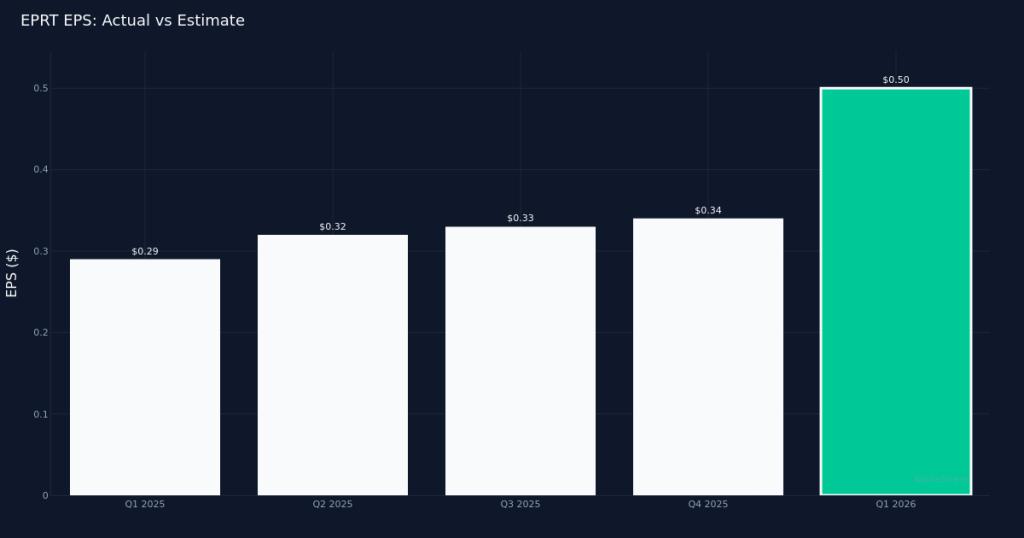

Strong Beat Drives Outperformance. Essential Properties Realty Trust, Inc. (NYSE:EPRT) delivered a commanding Q1 2026 performance, posting AFFO per share of $0.50 that crushed Wall Street’s $0.37 estimate by 35.1%. The retail-focused REIT generated $158.8M in revenue for the quarter, marking a 22.8% increase from the $129.4M recorded in Q1 2025. Net income reached $105.8M for the quarter, underscoring the quality of the company’s net lease portfolio strategy. Despite the impressive results, shares declined 2.7% to $32.08, suggesting investors may be digesting the sharp rally preceding the print or repositioning ahead of the company’s ambitious full-year targets.

Portfolio Scale Underpins Growth. The REIT’s operational footprint expanded to 2,417 total properties at quarter end, providing a diversified base of rent-generating assets across the retail landscape. This scale advantage appears to be translating directly to the bottom line, as evidenced by Funds from Operations per share of 1 for the quarter. The substantial revenue growth of 22.8% year-over-year points to a combination of accretive acquisitions and strong rent collections rather than mere cost management, which bodes well for the sustainability of EPRT’s earnings trajectory. The company’s ability to convert top-line momentum into meaningful net income of $105.8M demonstrates operational efficiency within its net lease business model.

Ambitious Guidance Signals Confidence. Management laid out full-year FY 2026 expectations that reflect continued expansion, projecting adjusted EPS of $2.00 to $2.05 alongside revenue guidance of $1.10B to $1.50B. The wide revenue range suggests management is preserving flexibility around acquisition timing and deployment of capital, though the midpoint would imply sequential acceleration from the Q1 run rate. At the midpoint, the annual EPS target of approximately $2.03 would represent roughly four times the Q1 AFFO per share result, indicating management anticipates either improving margins or accelerating operational performance through the balance of the year.

Bullish Street Sentiment Intact. The analyst community remains decidedly optimistic on EPRT’s prospects, with Wall Street consensus standing at 17 buy ratings, 3 hold ratings, and zero sell recommendations. This overwhelmingly positive stance reflects confidence in the company’s net lease strategy and its ability to source attractive retail properties in an environment where many traditional retailers are rationalizing their real estate footprints. The 35.1% earnings beat should reinforce conviction among the bull camp, though the post-earnings stock decline of 2.7% suggests some profit-taking after what was likely a strong run into the print.

This article was generated with the assistance of AI technology and reviewed for accuracy. AlphaStreet may receive compensation from companies mentioned in this article. This content is for informational purposes only and should not be considered investment advice.