Shares of The Campbell’s Company (NASDAQ: CPB) stayed green on Monday. The stock has dropped 16% over the past three months. The food company, which underwent a name change recently, has been facing a dynamic consumer environment which impacted organic sales for its most recent quarter. Here’s a look at its quarterly performance against this backdrop:

Sales and earnings

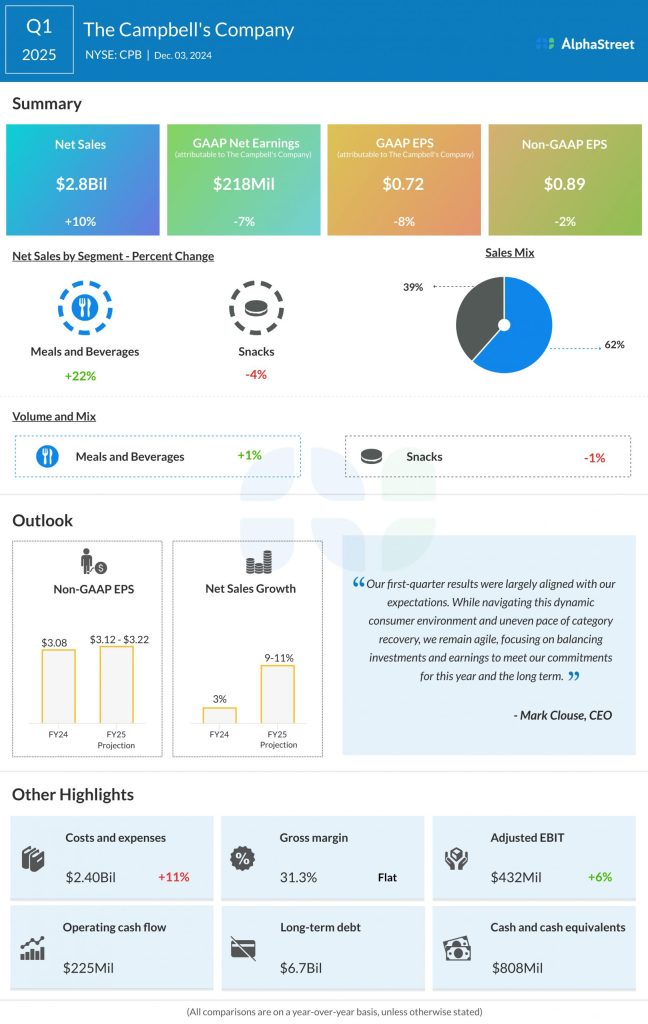

In the first quarter of 2025, Campbell’s net sales increased 10% year-over-year to $2.8 billion, reflecting the benefit from the Sovos Brands acquisition. Organic sales dipped 1%, due to a dynamic consumer environment and impacts from movements in retailer inventory levels caused by the late timing of the Thanksgiving holiday. Adjusted EPS fell 2% to $0.89.

Business performance

Campbell’s has reshaped its portfolio and is focusing on 16 brands which it believes has the largest potential for growth and margin improvement. These brands, which are termed its leadership brands, comprise eight brands each from both its Meals & Beverages and Snacks segments. In Q1, the leadership brands made up the majority of net sales and saw dollar consumption growth of nearly 2%.

In the first quarter, the Meals & Beverages segment saw sales grow by 22%, benefiting from the Sovos acquisition. Organic sales remained flat. The soup portfolio benefited from gains in broth and improvements in the ready-to-serve category. The condensed soup segment saw share growth, led by growth in red and white cooking soups as consumers prepare more meals at home. The company expects to see a pickup in condensed eating soup as the weather gets colder.

Campbell’s continues to benefit from strong momentum in Italian sauces, led by Rao’s and Prego. In Q1, Rao’s delivered in-market consumption growth of 15%. The company now expects pro forma growth for Rao’s to be slightly above 10% in fiscal year 2025. It sees significant opportunity for expansion for these brands, with rising adoption from millennial households.

In Q1, the Snacks segment saw sales drop by 4% while organic sales were down 2%. The company faced heavy competition in certain snack categories both from new brands as well as private label in certain salty snacks and cookies. However, it began to see a recovery in its snacking categories with gains in crackers, fresh bakery and deli snacks.

Outlook

Campbell’s continues to invest in its brands as it navigates the complex consumer environment. It expects the second quarter of 2025 to be a key indicator of its progress. In Q2, the company expects to see sequential improvement from the first quarter, with organic sales growth remaining relatively flat versus the prior year. Adjusted EPS is expected to be in the low $0.70 range. Organic growth is expected to modestly improve during the second half of fiscal year 2025 compared to the first half. The company also expects to see adjusted EPS progress in the latter half of FY2025.