Over the years, Walmart Inc. (NYSE: WMT) has constantly diversified while maintaining its dominance in the retail world. The company is preparing to report financial results for the first three months of fiscal 2025. The retail giant has a good track record of successfully navigating market challenges, including recent macro uncertainties, by delivering value for customers through competitive prices and convenience.

WMT rose to an all-time high in March, and the stock has gained about 10% in the past six months. The company raised its dividend by 9% this year and currently offers a yield of about 4%, which is well above the S&P 500 average. The positive outlook on the business indicates the stock will continue to be an investors’ favorite in the foreseeable future.

Q1 Report Due

When the Bentonville-headquartered company reports first-quarter results on May 16, at 7:00 am ET, the market will be looking for earnings of $0.52 per share. In the year-ago quarter, the company had earned $0.49 per share. The consensus revenue estimate is $159.41 billion, vs. $152.3 billion in the year-ago quarter.

After successfully transitioning from a brick-and-mortar-focused retailer to an omnichannel player — by building a strong e-commerce platform and setting up an extensive network of fulfillment centers — Walmart is now betting on its advertising business to boost revenues. E-commerce sales grew about 20% in fiscal 2024 and crossed $100 billion for the first time. The Walmart Connect advertising platform allows sellers to run campaigns, targeting their ads based on customers’ shopping habits, demographics, and product categories.

Tech Push

Interestingly, Walmart delivered decent profit margins last year despite keeping its prices low. The retailer has always strived to gain an edge over its peers like Target and Costco by integrating advanced technology, with the latest being the launch of AI-powered search and delivery using unmanned aerial vehicles. The company targets to make drone delivery available to about 75% of households in Dallas-Fort Worth by the end of this year.

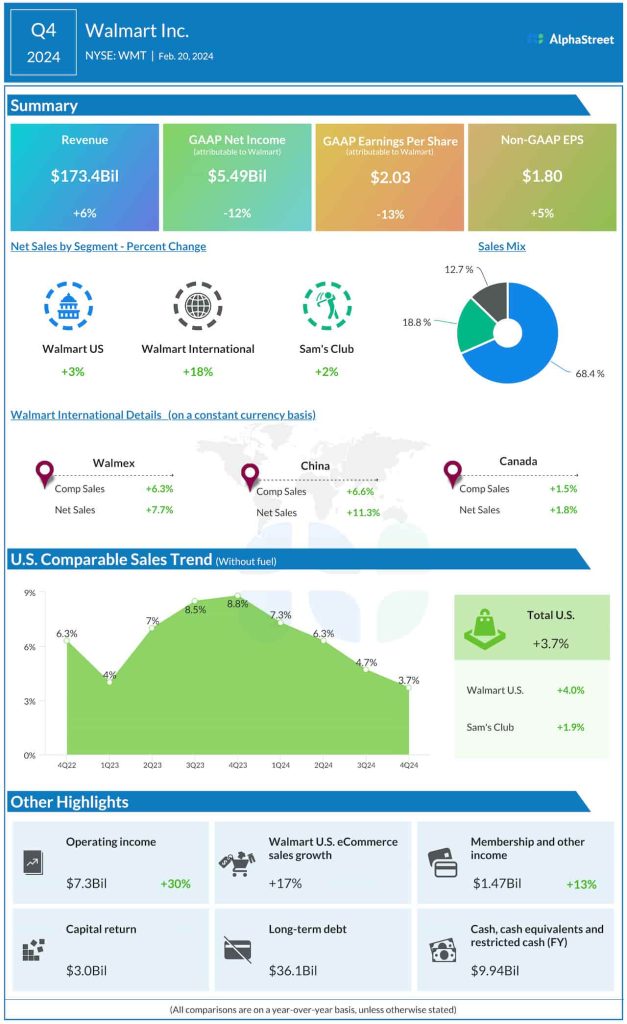

From Walmart’s Q4 2024 earnings call:

“Beyond our stores and clubs, we’re continuing to strengthen our first- and third-party e-commerce capabilities and scale those businesses around the world. The combination of the marketplace and the commissions that go with it, fulfillment services, membership, advertising, and our smaller but fast-growing data monetization business enable us to grow our bottom line faster than our top line while delivering everyday low prices for our customers and investing in our associates at the same time.”

Strong FY24

Walmart’s quarterly sales beat estimates consistently for about four years, and the trend continued in the fourth quarter when revenues increased 6% annually to $173.4 billion. Sales grew across all three operating segments – Walmart US, Walmart International, and Sam’s Club. Comparable store sales rose 3.7%, but growth decelerated for the fourth consecutive quarter.

E-commerce sales increased 17% in Q4, continuing the recent trend. Adjusted profit decreased 5% annually to $1.80 per share. Earnings also exceeded expectations, marking the seventh beat in a row. On a reported basis, net income declined in double digits to $5.49 billion or $2.03 per share.

Walmart’s stock has been above its 12-month average for over three months. On Thursday, it traded slightly above $60.