As a Caribbean-centric institution, First BanCorp’s (FBP) risk profile is uniquely tied to regional trade dynamics. The implementation of Mexico’s “Tsunami” tariffs on January 1, 2026, which impose duties of up to 50% on non-FTA components (primarily from China), presents an indirect headwind. While First BanCorp has no direct lending to Mexican manufacturing, its commercial clients in South Florida and the Virgin Islands rely on Caribbean maritime logistics that may face increased costs if regional trade flows are disrupted.

Furthermore, the bank’s $12.7 billion core deposit base remains sensitive to federal fiscal policy. Approximately $2.7 billion in public sector deposits are subject to repricing lags and potential outflows depending on Puerto Rico’s infrastructure spending pace. Unlike mainland banks, First BanCorp must also navigate the specific geopolitical reality of the “Jones Act” and federal disaster recovery funding, which remain the primary drivers of long-term commercial loan demand in its core Puerto Rico market.

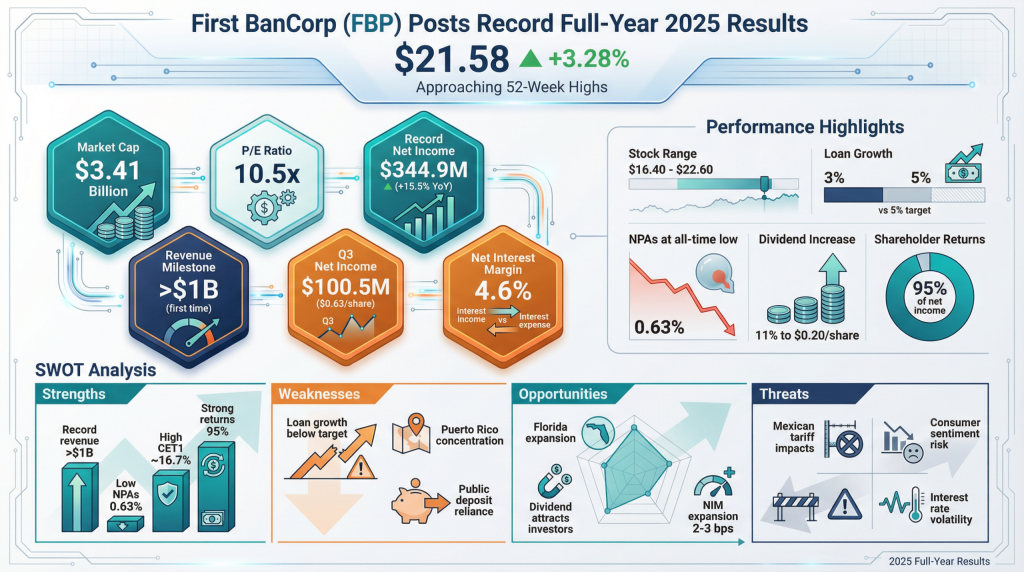

SWOT Analysis

- Strengths: Record annual revenue (> $1B); all-time low non-performing assets (0.63%); high CET1 capital ratio (~16.7%); strong shareholder returns (95% payout).

- Weaknesses: Decelerating loan growth (3% vs 5% target); high concentration in the Puerto Rico geography; reliance on public sector deposit stability.

- Opportunities: Expansion in the Florida commercial market; 11% dividend increase attracting income-focused investors; continued NIM expansion of 2-3 bps per quarter in 2026.

- Threats: Indirect impact of 2026 Mexican tariffs on regional supply chains; potential for increased credit costs if Puerto Rican consumer sentiment weakens; interest rate volatility impacting mortgage volumes.