Shares of Estée Lauder (NYSE: EL) gained 12% on Monday, after the company reported its earnings results for the second quarter of 2024. Although revenue and earnings declined year-over-year, both surpassed analysts’ projections. The company revised its outlook for the full year and outlined its profit recovery plan, which now includes a restructuring program.

Quarterly performance

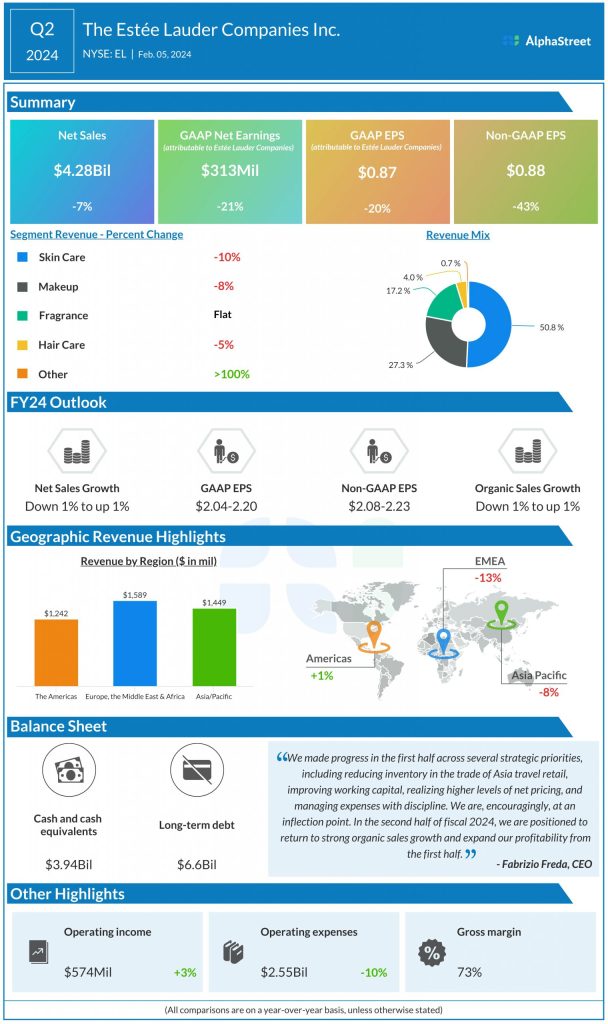

Estee Lauder’s net sales decreased 7% year-over-year to $4.28 billion in Q2 2024 but beat estimates of $4.1 billion. Organic sales fell 8% due to challenges in Asia travel retail and softness in prestige beauty in China. GAAP net income decreased 21% to $313 million, or $0.87 per share. Adjusted EPS fell 43% to $0.88 but surpassed projections of $0.55.

The company saw sales decline across most of its product categories and geographic regions during the second quarter. Sales in the Skin Care and Makeup categories declined 10% and 8%, mainly due to headwinds in the Asia travel retail business. Fragrance sales remained flat while Hair Care sales fell 6%, hurt by softness in North America.

EL’s sales in the Americas region dipped 1%, mainly due to a decline in North America which was partly offset by double-digit growth in Latin America. Sales fell 14% in the Europe, Middle East & Africa region, due to weakness in Asia travel retail as well as business disruptions in Israel and parts of the Middle East. Sales decreased 7% in Asia/Pacific, mainly due to challenges in China.

Outlook

For the third quarter of 2024, net sales are projected to increase 3-5% while organic sales are expected to rise 4-6% versus the prior-year period. Reported EPS is estimated to range between $0.35-0.46 and adjusted EPS is expected to range between $0.36-0.46.

For the full year of 2024, reported and organic sales are both expected to range between down 1% to up 1% compared to last year. Reported EPS is expected to range between $2.04-2.20 while adjusted EPS is expected to range between $2.08-2.23.

Profit recovery plan

Estee Lauder expanded its profit recovery plan for fiscal years 2025 and 2026 to include a restructuring program. The boosted plan aims to improve gross margins, and reduce costs and overhead expenses, while increasing investments in key consumer-facing activities.

The restructuring program will begin in Q3 2024 with specific initiatives expected to be substantially completed by the end of FY2026. As part of its restructuring program, the company plans to reduce around 3-5% of its positions. It expects to incur restructuring and other charges of between $500-700 million, before taxes. The program is expected to yield annual gross benefits of between $350-500 million, before taxes.