Shares of United Airlines Holdings Inc. (NASDAQ: UAL) were down over 1% on Friday. The stock has gained 17% year-to-date. Earlier this week, the company reported its first quarter 2023 earnings results, delivering a year-over-year increase in revenue along with a narrower loss. Here’s a look at the near-term expectations for the airline:

Revenue and profitability

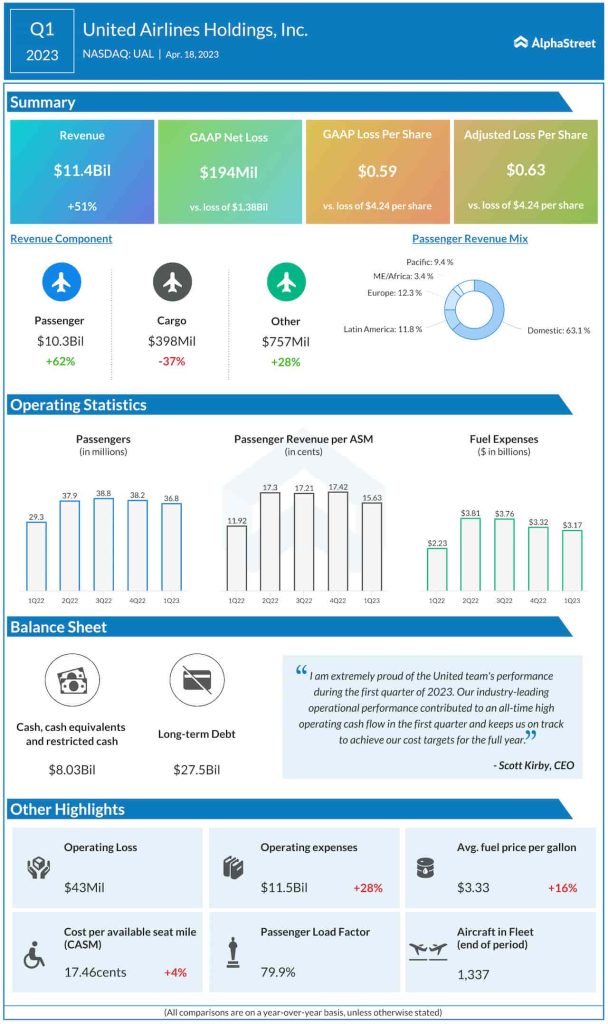

In the first quarter of 2023, United’s total operating revenue increased 51% year-over-year to $11.4 billion. Passenger revenues were up 62% while cargo revenues fell 36%. Total revenue per available seat mile (TRASM) increased 22.5% while passenger revenue per available seat mile (PRASM) rose 31.1%. Capacity was up 23.4%.

Looking into the second quarter of 2023, United anticipates favorable trends for business travel, with the rebound most pronounced in global long-haul markets. Total revenue is expected to be up 14-16% in Q2 2023 compared to the same period last year, with capacity up approx. 18.5%.

In Q1, the company reported a GAAP net loss of $194 million, or $0.59 per share, compared to a loss of $1.38 billion, or $4.24 per share, in the year-ago period. Adjusted loss per share was $0.63 versus a loss of $4.24 per share last year.

United expects adjusted EPS to be $3.50-4.00 for the second quarter of 2023 and $10-12 for the full year of 2023. Earnings growth in Q2 is expected to be supported by strong cost performance.

Costs

In Q1, United’s non-fuel costs, or CASM-ex, was down 0.1% from the year-ago period. For the second quarter of 2023, the company expects CASM-ex to be flat to up 2% compared to the prior-year period. Fuel price is estimated to range between $2.80-3.00. For the full year of 2023, United remains on track to keep CASM-ex approx. flat versus 2022. The company anticipates a decline in non-fuel unit costs during the second half of 2023 compared to the same period in 2022.