After delivering a solid performance last year, UnitedHealth Group (NYSE: UNH) will be reporting first-quarter financial data next week. The healthcare conglomerate’s business growth accelerated in recent years, driven mainly by M&A deals including some important acquisitions by its subsidiary Optum.

United’s stock climbed to an all-time high in November last year, but pulled back later and lost about 20% since then. It seems the shares are headed for a strong bounce back this year, with experts predicting up to one-third growth in the next twelve months. The company has raised its dividend regularly for many years, and the current yield is above the S&P 500 average. The good thing about the recent dip is that the stock has become a lot more affordable, and it offers a good buying opportunity that long-term investors wouldn’t want to miss.

Financials

Meanwhile, investor sentiment took a beating after the company reported a spike in medical costs a few months ago, despite delivering impressive quarterly numbers. The high costs be attributed mainly to an increase in elective procedures. Patients who postponed major surgeries during the pandemic are finally getting treated, resulting in larger insurance claims.

UnitedHealth, which is the largest health insurance provider in the US, has an impressive track record of consistently meeting or exceeding analysts’ quarterly earnings estimates for over a decade. There is a high chance of the trend continuing in the first quarter, the report for which is scheduled for release on Tuesday, April 16, at 5:55 am ET. On average, analysts following the company call for earnings of $6.64 per share for Q1 2024, on an adjusted basis, vs. $5.72/share a year earlier. Revenue is expected to grow 10.7% from last year to $99.38 billion.

Liquidity

The insurer has a strong balance sheet and healthy cash flow – it repurchased $8 billion of common shares last year. The company looks well-positioned to further expand the business and pursue more acquisitions. There has been a steady increase in medical spending due to the growing demand for care among the country’s aging population, which contributes to the top-line growth of healthcare firms like UnitedHealth.

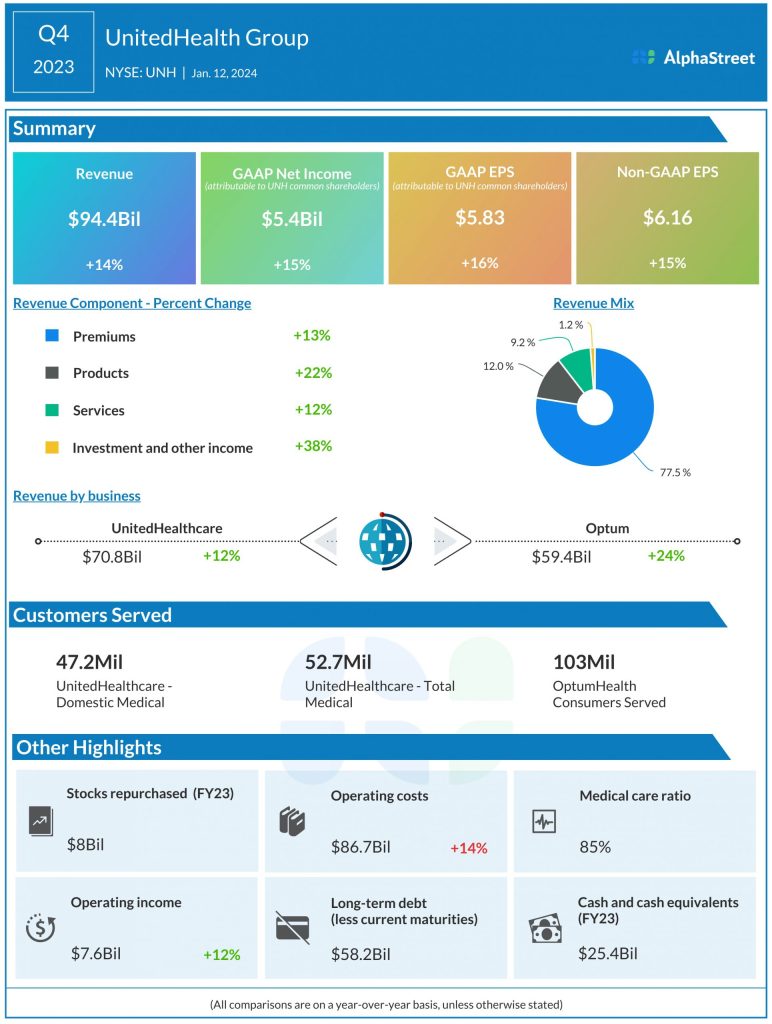

From UnitedHealth’s Q4 2023 earnings call:

“Our goal is to become the trusted source for healthcare information and advice; a go-to marketplace for health services, payments, and benefits, all through a few simple taps on a consumer’s phone. One of our larger consumer offerings is Medicare Advantage, which I’d like to touch on briefly. We’re proud of our long track record of growth and of delivering for the people who choose our offerings. During the recently completed annual enrollment period, we added about 100,000 more consumers, and we remain committed to our full-year goal of 450,000 to 550,000.”

In the final three months of fiscal 2023, revenue rose in double-digits across all components of the business, with the core Premiums division growing by 13%. Segment-wise, Optum, the company’s online healthcare delivery arm, performed exceptionally well. At $94.4 billion, total Q4 revenue was up 14% and above Wall Street’s forecast. Consequently, adjusted profit moved up 15% annually to $6.16 per share.

Data Breach

Last year, UnitedHealth suffered a setback when a ransomware group breached the company’s Change Healthcare platform and stole millions of sensitive records including health and insurance data. While the data breach exposes the vulnerability of the system, the company is facing multiple lawsuits for failing to safeguard patients’ personal information.

The twelve-month average value of UNH is slightly above $500. The stock had a soft start to the week and the trend continued on Thursday.