AlphaStreet Newsdesk powered by AlphaStreet Intelligence

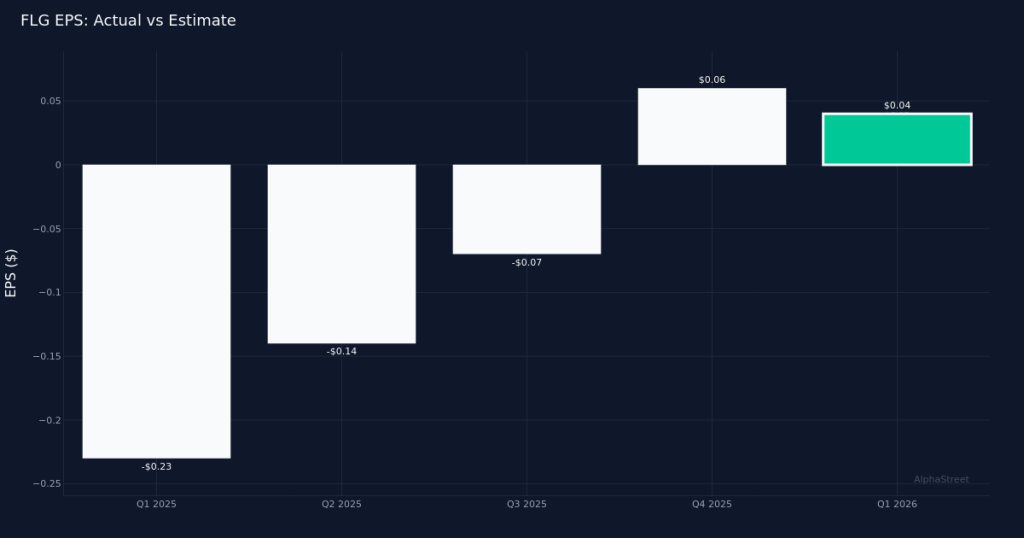

Modest Beat Delivered. Flagstar Bank, National Association (NYSE:FLG) reported Q1 2026 adjusted earnings of $0.04 per share, edging past the Street’s $0.03 consensus estimate by 33.3%. Revenue totaled $498.0M for the quarter, representing a 2.0% increase from the $490.0M recorded in Q1 2025. The regional bank’s stock traded largely unchanged following the release, suggesting investors are viewing the results as incrementally positive but not materially game-changing for the franchise.

Profitability Remains Thin. Bottom-line profit came in at $20.0M for the quarter, translating to razor-thin margins in an operating environment that continues to challenge regional banks. The modest earnings beat appears driven primarily by the top-line improvement rather than aggressive expense management, which is typically viewed more favorably by the market as it suggests sustainable revenue momentum. The 2.0% year-over-year revenue growth, while positive, reflects the headwinds facing the banking sector as net interest margins remain compressed and loan demand stays muted across many markets.

Balance Sheet Scale. Flagstar maintained total assets of $87.10B at quarter end, providing the regional bank with meaningful scale to compete against both larger money-center institutions and smaller community banks. The company’s physical footprint encompasses 340 total locations, positioning it as a significant regional player with the distribution network necessary to serve both retail and commercial banking customers. This branch network remains a competitive advantage in markets where in-person banking relationships continue to drive deposit gathering and loan origination, particularly for small and mid-sized businesses.

Mixed Street Sentiment. Wall Street analyst sentiment reflects cautious optimism, with consensus standing at 8 buy ratings and 11 hold ratings, while no analysts currently rate the shares a sell. This distribution suggests the investment community sees limited downside risk but remains unconvinced that Flagstar has identified a clear path to materially accelerate growth or expand profitability in the current rate environment. The lack of a decisive stock reaction following the earnings release reinforces this measured stance, as investors await evidence of improving loan growth, deposit stability, or margin expansion before committing fresh capital.

This content is for informational purposes only and should not be considered investment advice. AlphaStreet Intelligence analyzes financial data using AI to deliver fast and accurate market information. Human editors verify content.