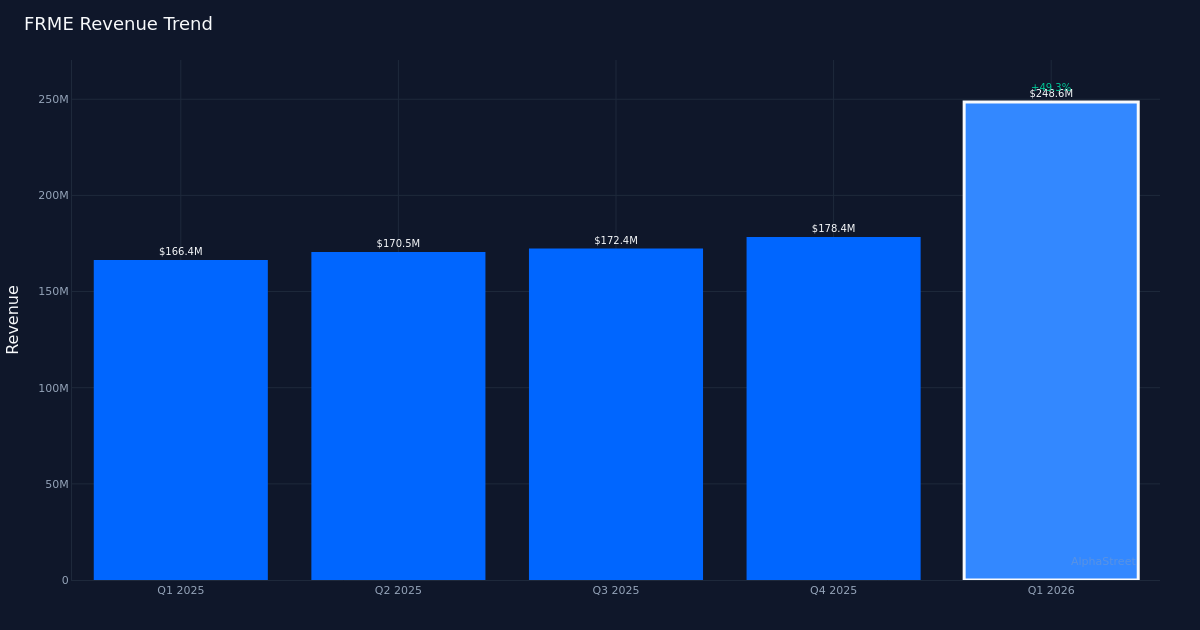

Solid beat. First Merchants Corporation (NASDAQ: FRME) reported Q1 2026 adjusted earnings of $1.03 per share, topping the $0.95 consensus estimate by 8.4%. The regional bank reported total interest income of $248.6M for the quarter, up 11.7% from $222.5M in Q1 2025, demonstrating momentum in its core banking operations. Net income reached $63.1M for the quarter, while the company’s stock traded largely unchanged following the release, suggesting investors may have anticipated the strong results or are waiting for more color on sustainability.

Revenue-driven performance. The quality of this beat appears solid, anchored by double-digit interest income growth that signals genuine business expansion rather than margin engineering through cost reduction alone. For a regional bank, an 11.7% year-over-year topline increase reflects healthy demand for lending products and deposit services in First Merchants’ operating markets. The company operated $21.1B in total assets at quarter-end, providing scale advantages as it competes against both larger national institutions and smaller community banks across its footprint.

Muted market reaction. Despite the earnings beat and topline growth acceleration, shares remained largely unchanged after the announcement. This tepid response could reflect several factors: the regional banking sector may be facing broader headwinds from interest rate concerns, investors might be seeking reassurance on asset quality metrics not disclosed in the preliminary data, or the market may have already priced in strong performance based on peer results earlier in the earnings season. The disconnect between fundamental performance and stock price movement warrants attention as more details emerge from the full earnings call.

Analyst positioning. Wall Street maintains a constructive stance on First Merchants, with consensus standing at 7 buy ratings, 3 hold ratings, and zero sell recommendations. This bullish tilt from the analyst community suggests confidence in the bank’s strategic positioning and growth trajectory, even as the stock fails to respond immediately to the quarterly beat. The absence of any sell ratings is particularly noteworthy in the current banking environment, where credit quality and interest rate sensitivity have prompted downgrades across the regional bank sector.

This article was generated with the assistance of AI technology and reviewed for accuracy. AlphaStreet may receive compensation from companies mentioned in this article. This content is for informational purposes only and should not be considered investment advice.