Shares of General Mills Inc. (NYSE: GIS) were down 4% on Tuesday despite the company delivering strong results for the second quarter of 2023 and raising its full-year outlook. The company believes that inflation, economic health of consumers, and supply chain volatility will continue to have a significant impact on its performance in fiscal year 2023.

Quarterly performance

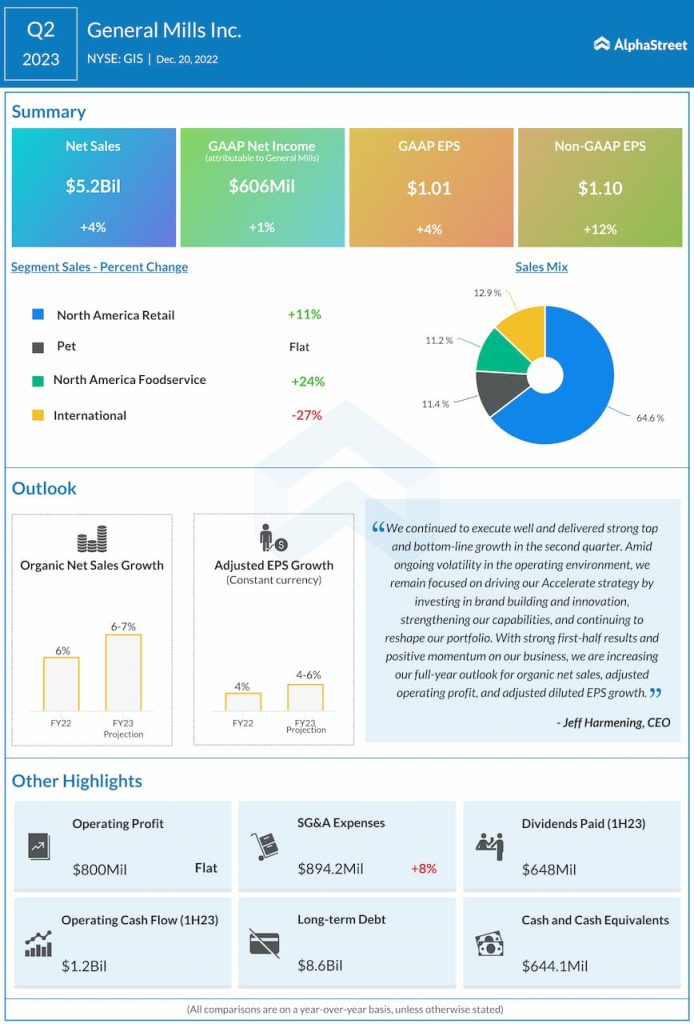

General Mills reported net sales of $5.2 billion for the second quarter of 2023, up 4% compared to the same period a year ago. Organic net sales increased by 11%, driven by positive net price realization and mix. GAAP EPS was up 4% to $1.01 while adjusted EPS rose 12% in constant currency to $1.10. The top and bottom line numbers both surpassed projections.

Category performance

In Q2 2023, General Mills recorded double-digit sales growth in its North America Retail and North America Foodservice segments, driven by pricing and mix. The company recorded an 18% sales growth in US Snacks and 10% growth in both US Meals & Baking Solutions and US Morning Foods. Sales in the International segment fell 27% in the second quarter, driven mainly by lower pound volume.

Net sales remained flat in the Pet segment as pricing and mix were offset by lower pound volume. Sales in this segment was hurt by a reduction in retailer inventory, capacity constraints and customer service challenges. Amid these headwinds, the Blue Buffalo brand continued to exhibit strength.

General Mills remains bullish on the growth prospects of its Pet business and it sees significant growth potential in particular for its Blue Buffalo pet food brand. On its earnings call, the company stated that the trends towards humanization and premiumization in the pet food category are strong and will continue to grow in the US and around the world.

GIS expects sales in the Pet segment to improve in the second half of 2023 getting back to double-digit growth. Customer service is expected to improve due to the capacity additions made by the company and this, combined with stable retail inventory levels, is expected to drive growth in the Pet business going forward.

Outlook

Looking ahead into fiscal year 2023, General Mills expects its performance to be impacted mainly by the inflationary environment, consumers’ economic health, and supply chain volatility. The company expects improvements in volume and price/mix to drive stronger growth in organic net sales. GIS expects input cost inflation to be 14-15% of total cost of goods sold for the full year.

Based on its strong first half results and the strength in its business, General Mills increased its outlook for the full year of 2023. The company now expects organic net sales growth of 8-9% versus the prior outlook of 6-7% growth. Adjusted EPS is expected to increase 4-6% in constant currency compared to the previous range of 2-5%.