Salesforce, Inc. (NYSE: CRM) achieved accelerated sales growth and profitability in recent quarters, in line with its transformation goal. The customer relationship management platform bets on new opportunities in generative AI to meet its growth target, while leveraging increased enterprise spending on digital transformation.

CRM is one of the top-performing stocks, currently trading sharply above its 12-month average. It has gained an impressive 70% since slipping to a multi-year low a year ago. Adding to the positive investor sentiment, the management raised its full-year financial guidance a few months ago. The stock is reasonably priced compared to some of the big tech firms and has the potential to create good shareholder value.

AI Push

Having integrated its popular cloud-based tools like Einstein, Data Cloud, MuleSoft, and Slack into a single platform, Salesforce is well-prepared to take advantage of the widespread AI adoption. The company has been busy ramping up its AI capabilities lately. Meanwhile, after strengthening its portfolio through a series of acquisitions, including ExactTarget, e-commerce firm Demandware, and Tableau, the company has paused M&A activities for now and is focused on enhancing productivity and profitability.

Going by the recent uptrend, Salesforce’s quarterly revenues are expected to grow in double digits in the near term. Better-than-expected growth in current remaining performance obligations – 11% in Q2 – indicates that forward revenue growth would remain in double digits in the near future. A disciplined approach to cost management allowed the company to exceed its 30% adjusted margin target in the most recent quarter.

Q3 Report

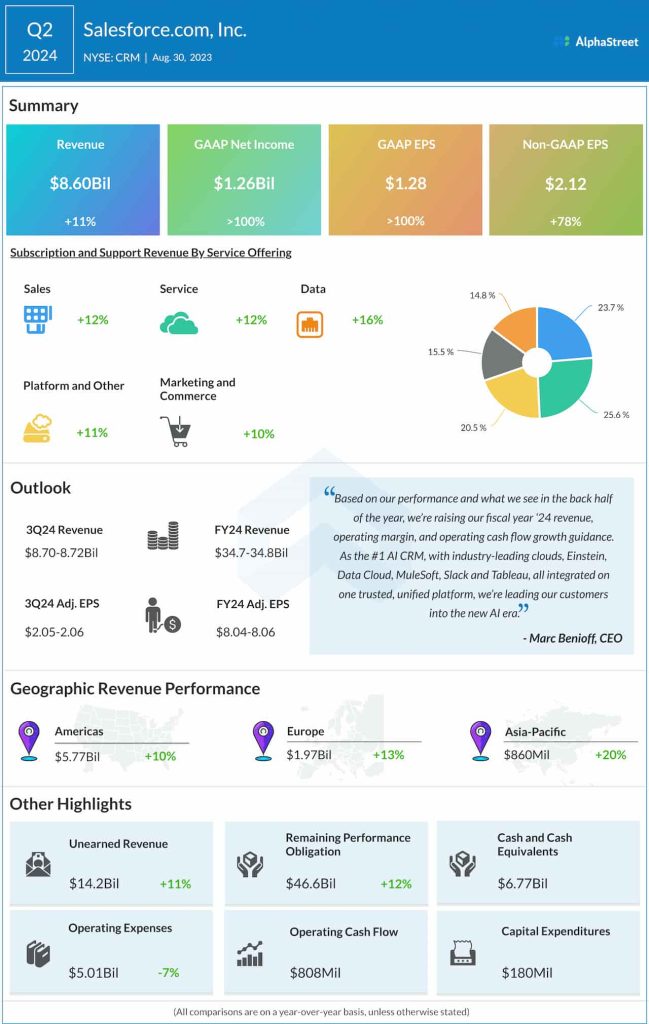

The tech firm’s third-quarter report is expected to come on November 29, after regular trading hours. The consensus earnings forecast is $2.06 per share, vs. $1.40 per share in the third quarter of 2023. It is estimated that Q3 revenues rose to $8.72 billion from last year. Salesforce executives are looking for October-quarter revenues in the range of $8.70 billion to $8.72 billion, and adjusted earnings per share between $2.05 and $2.06.

From Salesforce’s Q2 2024 earnings call:

“…we’ve maintained our disciplined approach to cost management while also investing in growth initiatives across our entire platform and offerings. And, we’re positioning Salesforce for the future and will continue to drive our margins, and also while we’re continuing to drive customer growth. Revenue in the second quarter was 8.6 billion, that’s up 11% year over year and the same in constant currency.”

Key Metrics

Over the years, the company has impressed its stakeholders by delivering bigger-than-expected quarterly profits consistently. It has a balanced portfolio, with every segment contributing meaningfully to the top line. In the second quarter, all divisions — Sales, Service, Data, Platform, and Marketing — grew in double digits. As a result, total revenue jumped 11% year-over-year to $8.60 billion. Adjusted earnings surged 78% to $2.12 per share, and unadjusted profit more than doubled to $1.28 per share.

CRM has gained 14% in the past 30 days alone, outperforming the broad market. The stock closed Friday’s session slightly higher, continuing the recent trend.