Leading toymakers Hasbro Inc. (NASDAQ: HAS) and Mattel Inc. (NASDAQ: MAT) witnessed revenue and profit growth during their most recent quarters. The companies have seen healthy performance from most of their brands and they have been investing significantly in their entertainment offerings. As the important holiday season approaches, here’s a look at what these toymakers have planned in the near term:

Revenue and profits

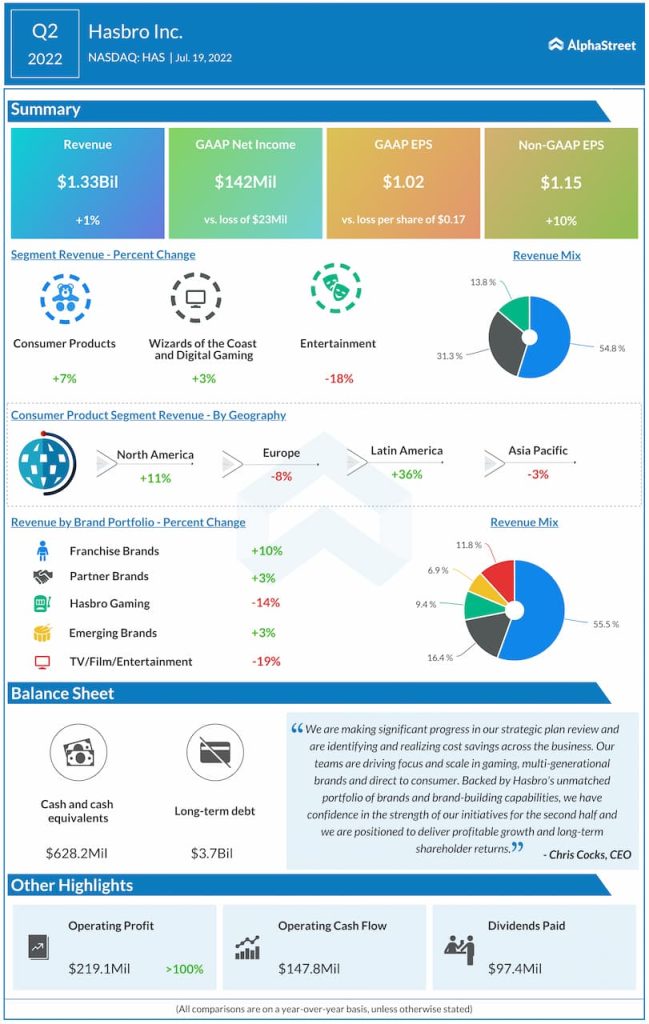

In the second quarter of 2022, Hasbro’s revenues increased by 1% year-over-year to $1.34 billion, helped by growth in its Consumer Products, and Wizards of the Coast and Digital Gaming segments. Mattel’s net sales for the same period rose 20% YoY to $1.23 billion, driven by double-digit sales growth in its North America and International segments.

For Q2, Hasbro reported adjusted EPS of $1.15, which was up 10% YoY while Mattel delivered adjusted EPS of $0.18, reflecting a growth of $0.15 from the year-ago period.

For the full year of 2022, Hasbro expects revenue to grow in low-single digits on a constant currency basis and operating profit to grow in mid-single digits to achieve an adjusted operating profit margin of 16%. For FY2022, Mattel expects net sales to grow 8-10% YoY in constant currency and adjusted EPS to range between $1.42-1.48.

Brands and categories

During the second quarter, gains from popular brands such as Play-Doh, My Little Pony, and Power Rangers helped drive a 7% growth in revenue for Hasbro’s Consumer Products segment. A 15% growth in Tabletop revenue led by Magic: The Gathering helped drive a 3% increase in revenue for the Wizards of the Coast and Digital Gaming segment.

For the full year of 2022, Hasbro expects low single digit revenue growth for Consumer Products and high single-digit to low double-digit revenue growth for the Wizards segment on a constant currency basis.

In Q2, Mattel saw billings growth for Dolls and Vehicles led by brands such as Barbie, Polly Pocket, and Hot Wheels. The Challenger categories saw a 48% rise in billings driven by Action Figures and Building Sets.

For FY2022, gross billings are expected to grow for Dolls, Vehicles and the Challenger categories, driven by Polly Pocket, Hot Wheels and Action Figures. Billings for Dolls will benefit from the relaunch of the Monster High brand. Billings for the Infant, Toddler and Preschool segment is also expected to grow led by Fisher-Price and Thomas & Friends.

Entertainment opportunity

Both Hasbro and Mattel are looking to maximize the value of their brands in the entertainment space. In Q2, Hasbro saw gains in its products for the Marvel and Star Wars franchises. The company has over 200 projects in development across film and television. There are over 35 development projects for Hasbro brands, which include content for Transformers, Dungeons & Dragons, My Little Pony and Power Rangers. Despite a double-digit decline in its Entertainment segment during Q2, Hasbro expects to see revenue growth for the full year in this division.

Mattel is working on capturing the full value of its IP in highly accretive business verticals like content, consumer products and digital experiences. The company has a Barbie movie coming out next year that will be released by Warner Bros. It is also working on movies and series based on titles like Matchbox, Monster High, and He-Man and the Masters of the Universe. Mattel sees huge opportunity in consumer products and digital experiences.

FY2023 outlook

Mattel aims to achieve high single-digit net sales growth in constant currency and adjusted operating income margin of 16-17% for FY2023. The company’s goal for EPS is to exceed adjusted EPS of $1.90 for the year.

Click here to read the full transcripts of Hasbro and Mattel’s Q2 2022 earnings conference calls