts total organic revenue growth of about 4% and core EPS of at least $8.15.

From PepsiCo’s Q1 2024 earnings call:

“We’ve been investing in capacity. We’re – right now we’re in the process of opening factories in Vietnam and in China and in India, and in Mexico and in – we just opened one in Poland. So, we keep expanding our manufacturing and our go-to-market capabilities in those markets. So, we feel good and I think that it’s going to continue to be a big source of growth for us. As we mentioned in CAGNY, I think our International business is already $36 billion and is growing at a very high single-digit level and with very good profitability.”

Results Beat View

In what is a rare distinction, the company delivered quarterly earnings that either beat or matched expectations consistently for over a decade, including in the first quarter that ended in March 2024. Core net income, adjusted for special items, increased 7% annually to $1.61 per share in Q1. Revenue advanced 2.3% to $18.2 billion, with a 2.7% growth in organic revenue. The top line exceeded Wall Street’s forecast, continuing the recent trend. Net income attributable to the company was $2.04 billion or $1.48 per share in the first quarter, compared to $1.93 billion or $1.40 per share a year earlier.

A few weeks ago, shares of PepsiCo slipped below their long-term average, after pulling back from a 10-month high. They have lost more than 10% in the past twelve months.