The freight forwarding industry is one among the several sectors which were badly affected by the trade war, and the recent escalation of the US-China standoff points to further deterioration of the market conditions. After issuing a dismal outlook for the current fiscal year a few months ago, shipping giant FedEx (FDX) will be reporting its third-quarter earnings on March 19 after the closing bell.

Market watchers are looking for a 15% decline in earnings to $3.17 per share, while revenues are forecast to grow 7% to $17.69 billion. Since their initial release, the estimates were trimmed to reflect the bearish sentiment among a section of analysts. Considering the downgrade and the earnings misses in the trailing two quarters, the chances of third-quarter profit beating the Street view are bleak.

Of late, cargo companies have been facing competition from Amazon (AMNZ) as the tech firm continues to expand its presence in the transport sector. Given the e-commerce giant’s track record of diversifying successfully, the threat it poses to cargo companies like FedEx and United Parcel Service (UPS) cannot be ignored.

Since their initial release, the estimates were trimmed to reflect the bearish sentiment among the analysts

With the new equations putting additional pressure on market share, FedEx needs to ease the strain on margins by continuing its cost-cutting initiatives. Efforts should also be made to expedite the integration of TNT Express, which has not been completed, though the acquisition was closed several months ago.

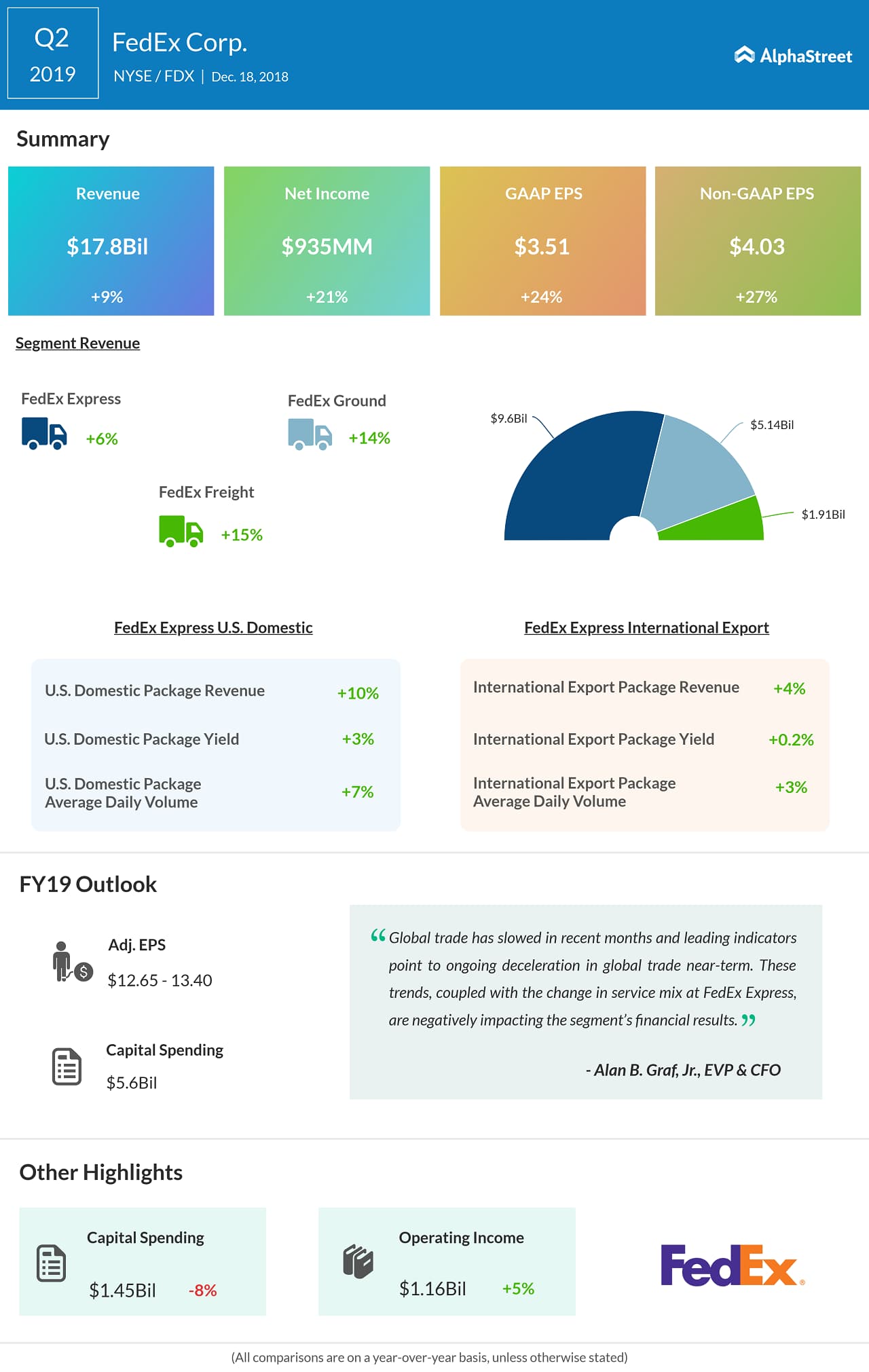

When results for the second quarter of 2019 were published, the positive sentiment over the impressive outcome was spoiled by the downward revision of the full-year earnings outlook by the management. Though adjusted earnings and revenues rose to $4.03 per share and $17.8 billion respectively, the stock dropped.

Related: Listen to FedEx quarterly earnings conference calls

In January, rival cargo mover United Parcel Service posted double-digit growth in fourth-quarter adjusted earnings to $1.94 per share. It reflected broad-based revenue growth that pushed up the top-line by 5% to about $17 billion.

The recent dip in the stock price makes FedEx a promising investment option – a status that is expected to remain unchanged in the remainder of the year and beyond. The decline of the shares over the past twelve months was pretty quick, losing about 33%. However, the stock recovered from the multi-year lows seen towards the end of last year and stabilized in the early weeks of 2019.