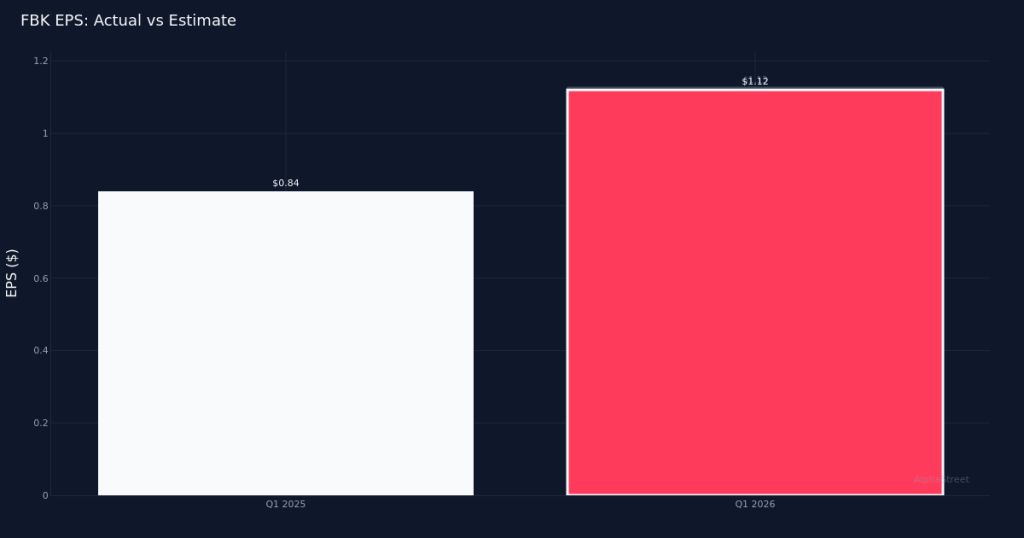

Narrow Miss. FB Financial Corporation (NYSE:FBK) reported Q1 2026 adjusted diluted earnings of $1.12 per share, falling just short of the $1.13 consensus estimate by 0.9%. Despite the modest earnings shortfall, the Nashville-based regional bank delivered a strong revenue performance, generating $172.3M for the quarter—a 31.9% increase from the $130.7M recorded in Q1 2025. Adjusted net income reached $58.3M for the quarter, underscoring the company’s continued profitability amid a dynamic operating environment for regional banks.

Revenue-Driven Growth. The quality of FB Financial’s performance appears solid, with the year-over-year revenue expansion driving results rather than aggressive cost-cutting measures. The 31.9% revenue growth demonstrates strong momentum in the company’s core banking operations, suggesting healthy net interest income and fee generation across its 90 total bank branches at quarter end. This top-line strength is particularly noteworthy for a regional bank navigating the current interest rate environment, indicating effective loan origination and deposit management strategies that should provide a sustainable foundation for future earnings.

Balance Sheet Positioning. Loans held for investment (HFI) stood at $12.50B for the quarter, a critical metric for evaluating the bank’s lending activity and asset quality. This loan portfolio size reflects FB Financial’s positioning within the regional banking landscape and its capacity to generate net interest income. The relationship between this loan base and the company’s branch network suggests reasonable deployment of capital across its Tennessee and surrounding market footprint, though investors will be keen to understand credit quality trends and any changes in loan mix composition as the year progresses.

Market Reaction. Shares of FBK traded up following the earnings release, suggesting investors looked past the slight earnings miss to focus on the robust revenue growth and solid profitability metrics. The positive stock reaction indicates that the market views the company’s trajectory favorably, with the top-line performance apparently outweighing concerns about the marginal earnings shortfall. Wall Street consensus currently stands at 6 buy ratings, 3 hold ratings, and 0 sell ratings, reflecting generally constructive sentiment toward the regional bank’s prospects.

This article was generated with the assistance of AI technology and reviewed for accuracy. AlphaStreet may receive compensation from companies mentioned in this article. This content is for informational purposes only and should not be considered investment advice.