PepsiCo Inc. (NASDAQ: PEP) is scheduled to report second quarter 2019 earnings results on Tuesday, July 9, before market open. Earnings are estimated to decline 7.5% year-over-year to $1.49 per share while revenues are projected to increase 2% to $16.4 billion. Over the trailing four quarters, the company has topped earnings estimates three times.

PepsiCo’s topline results are expected to benefit from the

strong performance of the snacks business, which continues to deliver solid revenues.

The beverages business is also slightly gaining momentum and this could add to

the gains in the quarter. However, the company continues to see weakness in the

Quaker Foods North America segment which is likely to dent the topline.

PepsiCo continues to boost its strong product portfolio through

innovation and strategic partnerships. The company recently teamed up with

Lavazza to launch iced coffee in the UK. PepsiCo’s diversification efforts

through various acquisitions and partnerships are likely to pay off in driving

growth going forward.

Although the company is dealing with changing customer preferences in the US, it is seeing growth outside the US, particularly in emerging markets. This growth is likely to prove beneficial to the results in the second quarter. PepsiCo has also been taking measures to reduce costs and this is likely to help profitability.

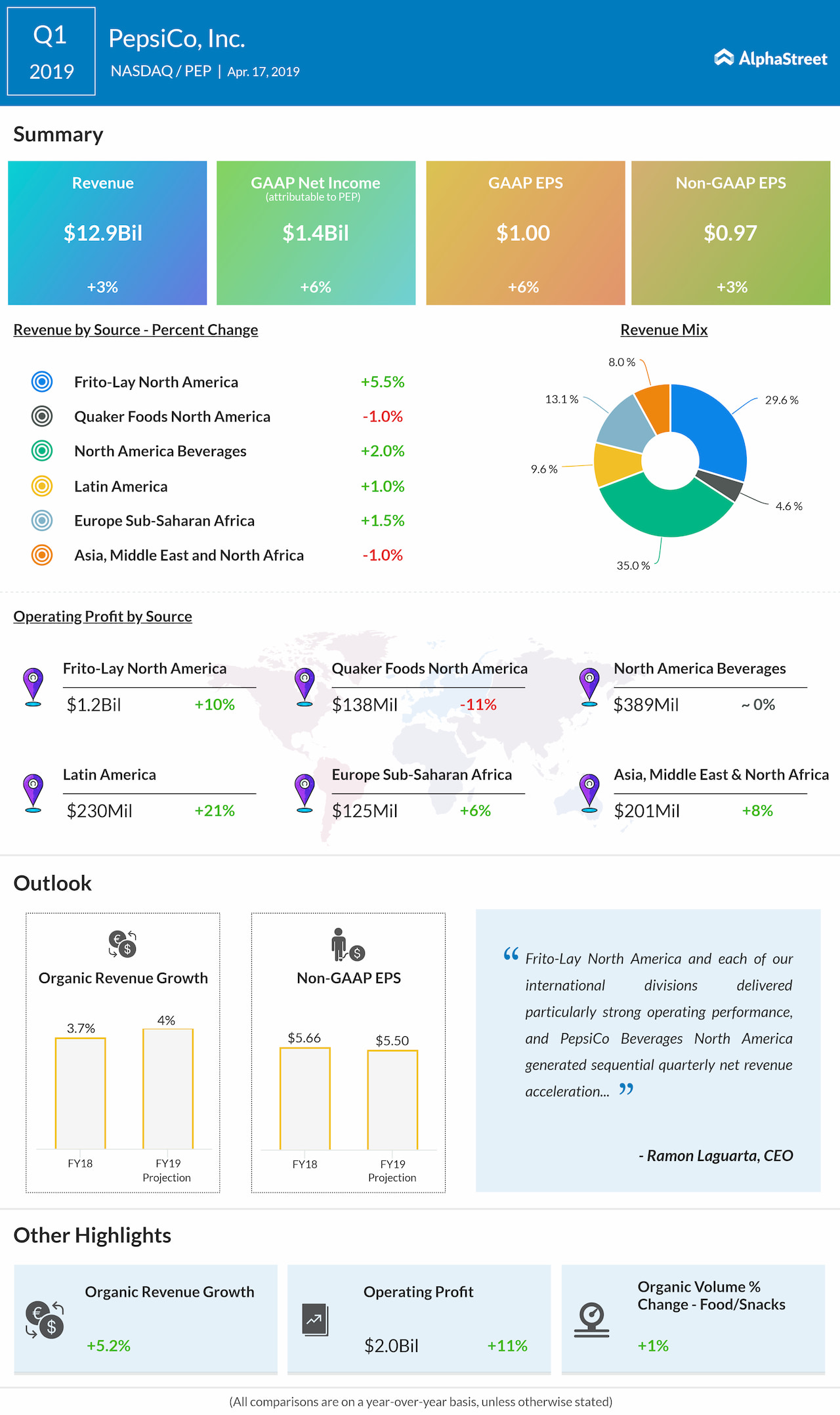

In the first quarter of 2019, PepsiCo beat revenue and earnings estimates. Both revenue and adjusted EPS grew 3% year-over-year. The company posted revenue growth across all its segments, barring Quaker Foods North America and AMENA.

For the full year of 2019, PepsiCo expects organic revenue to grow 4% and core constant currency EPS to decline 1%. PepsiCo’s shares have gained 19% thus far this year and 23% over the trailing 52 weeks.