Darden Restaurants, Inc. (NYSE: DRI), a full-service restaurant operator, has faced margin pressure this year from higher input costs tied to tariffs on key commodities. Despite that, management remains optimistic, pointing to growth initiatives such as first-party delivery and an expanding restaurant footprint. Still, softer discretionary spending and evolving consumer dining preferences pose risks to sustaining momentum.

Estimates

Darden’s second-quarter 2026 earnings report is scheduled for release on December 18 at 7 am ET. Wall Street analysts project adjusted earnings of $2.1 per share for the November quarter, on sales of $3.08 billion. A year earlier, the company had posted net income of $2.03 per share and sales of $2.89 billion. The company’s popular brands, Olive Garden and LongHorn Steakhouse, continue to benefit from strong consumer demand for casual dining.

Orlando, Florida-based Darden’s stock has declined more than 18% since hitting an all-time high mid-year, with the downturn accelerating in the past three months. DRI regained momentum over the past month, and the uptrend continues ahead of earnings. The management has regularly increased quarterly dividends, with the latest, a 7% increase in September 2025, representing an above-average yield of 2.8%.

Key Metrics

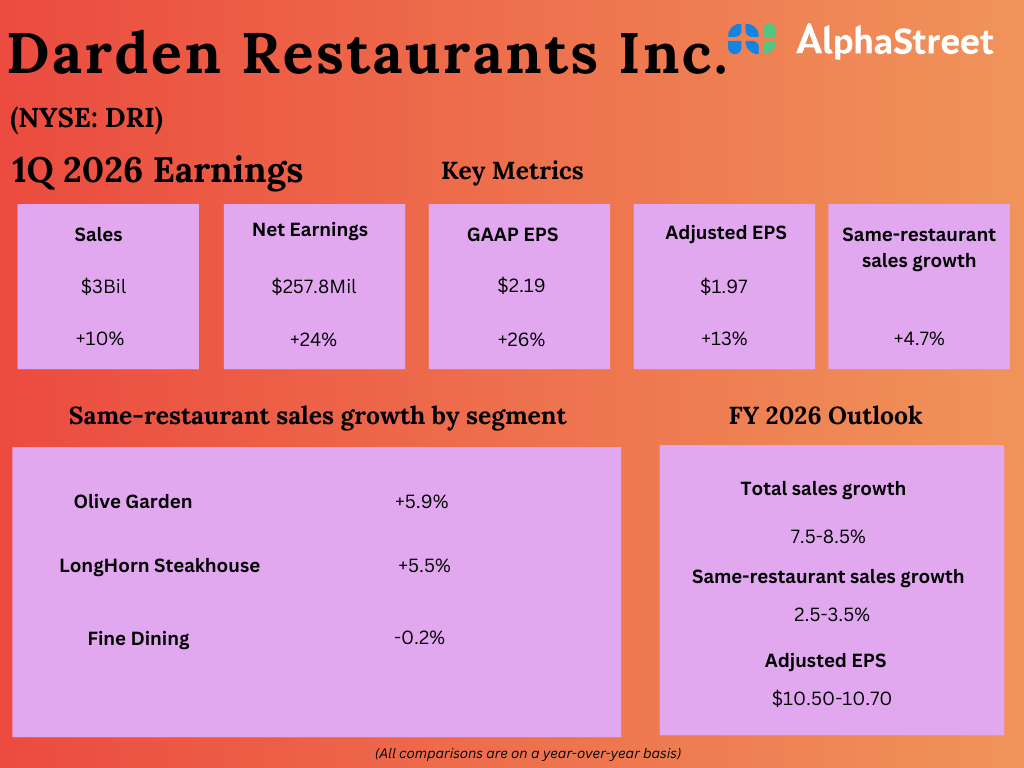

In the first three months of FY26, Darden’s total sales increased 10.4% year-over-year to $3 billion, with blended same-restaurant sales growing 4.7%. Net income was $257.8 million or $2.19 per share in Q1, compared to $207.2 million or $1.74 per share in the year-ago quarter. On an adjusted basis, earnings rose 12.6% to $1.97 per share. However, the numbers fell short of expectations. The management said it expects sales growth of 7.5-8.5% and same-restaurant sales growth of 2.5-3.5% for fiscal 2026, revised up from the previously issued outlook. The forecast for full-year adjusted earnings is between $10.50 per share and 10.70 per share.

From Darden Restaurant’s Q1 2026 Earnings Call:

“While we are reiterating our full-year earnings per share guidance, we expect the lowest year-over-year EPS growth to be in the second quarter, driven by the significant step-up in beef costs and our measured approach to pricing for these costs. We expect our pricing for the second quarter to be approximately 100 basis points below total inflation. We have a proven track record of successfully navigating through higher costs, and we’ll continue to take a disciplined approach to ensure the long-term health of our business. We believe our strategy remains the right one for our company.”

Road Ahead

The Darden leadership is betting on initiatives like the Buy One, Take One promotion, primarily at Olive Garden, and first-party delivery to deal with macro challenges and drive traffic. Upward revision of the full-year sales forecast underscores the management’s confidence in its growth strategy. Meanwhile, increasing input costs, particularly higher beef prices, are eating into the company’s margins.

On Monday, Darden’s stock opened at $183.28, which is 7% lower than its 12-month average price. The shares have grown about10% in the past twelve months.