After ending the last fiscal year on a positive note, Cisco Systems (NASDAQ: CSCO) is all set to publish first-quarter results Wednesday after the closing bell. In the last report, the management had predicted that October-quarter earnings would be in the $0.80-0.82 per-share range, on modest revenue growth.

Analysts’ consensus earnings estimate for the first quarter is $0.81 per share, which represents an 8% increase from last year. Revenues are expected to be $13.08 billion.

The San Jose, California-based network gear maker has dominated the switch and router market for long, a trend that is expected to have added to top-line growth this time. Like in the past, uncertainties in China, a prominent market for the tech firm, and its tariff dispute with the US could impact the performance negatively. Initial estimates show that the unfavorable macroeconomic backdrop continues to be a drag on order growth.

Nevertheless, the results will likely benefit from the recent updates to the highly successful Catalyst 9000 series of switches, which were introduced a couple of years ago, besides the company’s popular offerings in the wireless division, including the Meraki solutions and Wave 2 access points.

Growth Drivers

The new trends in the data center market are turning out to be boon for Cisco, especially the rapid shift to the high-speed 400G architectures, as it has been with the widespread adoption of cloud technology.

The solid momentum in the software subscription business, a relatively new area for the company, and the growing demand for its cybersecurty offerings are expected to have contributed to growth in the early months of the fiscal year. There has been a marked increase in enterprise spending on data security and 5G networks, another promising area as far as Cisco is concerned.

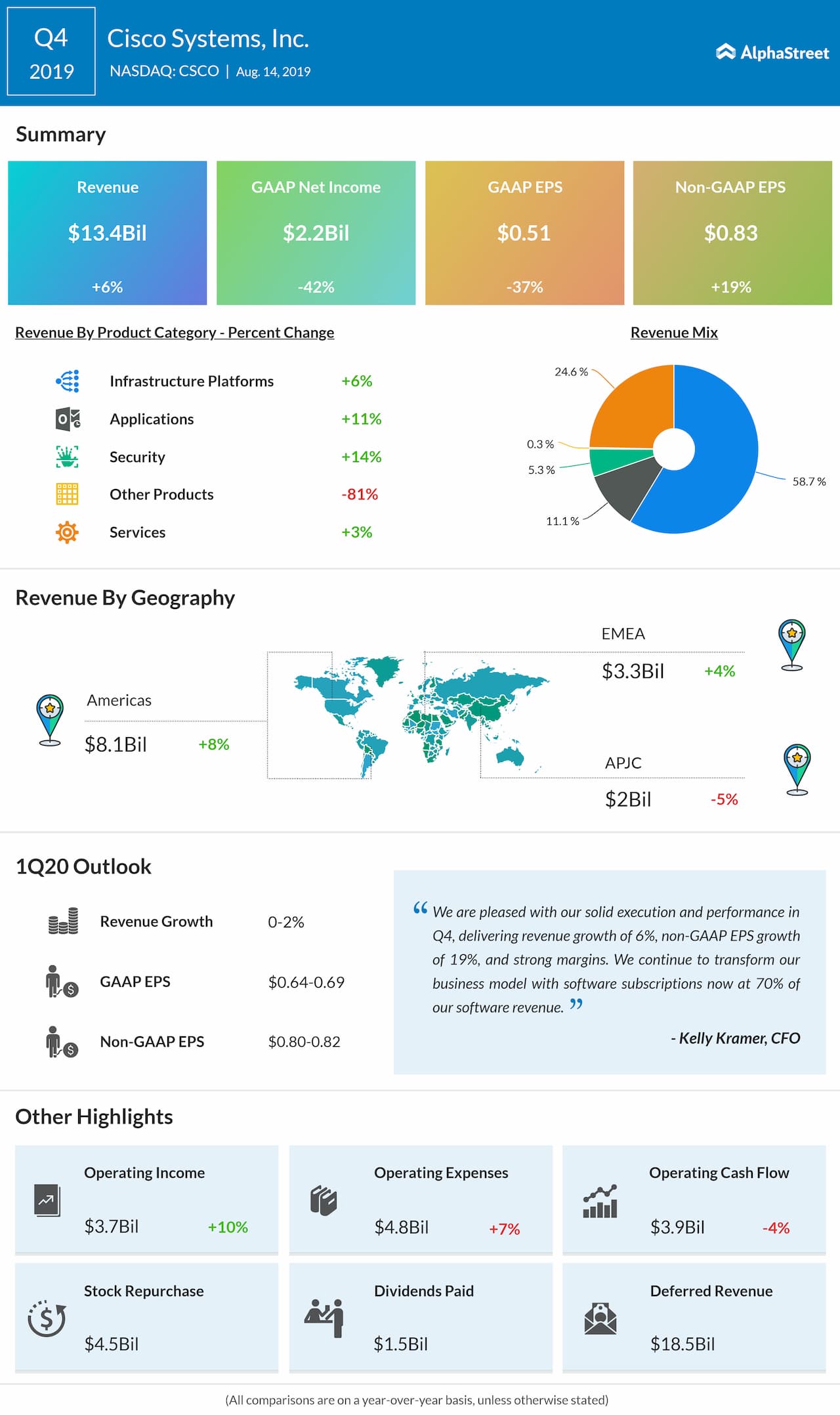

Q4 Outcome

In the July-quarter, revenues declined 6% annually to $13.4 billion, as estimated by analysts. Supported by the positive top-line performance, adjusted earnings rose 19% annually to $0.83 per share and exceeded the forecast.

Peer Performance

Reflecting the challenging market conditions, rival router maker Juniper Networks (JNPR) last month said its third-quarter earnings declined in double digits to less than 50 cents even as revenues dropped 4%.

Shares of Cisco hit a nine-year high in July and declined 16% since then. On Monday, the stock traded slightly below the $50-mark, close to the levels seen a year earlier.