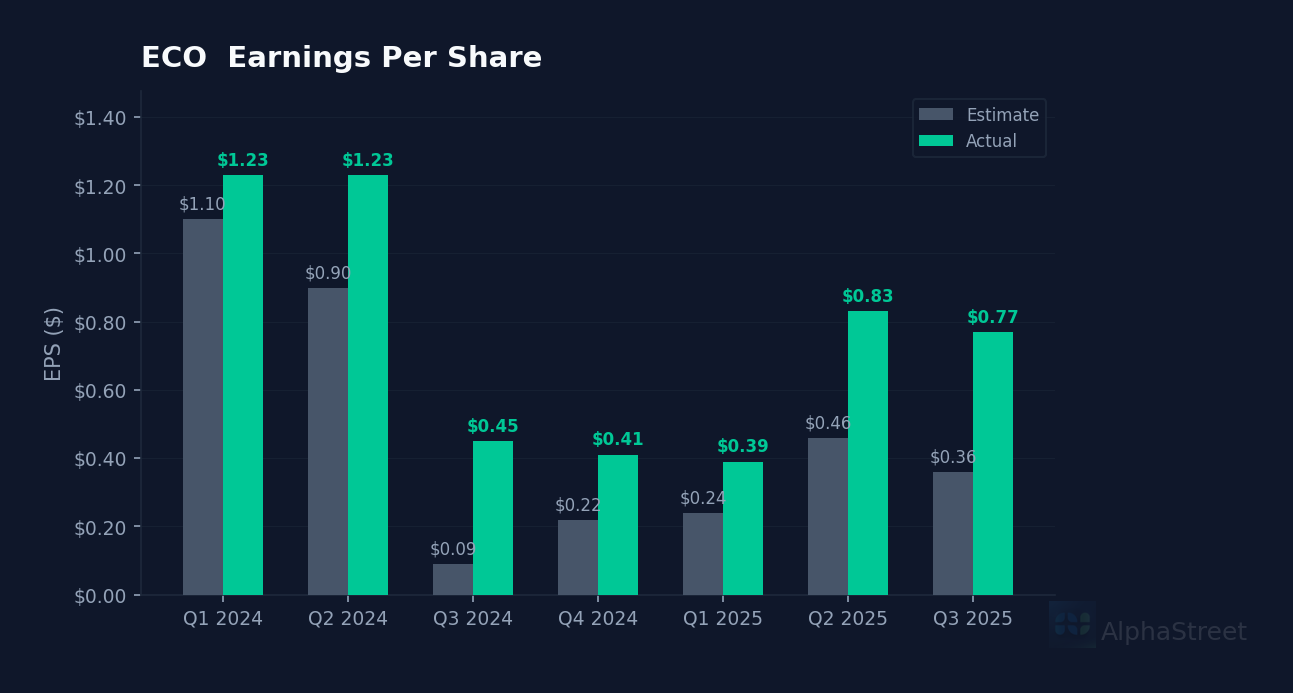

Blowout quarter doubles estimates. Okeanis Eco Tankers (ECO) posted Q4 2025 earnings per share of $0.77, crushing the consensus estimate of $0.36 by 113.9%. Revenue landed at $349.9M, up 6.7% year-over-year. Shares jumped 3.7% in extended trading to $44.64, extending a powerful rally that’s seen the stock climb 19.1% over the past three months as tanker rates remained elevated.

Six-quarter streak of outperformance. This marks the sixth consecutive quarter ECO has beaten analyst estimates, with surprise percentages ranging from 36.7% to 400%. The marine shipping operator’s trailing twelve-month EPS now sits at $2.38, implying a forward P/E of 17.9x—modest for a company consistently delivering triple-digit upside to expectations. Operating margin of 38.3% and profit margin of 21.9% highlight the operational leverage inherent in the tanker business when day rates support premium earnings.

Recent capital raise positions for growth. On November 19, 2025, OET completed a $115 million equity offering of 3.2 million new shares following strong institutional demand. The timing—just weeks before this earnings beat—suggests management capitalized on momentum to fund fleet expansion or debt reduction while the stock traded near multi-year highs. The company operates eco-design VLCCs and Suezmax tankers, positioning it to benefit from tightening emissions regulations and the ongoing global energy transition.

Valuation disconnect persists. Despite the consistent earnings outperformance, ECO trades at just 18.8x trailing earnings with an analyst price target of $45.00—barely 0.8% above current levels. The market cap of $1.74 billion appears compressed given the company’s ability to generate $349.9M in quarterly revenue with best-in-class margins. Forward EPS estimates of $2.50 and current-quarter consensus of $0.65 suggest analysts remain conservative, creating potential for additional upside if the beat streak continues.

Tanker fundamentals remain supportive. Global crude tanker rates have stayed elevated through 2025 as refinery utilization recovered and ton-mile demand increased with shifting trade patterns. ECO’s eco-design fleet commands premium charter rates while burning less fuel—a structural advantage as IMO 2030 emissions targets approach. Management’s previous commentary from Q3 emphasized “good momentum across our core end markets,” and the Q4 results validate that trajectory held through year-end.

This article was generated using AlphaStreet’s proprietary financial analysis technology and reviewed by our editorial team.