Shares of General Mills, Inc. (NYSE: GIS) gained over 2% on Wednesday after the company posted better-than-expected earnings results for the second quarter of 2026. Revenue and earnings declined versus the previous year but surpassed analysts’ expectations. GIS continues to invest in its brands and these investments are anticipated to drive improvement through the remainder of the year.

Innovation to yield sales growth

General Mills continues to invest in its brands to drive volume-driven organic net sales growth. Its initiatives under the Remarkable Experience Framework are mainly focused on areas such as product, packaging, value, marketing, and omnichannel execution. In terms of product innovation, the company plans to generate a 25% increase in sales from new products in fiscal year 2026.

During the first half of the year, GIS saw strong performances from products like Cheerios Protein, Mott’s snack bars, and Annie’s Super Mac. In the second half of the year, the company plans to roll out products that cater to consumers’ preferences for healthier options, bold flavors, and familiar flavors. These include new offerings under its Nature Valley Protein Granola line, as well as the expansion of its Ghost protein cereal line and Ghost performance nutrition bars. The company is also launching new Old El Paso chimichanga and Mexican pizza offerings and a new line of Cheerios granola.

The branded foods provider is offering consumers new sizes and formats in packaging and it is adjusting prices to bring more value and convenience to them. It is also leveraging digital tools to improve its marketing efforts. In Q2, these measures helped drive high-single-digit retail pound growth in the salty and fruit snacks categories. Based on its early success with its new products, GIS believes it is on track to achieve double-digit sales growth from new products in FY2026.

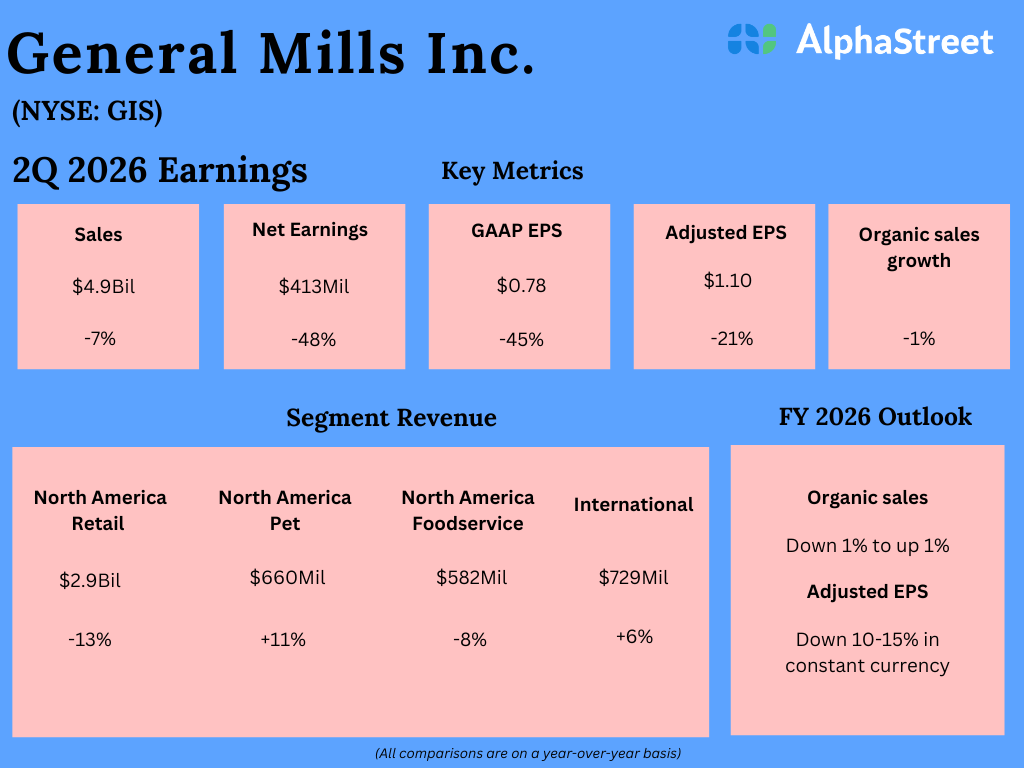

Q2 performance

In the second quarter of 2026, General Mills’ net sales decreased 7% year-over-year to $4.9 billion but beat estimates of $4.78 billion. Organic sales were down 1%, due to unfavorable price realization and mix. On a GAAP basis, earnings per share fell 45% to $0.78. On an adjusted basis, EPS declined 21% to $1.10 but surpassed projections of $1.02.

Sales in the North America Retail segment decreased 13%, with declines across US Snacks, US Meals & Baking Solutions, and Big G Cereal & Canada. Sales in North America Pet grew 11%, benefiting from the North American Whitebridge Pet Brands acquisition. Net sales rose double digits in cat food and pet treats, but dropped low-single digits in dog food. North America Foodservice saw sales decline by 8% while the International segment saw sales growth of 6%.

Outlook

General Mills continues to face a challenging consumer environment and the company is investing significantly in its brands to drive growth. These growth investments are expected to weigh on the bottom line during the year. GIS forecasts organic sales for fiscal year 2026 to be down 1% to up 1%. Adjusted EPS is expected to be down 10-15% in constant currency.