With over 190% growth so far this year, streaming company Roku (NASDAQ: ROKU) has been one of the best-performing stocks in 2019. The growth has been driven by its operational excellence and not by any outside factors, which underpins the bullish outlook on the stock.

With the stock price now hitting three-digit figure, investors are left wondering how much more of the fireworks are left in Roku. A few days back, RBC Capital Markets said in an investors’ note that the stock is not anymore a good pick and the bull run is over. It also downgraded Roku to “sector perform” from “outperform,” though the price target was left unchanged at $90.

On the whole, analysts continue to be divided on their

opinion on the stock, with six out of 12 recommending Buy. While four analysts

have a Hold rating, two have Sell. In this scenario, it becomes difficult of an

investor to be absolutely sure about a stock.

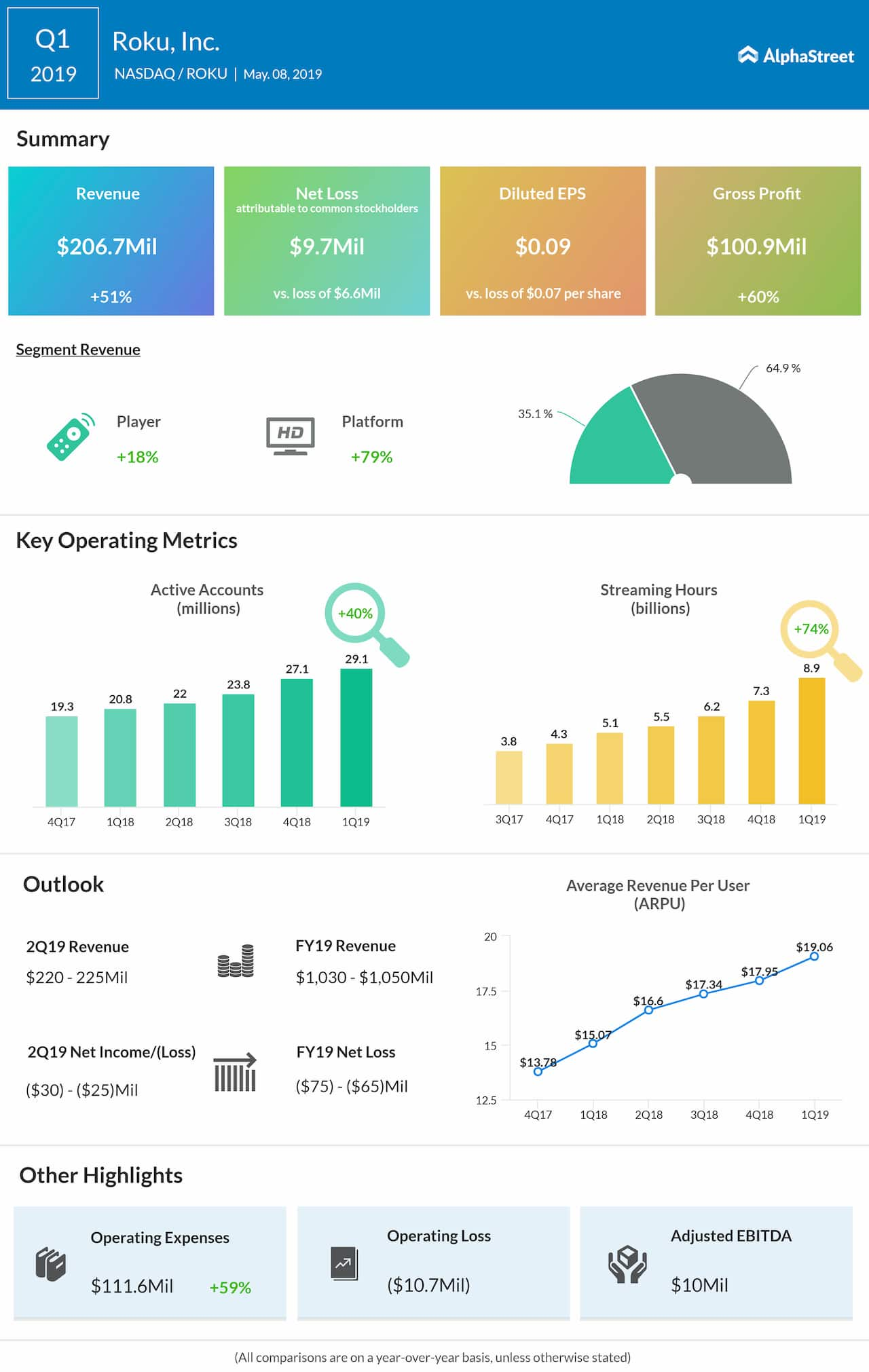

There is only one slight detail that you need to focus on to merit the stock. All analysts converge on the stock’s long-term prospects, driven by the massive expansion opportunities that are present outside the US market, as well as the remarkable growth trend achieved in the advertising segment, aka the Platform unit (see image).

READ: Electric airplanes: The market, the challenges, and the key players

The platform business, which generates money through subscriptions, OS licensing, advertising and transaction revenues, has been churning high margin returns to the Los Gatos, California-based company.

Though the company is popularly known for its hardware, this segment (Player) currently accounts for only about one-third of its total revenue.

Also to be noted is the fact that international revenues accounted for only about a tenth of its total revenue in the most recent quarter. You may expect further expansions in the years to come, which is likely to establish Roku as a leading content streamer.

In the short term though, the stock may experience a

correction, following the long bull run. On an average, the stock has a 12-month

price target of $89, which is at a 14% downside from the last close.

However, if you are planning to hold it longer, you may see more returns coming your way. Wall Street expects 41% growth in sales in the current fiscal year and 34% growth in the next one. Hence, even if you suffer short-term losses, keeping it locked would probably secure better returns.

Get access to timely and accurate verbatim transcripts that are published within hours of the event.