Graham Corporation (GHM.NYSE), a U.S.-based designer and manufacturer of mission-critical fluid, heat-transfer, and vacuum systems for Defense, Space, and Energy & Process markets, delivered strong third-quarter fiscal 2026 results, supported by defense demand, strategic acquisitions, and growing aftermarket revenue. The company’s market capitalization is approximately $800 million, reflecting small-cap industrial sector positioning.

Sales Climb on Defense Momentum

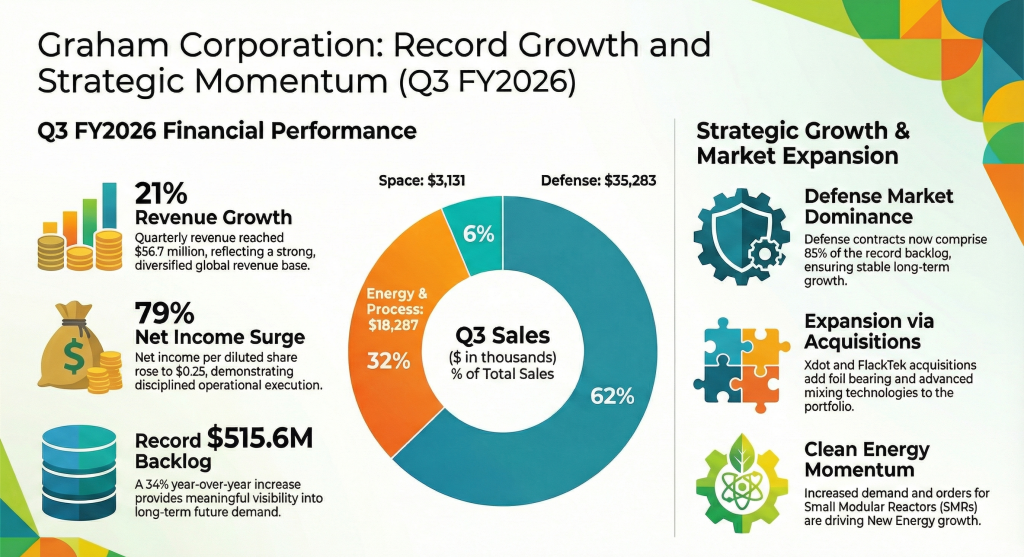

Graham reported net sales of $56.7 million, up 21% year-over-year, driven primarily by a 31% increase in Defense segment sales and contributions from new programs. Gross profit rose 15% to $13.5 million, while gross margin slightly declined to 23.8%, reflecting a higher mix of lower-margin sales, increased material costs, and the absence of a prior-year $0.3 million grant.

Profitability Gains Despite Margin Pressure

GAAP net income surged 79% to $2.8 million, or $0.25 per diluted share, with adjusted net income at $3.5 million, or $0.31 per share. Adjusted EBITDA increased 50% to $6.0 million, with a margin of 10.7%, benefiting from operational leverage and improved cost management. For the first nine months of fiscal 2026, Graham generated $16.1 million in net cash from operations.

Orders and Backlog Reach New Highs

Orders for Q3 reached $71.7 million, producing a book-to-bill ratio of 1.3x. Backlog hit a record $515.6 million, with 85% tied to Defense, providing extended revenue visibility. Management expects 35–40% of backlog to convert to sales within 12 months, with the remainder spread over multi-year Navy contracts.

U.S. Remains Core Revenue Base

Revenue continues to be heavily U.S.-focused, with domestic sales of $48.1 million (85%), up 21% year-over-year. International sales totaled $8.6 million, with Asia contributing $3.4 million (+51%) and the Middle East $1.4 million, slightly down from the prior year. Orders remain concentrated in the U.S., accounting for $68.7 million (96%) of new orders.

SG&A Efficiency Improves

Total SG&A, including amortization, was $10.6 million, up $0.9 million from Q3 2025. Personnel and benefits increased $597,000 due to headcount and technology investments. Acquisition and integration costs for FlackTek and Xdot contributed $539,000, while performance- and equity-based compensation added $237,000. These increases were partially offset by a $769,000 reversal of bad debt reserves, lowering SG&A as a percentage of sales to 18.6%, down from 20.6% a year ago.

Cash Flow and Capex Highlights

Unbilled revenue rose $19.3 million, balanced by a $27.8 million increase in customer deposits, reflecting a strong pipeline of funded work. Inventory increased to $48.5 million, driven by a $7.6 million rise in work-in-process. Net capital expenditures for the nine-month period totaled $13.3 million, including a $17.6 million Navy facility in Batavia (partially supported by a $13.5 million grant) and a cryogenic test facility in Jupiter, Florida, completed in February 2026.

Segment Performance and Aftermarket Growth

Aftermarket sales for Energy & Process and Defense markets totaled $10.8 million, up 11%, highlighting recurring revenue strength. In Energy & Process, revenue was supported by Small Modular Reactors (SMRs), fueled by demand from AI data centers and cryptocurrency mining. Space revenue fell 18% to $3.1 million, reflecting launch program variability.

Tax Benefits and Legislative Support

The effective tax rate fell to 11%, from 29% in Q3 2025, primarily due to higher-than-expected R&D tax credits. The One Big Beautiful Bill (OBBB) Act is expected to provide approximately $8 million in cash tax savings over two years, offsetting modest upward pressures on the effective tax rate.

Strategic Acquisitions Drive Technology Expansion

The FlackTek acquisition for $35 million establishes a third platform in advanced mixing and material processing, serving sectors including energetics, medical, and battery markets. The MEGA mixer provides 24x higher throughput than conventional planetary mixers. Xdot, acquired for $0.9 million, adds foil bearing technology to Barber-Nichols, contributing $0.5 million to Q3 backlog and expanding high-speed rotating machinery capabilities.

Updated Guidance and Growth Outlook

Graham raised full-year guidance following strong results and FlackTek integration, projecting revenue of $233–$239 million and adjusted EBITDA of $24–$28 million. Capital expenditures are expected at $15–$18 million, and the effective tax rate at 16–18%. Management reaffirmed its strategic fiscal 2027 goal of 8–10% organic revenue growth and low- to mid-teen adjusted EBITDA margins.

Competitive Positioning

Backlog strength, defense exposure, and diversified technology platforms differentiate Graham from peers such as SPX Flow, Flowserve, and Chart Industries. While macroeconomic and geopolitical factors influence capital project timing, the company’s combination of recurring aftermarket demand, specialized energy technologies, and strategic acquisitions positions it to sustain growth and margin expansion.