AlphaStreet Newsdesk powered by AlphaStreet Intelligence

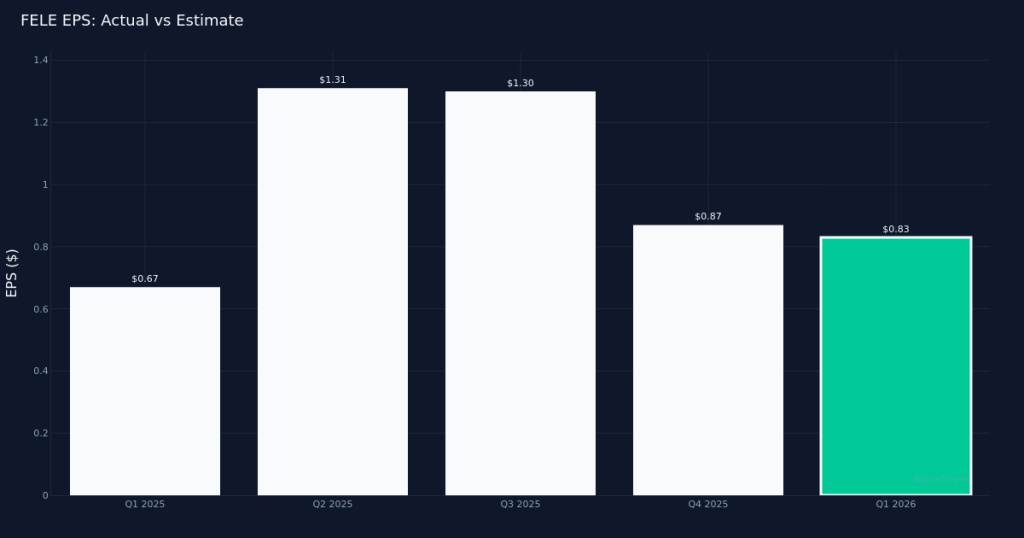

Solid beat. Franklin Electric Co., Inc. (NASDAQ:FELE) reported Q1 2026 adjusted earnings of $0.83 per share, topping the Street’s $0.77 consensus by 7.8% and signaling continued momentum in the specialty industrial machinery maker’s core water systems business. The company generated $500.4M in revenue for the quarter, representing a 10.0% increase from the $455.2M recorded in Q1 2025, with bottom-line profit coming in at $34.3M. Shares traded down 4.6% to $98.71 following the print, suggesting investors may be focusing on guidance or near-term margin dynamics despite the top-and-bottom-line beat.

Revenue-driven performance. The quality of Franklin Electric’s beat appears robust, with the double-digit revenue expansion driving the earnings outperformance rather than mere cost-cutting measures. Water Systems led segment performance with $318.0M in revenue, up 11.0% year-over-year, demonstrating healthy end-market demand for the company’s groundwater pumping systems and water treatment equipment. This revenue acceleration across the company’s flagship segment indicates underlying strength in residential, agricultural, and municipal water infrastructure spending, which should provide confidence in the sustainability of the growth trajectory.

Measured outlook. Management projected FY 2026 adjusted EPS in the $4.40 to $4.60 range, with revenue expected between $2.17B and $2.24B for the full year. The midpoint of the earnings guidance implies a modest sequential acceleration from the current quarterly run rate, suggesting management sees continued strength in order patterns but remains appropriately cautious about potential headwinds in the back half of the year. The revenue guidance range represents a relatively wide band, likely reflecting uncertainty around key end markets including agricultural spending and global infrastructure investment trends that have historically driven variability in Franklin Electric’s business mix.

Market pressure persists. The 4.6% post-earnings decline in Franklin Electric’s stock price appears disconnected from the fundamental beat delivered this quarter, potentially reflecting profit-taking after a strong run or investor concerns about the sustainability of Water Systems growth rates. With Wall Street consensus standing at 4 buy ratings and 4 hold ratings with no sells, the analyst community appears evenly split on the stock’s risk-reward profile at current levels, suggesting limited conviction about near-term upside despite the company’s execution track record in specialty pumping and water systems applications.

This content is for informational purposes only and should not be considered investment advice. AlphaStreet Intelligence analyzes financial data using AI to deliver fast and accurate market information. Human editors verify content.