After recovering from a rough patch, Micron Technology Inc. (NASDAQ: MU) is preparing to report fourth-quarter results next week, even as the market keeps a close watch on the event to get a sense of the chipmaker’s financial health. The company bets on the growing demand for its high-margin AI-related products like High Bandwidth Memory to stay on the growth path.

Micron’s stock, having fallen from its mid-June high, is currently trading close to where it was at the beginning of the year. The shares have lost 5.5% in the past six months. Considering the relatively low price and the company’s AI-driven growth prospects, MU looks like a good investment option.

Estimates

According to analysts, Micron swung to a profit of $1.03 per share in the fourth quarter from a loss of $1.07 per share in the same period of fiscal 2023. The improvement is driven by an estimated 72% surge in Q4 revenues to $6.91 billion. The report is slated for release on Wednesday, September 25, at 4:05 pm ET.

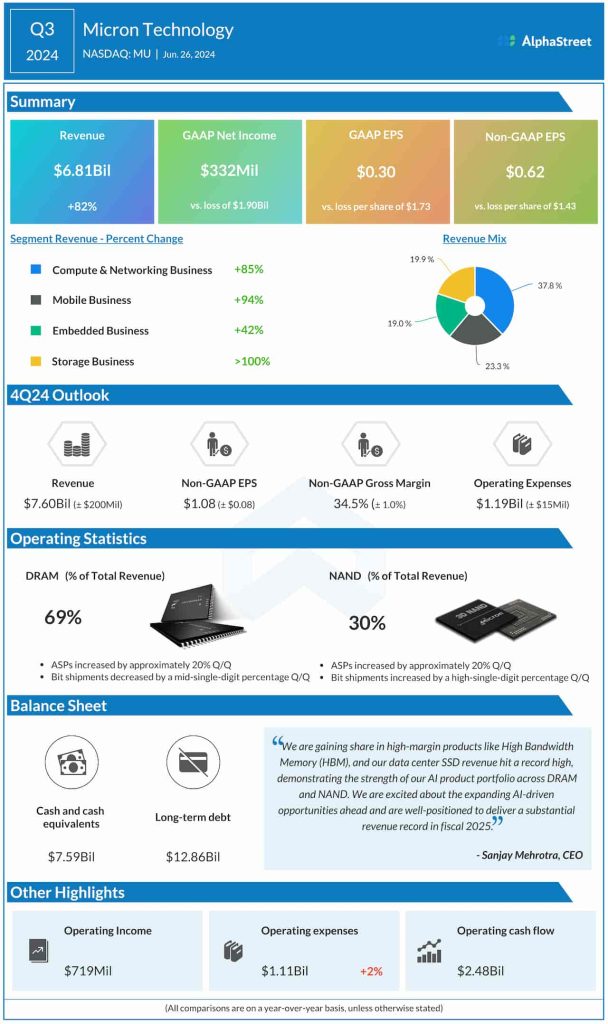

Earlier, encouraged by the strong Q3 outcome, the Micron leadership said it expects fourth-quarter revenues to increase to $7.6 billion. It is looking for adjusted earnings of $1.08 per share for the August quarter. The guidance for adjusted gross margin is approximately 34.5% while operating expense is expected to be around $1.19 billion in Q4.

AI Power

Micron’s aggressive AI integration across the DRAM and NAND portfolios has resulted in data center SSD revenue climbing to a record high in the most recent quarter. Taking a cue from the favorable demand-supply environment, the management implemented significant price increases, driving profit growth across all end markets. That, combined with expanding share in AI-related product types like high-capacity DIMMs and data center SSDs, should enable the company to meet its growth goals. Recently, Micron signed an MoU for a government grant of around $6 billion, to support its planned memory manufacturing expansion at the Idaho facility.

“Robust AI-driven demand for data center products is causing tightness on our leading-edge nodes. Consequently, we expect continued price increases throughout calendar 2024 despite only steady near-term demand in PCs and smartphones. As we look ahead to 2025, demand for AI PCs and AI smartphones and continued growth of AI in the data center creates a favorable setup that gives us confidence that we can deliver a substantial revenue record in fiscal 2025, with significantly improved profitability underpinned by our ongoing portfolio shift to higher-margin products,” said Micron’s CEO Sanjay Mehrotra in a recent statement.

Strong Results

In the third quarter, revenues jumped to $6.81 billion from $3.75 billion in Q3 2023. Revenue grew sharply across all four operating segments. The tech firm reported earnings of $0.62 per share for the May quarter, excluding special items, compared to a loss of $1.43 per share a year earlier. Both revenue and profit beat Wall Street’s estimates for the fifth time in a row. Unadjusted net income was $332 million or $0.30 per share in Q3, compared to a loss of $1.90 billion or $1.73 per share last year.

Micron’s shares opened Tuesday’s session at $87.18 and traded higher in the early hours. It is below the long-term average price of $98.06.