AlphaStreet Newsdesk powered by AlphaStreet Intelligence

DEA|Core FFO Per Share $0.77 vs $0.09 est (+755.6%)|Rev $91.5M vs $88.3M est (+3.7%)|Net Income $1.4M

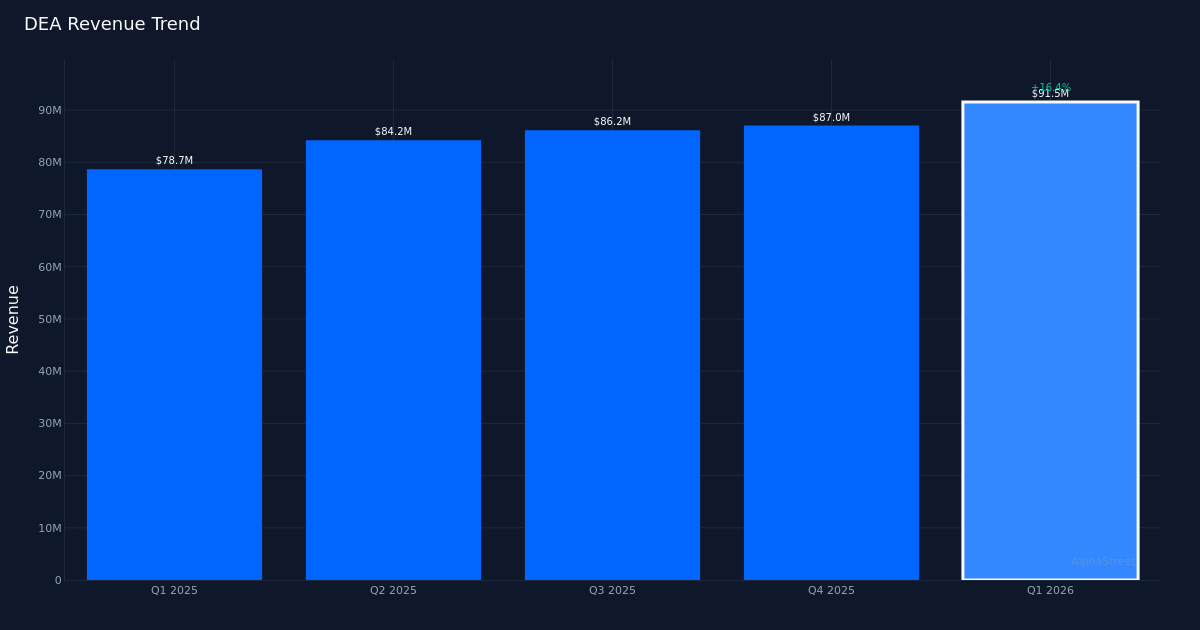

DEA|Core FFO Per Share $0.77 vs $0.09 est (+755.6%)|Rev $91.5M vs $88.3M est (+3.7%)|Net Income $1.4MEasterly Government Properties (DEA) delivered a dramatic bottom-line beat in Q1 2026, surging past analyst expectations with core FFO per share of $0.77 versus the $0.09 consensus estimate. The government-focused office REIT reported revenue of $91.5M, edging past the $88.3M estimate by 3.7%, while the stock climbed 1.5% to $23.52 on the results. This marks a clean sweep for the company, beating on both top and bottom lines. The magnitude of the EPS surprise—driven by an adjusted earnings per share that increased year-over-year—signals either a significant operational inflection or one-time tailwinds that merit deeper scrutiny.

The earnings quality picture reveals tension between top-line momentum and margin compression that warrants caution. While revenue grew a robust 16.3% year-over-year from $78.7M to $91.5M, net margin deteriorated 2.8 percentage points from 4.3% in Q1 2025 to just 1.5% in the current quarter. Net income declined from $3.4M a year ago to $1.4M this quarter, meaning the company delivered less absolute profit despite pulling in nearly $13M more in revenue. This inverse relationship—expanding revenue paired with contracting net income—suggests the growth came at a price, likely through higher operating costs or financing expenses that outpaced the benefit of scale. The 1.5% net margin ranks among the thinnest for REITs and raises questions about sustainable profitability as the portfolio scales.

EBITDA performance provides a more encouraging view of operational health, though even here growth lags revenue expansion. EBITDA increased to $57.3 million from $51 million last year, representing approximately 12% growth. The $57.3M EBITDA figure translates to a 62.6% EBITDA margin on the $91.5M revenue base, which demonstrates the underlying cash generation capability of government-leased properties. Yet the 12% EBITDA growth rate trails the 16.3% revenue growth, pointing to operational leverage that’s working in reverse—costs are growing faster than the top line, a dynamic that typically emerges during rapid expansion phases when integration costs and startup inefficiencies temporarily depress margins.

The four-quarter revenue trajectory shows consistent sequential acceleration that validates the growth thesis. Revenue climbed from $84.2M in Q2 2025 to $86.2M in Q3 2025, then $87.0M in Q4 2025, and finally $91.5M in Q1 2026. This pattern of consecutive quarterly growth—with each quarter setting a new high-water mark—demonstrates that the 16.3% year-over-year increase isn’t a one-quarter anomaly but rather the continuation of a sustained upward trajectory. Operating across 106 properties, the company has achieved scale that should theoretically support better margins, making the net margin compression all the more noteworthy.

Guidance for FY 2026 sets modest expectations that seem conservative given Q1’s explosive beat. The company projects full-year Core FFO/share of $3.06 to $3.12, with a midpoint of $3.09. Annualizing the Q1 number of $0.77 oer share would yield approximately $3.08 for the year, essentially matching guidance midpoint. Management framed this as favorable relative to sector peers, noting “as we look at our earnings that we’re delivering for shareholders this year, the midpoint of the range is 3% growth, again, which I think is very favorable relative to the REIT sector, especially given our sort of AA plus revenue stream.”

Funds From Operations (FFO) metrics better reflect REIT operating performance. On a reported basis, FFO per share increased to $0.76, up from $0.71, representing approximately 7% growth. The $0.77 core FFO per share aligns precisely with the adjusted EPS figure.

Capital allocation commentary signals a measured approach to pipeline development that could support future growth. When discussing development opportunities, CEO Darrell Crate noted, “Yeah, I mean, look, it’s, it’s a terrific way for us to get involved early in a project and I think we could see ourselves allocating about $30 million to this pipeline.” This relatively modest capital commitment—representing roughly one-third of quarterly revenue—suggests disciplined growth rather than aggressive expansion. For a REIT managing 106 properties, adding selectively to the pipeline while maintaining the quality of government tenants should support the 3% growth trajectory embedded in guidance without stretching the balance sheet.

The muted 1.5% stock price response to the strong earnings beat reflects market sophistication in parsing GAAP versus operating metrics. At $23.52, investors appear to be discounting the headline EPS figure and focusing instead on the core FFO growth of 5.5% and the forward guidance implying 3% full-year expansion. The stock’s modest uptick suggests the market views this quarter as solid execution rather than a transformative inflection, appropriate for a government-leased office REIT where volatility is typically low and growth is steady but unspectacular.

This content is for informational purposes only and should not be considered investment advice. AlphaStreet Intelligence analyzes financial data using AI to deliver fast and accurate market information. Human editors verify content.