Shares of KB Home (NYSE: KBH) fell 8% on Friday. The company reported its earnings results for the fourth quarter of 2025 and although the top and bottom line numbers declined versus the previous year, they surpassed market projections. The homebuilder, like its peers, continues to face tough housing market conditions but remains focused on its strategy to navigate this difficult environment.

Better-than-expected results

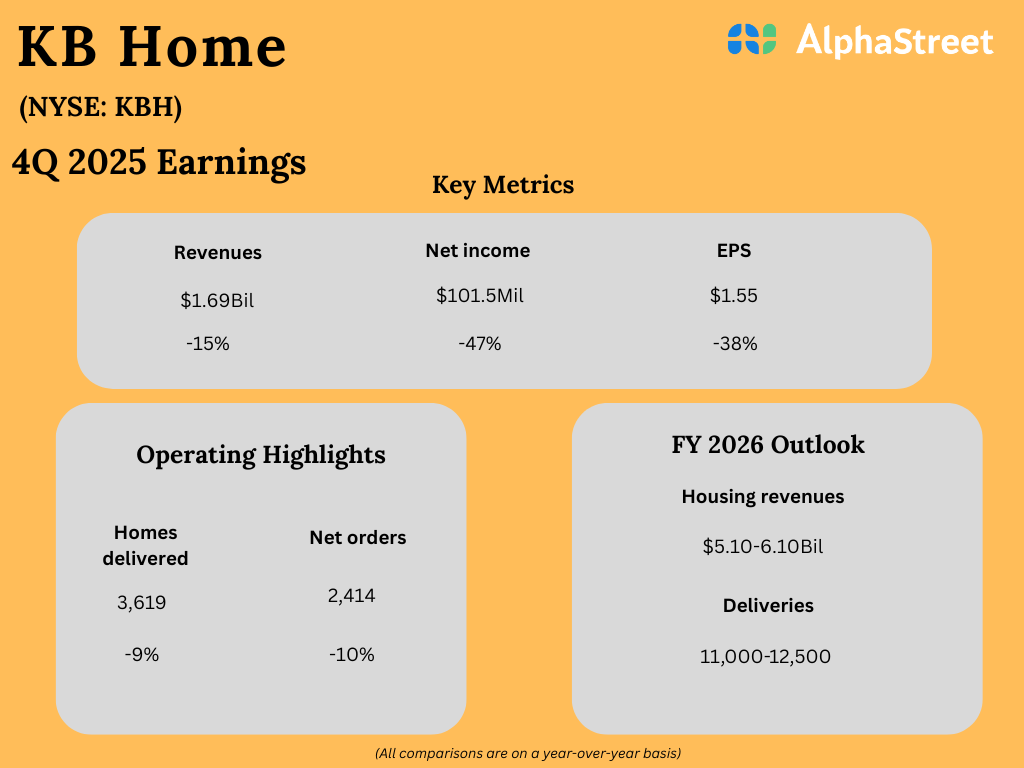

KB Home’s revenue and earnings for the fourth quarter of 2025 decreased versus the year-ago period but came ahead of estimates. Revenues of $1.69 billion were down 15% year-over-year. On a GAAP basis, earnings per share fell 38% to $1.55. Adjusted EPS declined 24% to $1.92.

Steering through market headwinds

As mentioned on its earnings call, KB Home remains optimistic about the housing market as it believes there is underlying demand for homes supported by factors such as population, household formation, and job and wage growth. However, affordability constraints in the near term are causing consumers to prolong their decisions on home-buying.

In Q4, KBH’s net orders decreased 10% to 2,414, and homes delivered declined 9% to 3,619. Average selling price fell 7% to $465,600. Adjusted housing gross profit margin dropped to 17.8% from 20.9% last year, due to price reductions, higher relative land costs and geographic mix.

The company continues to focus on improving its build times, lowering direct costs, and balancing pace and price. It believes in offering transparent and affordable prices rather than heavy incentives. KBH saw steady traffic in its communities during the fourth quarter and it ended the period with 271 active communities, which was up 5% from the previous year.

KB Home is also focusing more on its built-to-order (BTO) model, which allows customers to choose homes according to their preferences and budget. BTO homes tend to generate higher margins compared to inventory homes. KBH saw a shift towards more BTO sales during November and this trend has continued into December.

In the first quarter of 2026, KBH is planning to open 35-40 new communities, which are expected to generate favorable gross margins, helped by a sales mix that is largely built-to-order. In Q4, BTO homes made up 57% of total deliveries and the company is focused on bringing this number to 70% or higher.

Outlook

For the first quarter of 2026, KB Home expects to generate housing revenues of $1.05-1.15 billion on expected deliveries of 2,300-2,500 homes. Adjusted housing gross profit margin is expected to be 15.4-16.0%. Margins are likely to be impacted by factors such as pricing pressure and higher lot costs and the company plans to partly offset this pressure with lower direct construction costs per unit.

KBH expects margins to improve through fiscal year 2026, helped by its strategy to shift the sales mix to more BTO homes. For FY2026, the company expects deliveries of 11,000-12,500 homes and housing revenues of $5.10-6.10 billion.